Shares of Immunovant Inc (IMVT) Stock trading near the high end of its 52-week range

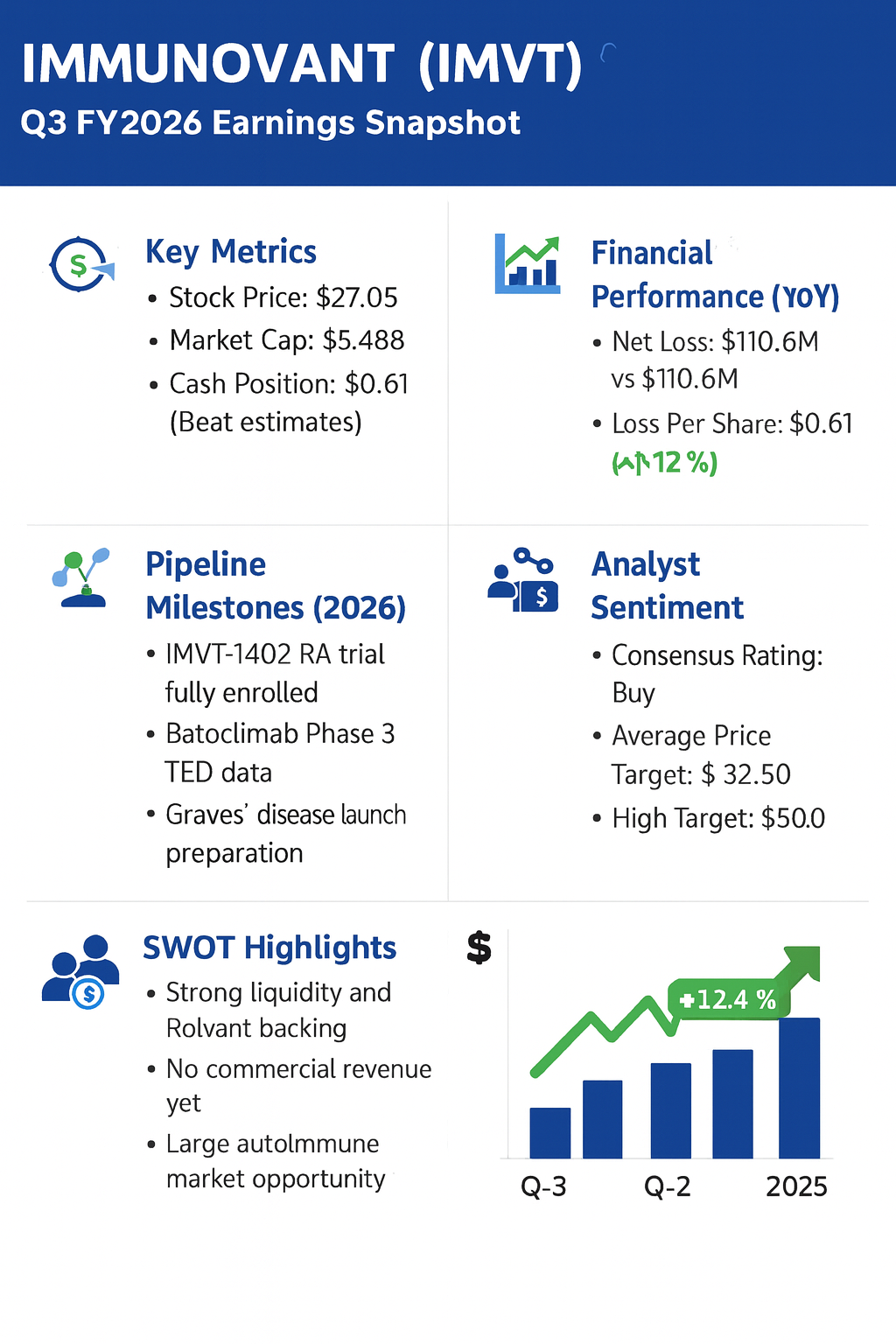

Shares of Immunovant Inc (IMVT) rose 12.4% to $27.05 in Friday trading following the release of third-quarter fiscal year 2026 results that surpassed analyst expectations. The stock is trading near the high end of its 52-week range of $12.72 to $27.80. The intraday gain follows a reported quarterly net loss that was narrower than consensus forecasts, alongside updates on multiple potentially registrational clinical trials.

Company Description: Immunovant is a clinical-stage biopharmaceutical company focused on developing therapies for patients with autoimmune diseases mediated by pathogenic IgG antibodies. The company’s lead assets, IMVT-1402 and batoclimab, target the neonatal Fc receptor (FcRn) to reduce levels of circulating IgG. Its primary development programs focus on indications including Graves’ disease, thyroid eye disease, myasthenia gravis, and rheumatoid arthritis.

Current Stock Price: $27.05 (Close, Feb 6, 2026)

Market Capitalization: Approximately $5.48 billion

Valuation: As a clinical-stage biotechnology company with no commercialized products, Immunovant lacks a meaningful forward P/E ratio. Valuation is primarily driven by its cash position, which was significantly bolstered by a $550 million equity financing in December 2025, and the anticipated commercial potential of its late-stage immunology pipeline.

Narrower Loss and Bolstered Cash Reserves

Immunovant reported a net loss of $110.6 million, or $0.61 per share, for the third quarter ended December 31, 2025. This result beat the analyst consensus estimate of a $0.72 loss per share. For the first nine months of fiscal 2026, the company reported a non-GAAP net loss of approximately $167 million.

| Metric | Q3 FY2025 | Q3 FY2026 | YoY Change |

| Total Revenue | $0 | $0 | N/A |

| Net Loss | $111.1M | $110.6M | -0.45% |

| Net Loss Per Share | $0.76 | $0.61 | -19.7% |

| R&D Expenses | $94.5M | $98.9M | +4.6% |

Research and development (R&D) expenses rose to $98.9 million from $94.5 million in the prior-year period, driven by clinical trial acceleration for IMVT-1402. General and administrative (G&A) expenses fell to $15.4 million from $19.8 million. The company ended the quarter with $994.5 million in cash and cash equivalents, up from $713.9 million as of March 31, 2025, providing a runway through the anticipated launch of its Graves’ disease program.

Pipeline Progress and Analyst Sentiment

Management confirmed that the potentially registrational trial for IMVT-1402 in difficult-to-treat rheumatoid arthritis (D2T RA) is now fully enrolled, with topline data expected in the second half of 2026. Topline data from two Phase 3 trials of batoclimab in thyroid eye disease (TED) are anticipated in the first half of 2026.

Following the results, analyst consensus remains “Buy,” with an average price target of $32.50. Some firms, including Wolfe Research, have set targets as high as $50.00, citing the multibillion-dollar potential of the Graves’ disease market, which affects approximately 880,000 patients in the U.S..

Macro Pressures and Geopolitical Exposure

As a clinical-stage entity, Immunovant faces sector-wide pressures including a high cost of capital for R&D-heavy firms and intense competition in the FcRn-inhibitor space from established players like argenx.

The company maintains limited direct exposure to geopolitical risks or tariffs as its primary operations and clinical sites are currently centered in North America. However, future commercialization would require a global supply chain for biologics, which could be subject to international regulatory divergence and trade policies impacting pharmaceutical manufacturing.

Immunovant Inc (IMVT) SWOT Analysis

Strengths

- Strong Liquidity: ~$995M cash position following $550M financing supports operations through multiple clinical readouts.

- Leading IgG Reduction: Pipeline assets show potential for deeper IgG reduction compared to first-generation inhibitors.

- Strategic Backing: Strong support from parent company Roivant Sciences, which recently increased its stake.

Weaknesses

- Zero Revenue: Typical for clinical-stage biotech, but necessitates continuous capital market access.

- Clinical Risk: Valuation is highly concentrated on successful outcomes of Phase 3 trials in TED and Graves’ disease.

- Pipeline Concentration: Heavy reliance on the success of the FcRn-targeted mechanism across multiple indications.

Opportunities

- First-in-Class Potential: IMVT-1402 could become the first-in-class therapy for several orphan inflammatory diseases.

- Market Expansion: Graves’ disease represents a large underserved market with nearly 900,000 U.S. patients.

- Multiple Readouts: Imminent Phase 3 data in TED and Phase 2b data in rheumatoid arthritis serve as major catalysts in 2026.

Threats

- Intense Competition: Competing FcRn therapies from larger biopharma companies could limit future market share.

- Regulatory Hurdles: Potential delays in NDA submissions or FDA approval processes.

- Patent Litigation: Sector-wide risk of IP challenges as the FcRn market matures.