Shares of Visa (NYSE: V) were down 1% on Friday. The stock has dropped 3% over the past three months. The payments giant continues to see strong momentum in its business with robust revenue and profit growth in its most recent quarter, supported by strength in its payments solutions and value-added services.

Revenue and earnings growth

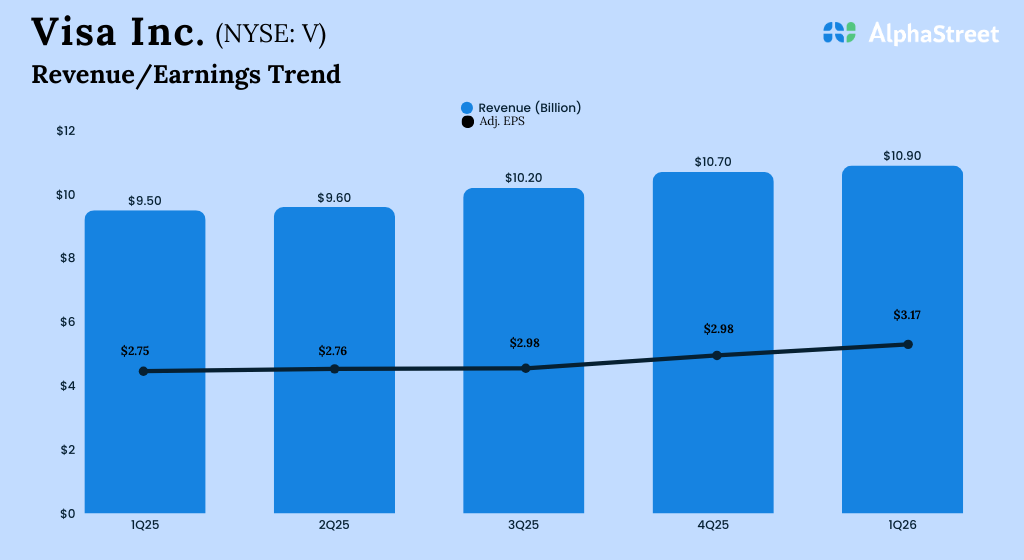

Visa saw strong revenue and earnings growth for the first quarter of 2026, driven by resilient consumer spending. Revenues and adjusted earnings per share both increased 15% year-over-year to $10.9 billion and $3.17, respectively, with the top line benefiting from gains in value-added services and commercial and money movement solutions, and the bottom line aided by revenue growth.

Growth drivers and value-added services

Visa saw strong performance in its business during the first quarter of 2026. Global payments volume increased 8% YoY in constant dollars, with growth in both US and international payments volume. In the US, consumer spending remained resilient, with rapid growth in ecommerce compared to in-person spend. Both credit and debit payments were up, and both discretionary and non-discretionary spend stayed strong.

Total processed transactions grew 9% YoY to 69.4 billion, while total cross-border volume, in constant dollars and excluding intra-Europe transactions, grew 11% YoY in Q1.

During the quarter, strong payments volume, cross-border volume and processed transaction growth helped drive consumer payments revenue. Visa credentials form an important part of the consumer payments business. V has been improving Visa credentials through tap to pay, Visa Flex Credential and tokens. More than 80% of face-to-face transactions are now done using tap to pay. The company has about 20 million Visa Flex credentials and over 17.5 billion tokens globally, with both showing rapid growth.

Commercial and money movement solutions revenue rose 20%, with a 10% growth in commercial payments volume. Visa Direct transactions grew 23% to 3.7 billion transactions, with both domestic and cross-border showing strength. Value-added services revenue grew 28% YoY to $3.2 billion, helped by greater demand for advisory and other services.

Outlook

For the full year of 2026, Visa expects adjusted revenues to grow in the low-double-digits, as it anticipates a weaker volatility environment for the remainder of the year. Adjusted EPS is also expected to grow in the low-double-digits.

For the second quarter of 2026, the company expects adjusted revenue growth in the low-double-digits, as it anticipates lower contribution from pricing, lower volatility, and higher incentive growth versus the first quarter. In Q1, revenues grew 13% on a constant-dollar basis. Adjusted EPS growth in Q2 is projected to be at the high-end of low-double-digits.