Shares of Lowe’s Companies Inc. (NYSE: LOW) were down over 1% on Wednesday. The stock has gained 9% over the past 12 months. The home improvement retailer reported its first quarter 2024 earnings results a day ago, which exceeded estimates despite declining from the year-ago period. Here are a few points to note from the Q1 report:

Better-than-expected results

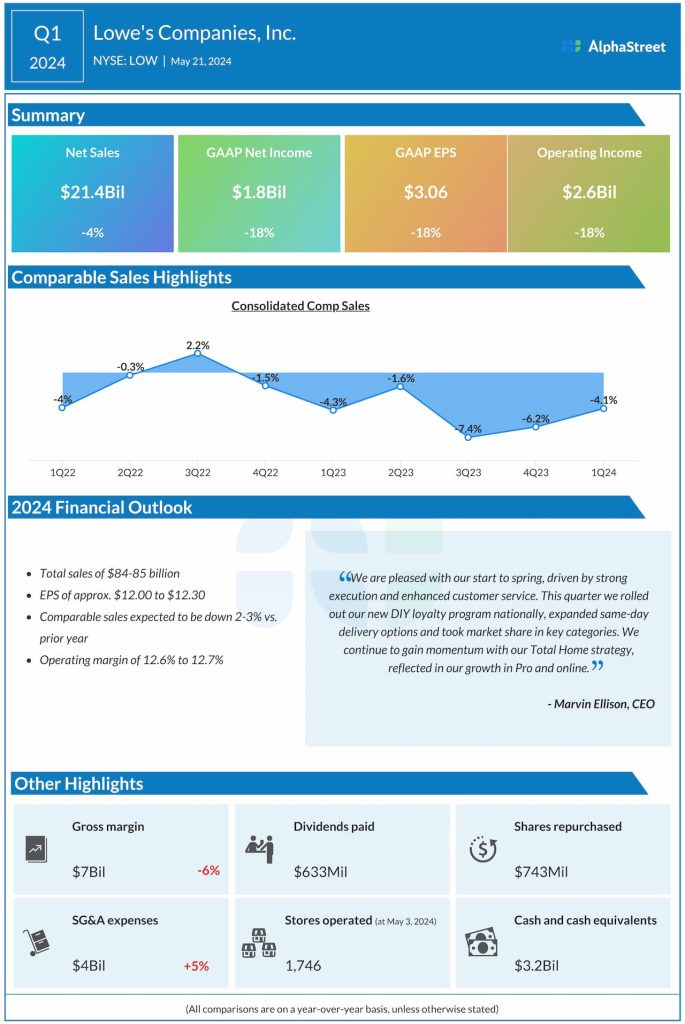

Lowe’s total sales for Q1 2024 decreased 4% year-over-year to $21.4 billion. Net income fell 18% to $1.8 billion, or $3.06 per share, compared to last year. Despite the year-over-year declines, both the top and bottom line numbers surpassed projections.

DIY weakness, strength in Pro

In Q1, Lowe’s comparable sales declined 4.1%, mainly due to the continued weakness in DIY big ticket discretionary spending. Comparable transactions decreased 3.1% during the quarter. Despite these headwinds, the retailer delivered better-than-expected spring seasonal sales.

The company’s Total Home strategy is paying off as it saw positive growth in Pro and online sales during Q1. Pro comps were positive in the quarter as strategic investments helped drive higher sales and customer engagement. Lowe’s recorded positive Pro comps across all three geographic divisions. Online sales rose around 1% in Q1.

As mentioned on the quarterly call, the Pro customer has proven resilient with recent surveys indicating healthy backlogs in line with last year. Lowe’s is focused on taking share with the small to medium-sized pros, who represent half of the highly fragmented $500 billion Pro market.

Comparable average ticket dipped 1% in Q1, as strength in Pro partly offset lower DIY bigger ticket sales and appliance pricing pressure. Factors like inflationary pressures, uncertainty around interest rate cuts, and customers’ preference for spending on discretionary services and experiences continue to weigh on DIY home improvement demand. Looking ahead to the full year, Pro sales are expected to outpace DIY.

Outlook

Lowe’s affirmed its outlook for the full year of 2024. The company continues to expect sales to range between $84-85 billion and EPS to range between $12.00-12.30. Comparable sales are expected to be down 2-3% from the prior year.

Based on the trends it is seeing in the business, Lowe’s expects comparable sales for the second quarter of 2024 to be roughly in line with the first quarter. The company expects comp sales in the second half to improve as it cycles over easier comparisons against the year-ago period, when the pullback in DIY intensified during Q3 2023. Lowe’s reiterated that it was not forecasting an improvement in demand trends but stating that comparisons would be easier in the second half of the year.