Shares of Campbell Soup Company (NASDAQ: CPB) rose over 1% on Friday. The stock has gained 21% over the past three months. The company delivered sales and earnings growth for the fourth quarter of 2024 against a dynamic consumer landscape. The Meals & Beverages segment recorded healthy gains during the quarter while the Snacks division continued to feel some pressure. Here’s a look at the soup-maker’s Q4 performance and its expectations for the coming fiscal year:

Sales and profits

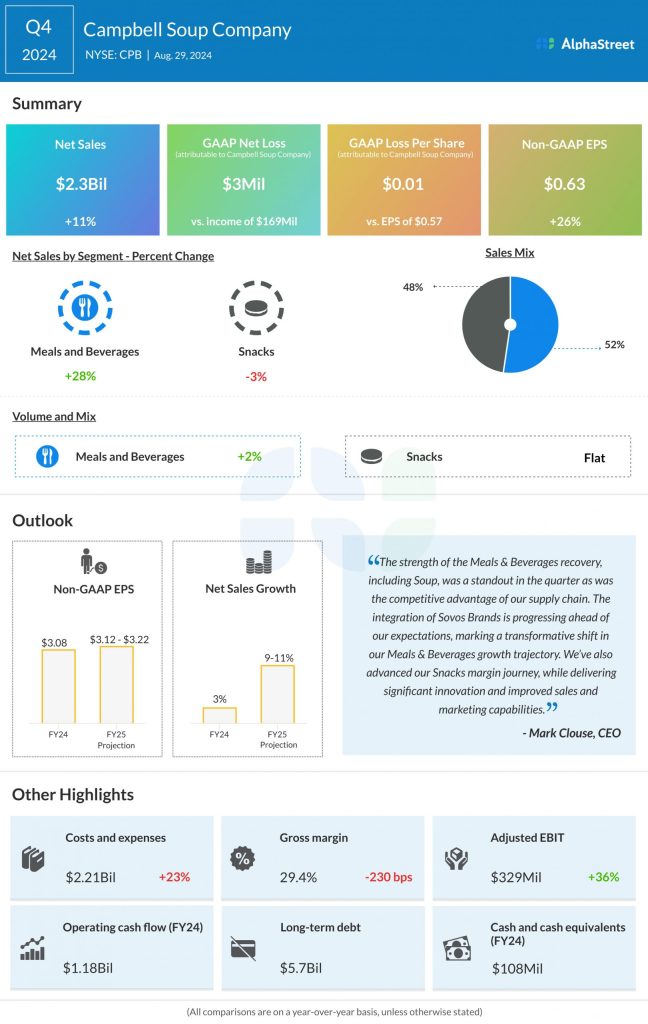

In Q4 2024, Campbell’s net sales grew 11% year-over-year to $2.3 billion, helped by benefits from the Sovos Brands acquisition. Organic sales dropped 1%. Adjusted EPS increased 26% to $0.63 in the quarter.

Campbell’s full-year 2025 guidance takes into account the ongoing recovery in the consumer environment. It also reflects the recent divestiture of the Pop Secret popcorn business. The company expects the impact of the divestiture to reduce reported net sales growth by approx. 1% and have a dilutive impact of $0.04 on adjusted EPS in FY2025.

Net sales are expected to grow 9-11% in FY2025 while organic sales are expected to be flat to up 2%. Adjusted EPS is expected to grow 1-4% for the year.

Segment performance

In Q4, sales in the Meals & Beverages segment increased 28%, helped by benefits from the Sovos Brands acquisition. Organic sales rose 1%, driven by gains in US soup, foodservice, and Prego pasta sauces, partly offset by declines in beverages. Sales of US soup grew 2%, driven by an increase in broth, partly offset by declines in ready-to-serve and condensed soups.

As mentioned on its conference call, during the quarter, Campbell recorded robust share gains in its Swanson broth business. The category continues to benefit from consumers opting for home cooking over dining out. In the Italian Sauces category, the company appears to be well-positioned to grow market share with the Rao’s and Prego brands, both of which are performing well. Campbell anticipates high single digit growth for Rao’s in fiscal year 2025.

The Snacks segment recorded a 3% drop in sales, on a reported and organic basis, in the fourth quarter. The company saw a 1% growth in power brands and a 1% decline in partner and contract brands. Partner and contract brands are low-margin compared to power brands and Campbell has been working on reducing its reliance on these businesses.

The company has been focusing more on its own brands and on improving the mix of its business but this is a headwind for the top line in the near term and it is expected to continue in FY2025. Campbell has been facing tough competition on its power brands but it is seeing gains in key brands like Goldfish, and it anticipates continued growth in these brands within its Snacks portfolio.