The toy industry is facing challenges as demand in general remains weak due to a tough macro environment. Against this backdrop, toy giant Hasbro Inc. (NASDAQ: HAS) delivered lower revenues in its most recent quarter and cut its guidance for the full year. Its rival Mattel, Inc. (NASDAQ: MAT) managed to deliver better results on the back of its successful Barbie movie.

Revenue and profits

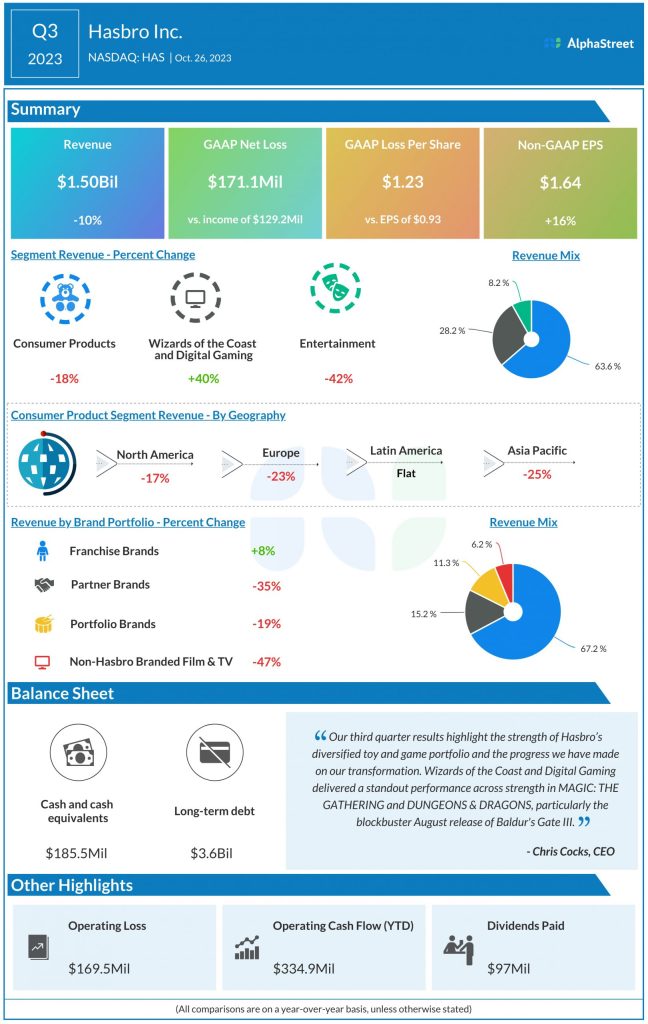

In the third quarter of 2023, Hasbro generated total revenue of $1.5 billion, which was down 10% year-over-year, as growth in the Wizards of the Coast and Digital Gaming segment was offset by declines in the Consumer Products and Entertainment segments. Adjusted EPS grew 16% YoY to $1.64.

Mattel’s net sales grew 9% to $1.9 billion in Q3 2023 compared to the prior-year period. Revenues grew 7% in constant currency. The company saw a rise in demand for its products during the quarter and its results benefited from the success of the Barbie movie. Adjusted EPS increased 32% YoY to $1.08.

Category performance

During the third quarter, Hasbro saw double-digit revenue declines in its Consumer Products and Entertainment segments due to planned license exits, softness in the overall toy industry and the impacts from the writers’ and actors’ strikes. The Wizards segment saw revenue growth of 40% helped by strong gains from Baldur’s Gate III, Monopoly Go! and MAGIC: THE GATHERING.

Mattel saw net sales increase by 10% in both its North America and International segments. Gross billings growth in these segments were driven by strength in Dolls and Vehicles, partly offset by Action Figures, Building Sets and Games. Net sales in the American Girl segment fell 13% in Q3.

Outlook

Hasbro believes the upcoming holiday season will be hugely driven by deals. The company is working with retail partners to provide customers with interesting offers and also on generating cost savings to improve margins.

Hasbro lowered its full-year 2023 revenue outlook on softness in Consumer Products. It now expects total revenue to decline 13-15% in FY2023 and the Consumer Products segment to see a decline in the mid to high teens. The Entertainment segment is expected to see revenues decline by 25-30% while the Wizards segment is expected to see an increase in the high single digits.

Mattel expects a strong holiday season. It expects to see top line growth and gross margin expansion in the fourth quarter of 2023. For full-year 2023, the toymaker expects net sales to be comparable to last year in constant currency.

Mattel expects continued benefits from the Barbie movie, along with growth in the Dolls and Vehicles categories. This is likely to be offset by declines in the overall toy industry as well as weakness in the company’s Infant, Toddler and Preschool, and Challenger categories. The company raised its adjusted EPS guidance to a range of $1.15-1.25 from $1.10-1.20.

Shares of Hasbro have dropped 25% while Mattel’s stock has gained 7% thus far this year.