Shares of Target Corporation (NYSE: TGT) stayed green on Thursday. The stock has dropped 13% year-to-date. The retailer delivered mixed results for the second quarter of 2023 a day ago and lowered its outlook for the full year. Its earnings beat was a silver lining to the revenue miss and guidance cut. Here’s a look at the headwinds faced by the company in its most recent quarter:

Sales decline

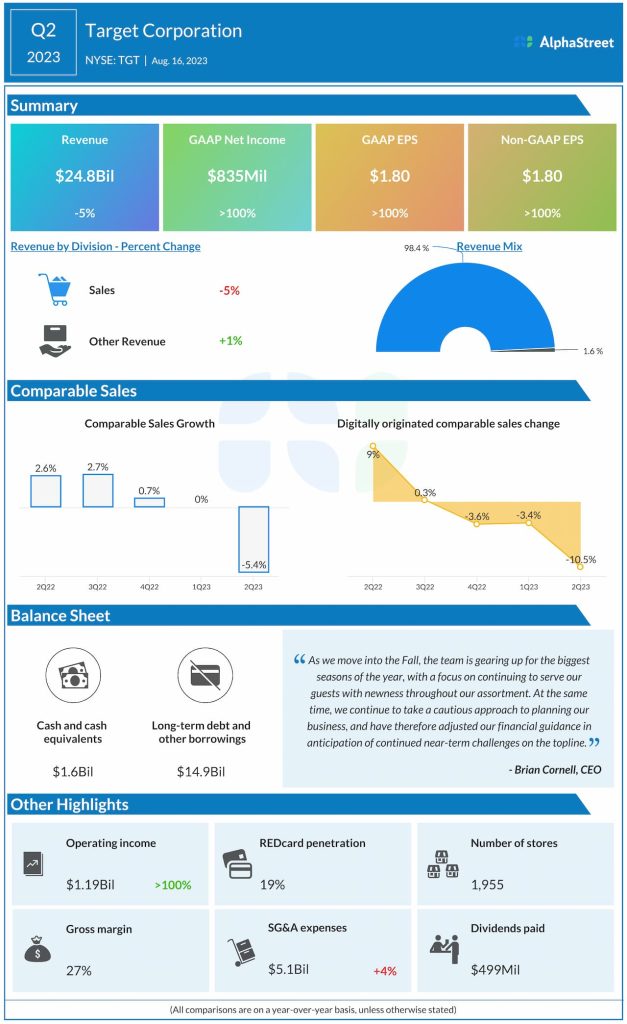

Target’s total revenue in Q2 2023 decreased 4.9% year-over-year to $24.8 billion, reflecting a sales decline of 4.9%. The top line number also missed market estimates. Comparable sales fell 5.4%, reflecting a decline of 4.3% in comparable store sales and a drop of 10.5% in comparable digital sales.

Guidance cut

On its quarterly conference call, Target said that the moderation of inflation rates is likely to put some pressure on dollar comps in frequency categories in the near term. The company expects comparable sales in a wide range centered around a mid-single-digit decline for the full year of 2023. It also lowered its outlook for GAAP and adjusted EPS to a range of $7-8 from the previous range of $7.75-8.75.

For the third quarter of 2023, Target expects comparable sales in a wide range around a mid-single digit decline, while GAAP and adjusted EPS are expected to range between $1.20-1.60.

Softness in discretionary and inventory shrink

During the second quarter, Target witnessed continued growth in its frequency categories, which was offset by softness in discretionary categories. As stated on its call, the impact of inflation in frequency categories like groceries and essentials as well as the shift in consumer spending towards services has put pressure on discretionary purchases. The rollback of pandemic support measures like stimulus payments are also putting pressure on customers.

Target also faces challenges from inventory shrink. Based on the high loss rates it is seeing, Q2 shrink was consistent with expectations. In Q3, the company expects dollar and rate pressure from shrink to be roughly consistent with the first half of the year at around 90 basis points. Over the long term, Target expects shrink rates to moderate from the current levels.