AbbVie, Inc. (NYSE: ABBV) has been recovering steadily from the virus-related slowdown and latest statistics show that the company’s performance has improved to pre-crisis levels in recent months. The pharmaceuticals firm owes the improvement mainly to its flagship arthritis drug Humira that witnessed stable demand despite facing biosimilar competition, mainly in the international market.

Also read: AbbVie Q3 2020 Earnings Call Transcript

The general disruption in the demand for prescription drugs, due to the shift in focus to coronavirus treatment, might affect the top-line until healthcare activities return to normal levels. On the positive side, revenues will benefit from AbbVie’s COVID-19 care efforts going forward, though Humira will stay in the spotlight, offsetting weakness in the Botox portfolio due to the pandemic-induced demand crunch. Also, contributions from Allergan, which joined the AbbVie-fold earlier this year, will add to the top-line.

COVID Care

While supporting clinics in their COVID care activities, AbbVie also looks to invest in consumer promotion to broaden the global aesthetics market that is believed to be under-penetrated. The consistent performance of its legacy products and the strong adoption of new drugs is a testament to the company’s strong fundamentals. As part of the NIH ACTIV program, immunology drug SKYRIZI will be evaluated as a potential treatment for COVID-19.

From AbbVie’s third-quarter 2020 earnings conference call:

“We’re already demonstrating that we have created a stronger, more diverse company with robust cash flows and multiple new growth vehicles for the long-term. And our pipeline is advancing nicely with numerous attractive late-stage programs that we believe will allow us to maintain a growing and vibrant business. We’re on track for the approval of more than a dozen new products for major indications over the next two years, which will collectively add meaningful revenue growth.”

Buy ABBV?

Analysts overwhelmingly recommend investing in ABBV as they see the market value expanding by more than a quarter in the next twelve months. A solid pipeline with several promising late-stage programs –complementing the high-growth arthritis portfolio — and the relatively low valuation should make the stock attractive to investors. Moreover, the management recently announced a double-digit increase in dividend from $1.18 per share to $1.30 per share.

Strong Q3

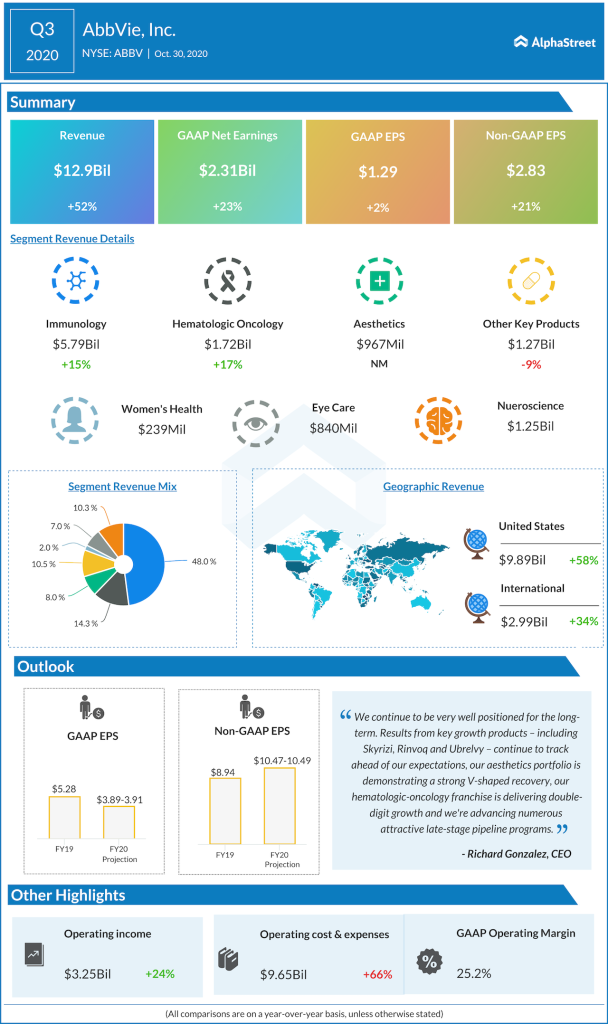

Immunology and Hematologic Oncology, which together account for more than half of total revenues, delivered double-digit growth in the third quarter. At $13 billion, total revenues were up 52%, also benefiting from synergies from the Allergan business. Consequently, adjusted earnings rose by a fifth to $2.83 per share and topped the Street view. Encouraged by the impressive outcome, the management forecasts that full-year earnings per share will be above the $10-mark.

Concerns over the continuing pressure on drug pricing will likely linger in the near future, prompting pharma companies like AbbVie to focus more on their pricing strategy. Meanwhile, there is speculation that the tax structure and pricing scenario would change after the election.

“As far as what our expectations would be in 2021, I think our expectations in 2021 from a price standpoint will be similar to what they were in ’19 and ’20, and that is we weren’t reliant on price. I mean, fortunately, our business is primarily a volume-driven business,” said AbbVie’s chief financial officer Richard Gonzalez while replying to analysts’ questions at the earnings call.

Stock Gains

Shares of AbbVie bounced back quickly from the virus-induced selloff in mid-march. They have maintained the momentum since then and closed the last session at the levels seen at the beginning of the year. The stock gained about 10% after losing steam prior to the latest quarterly report.