Conagra Brands, Inc. (NYSE: CAG), a leading provider of consumer-packaged goods, reported weaker-than-expected first-quarter results this week, with customers becoming increasingly budget-conscious amid elevated inflation. However, the company said it is on track to meet its targets for the full fiscal year. The market reacted negatively to the report and the company’s shares fell on Wednesday morning.

The stock had maintained a steady uptrend after recovering from a three-year low in early 2023, until this week’s earnings announcement that triggered a selloff. CAG has gained about 10% in the past twelve months but remains a relatively cheap stock. The company’s dominance in the packaged food market and the underlying momentum of the business should enable it to navigate the short-term headwinds and create strong shareholder value in the long term.

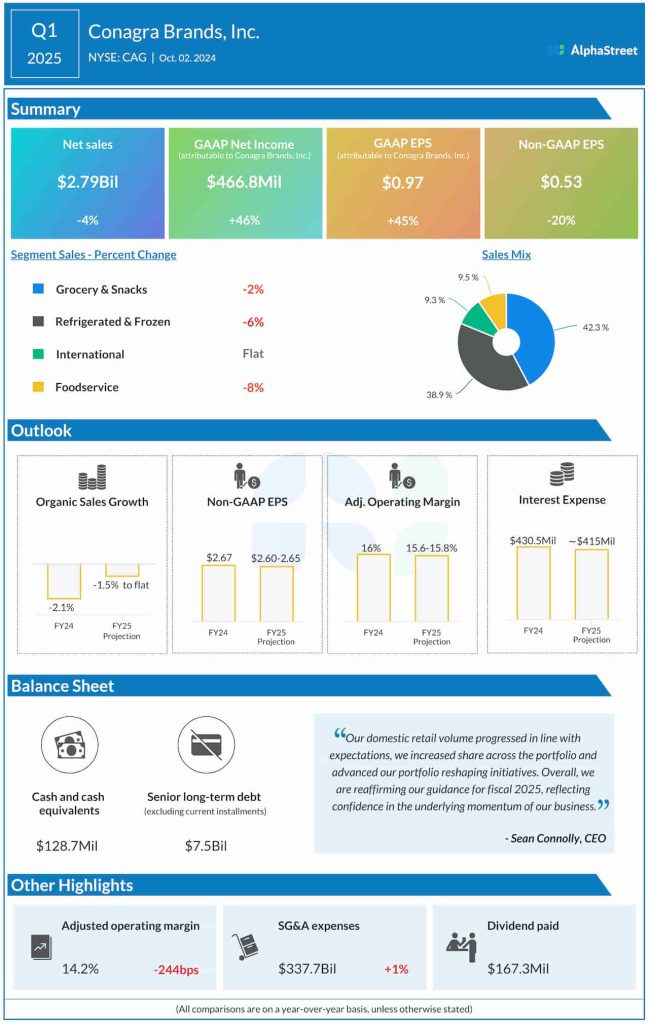

Slowdown

Conagra’s grocery and frozen foods segments experienced weakness in the early months of FY25, hurting the top line. It attributed the slowdown to unfavorable price/mix and production disruption at the Hebrew National business. Besides the sales slump, the bottom line was also impacted by cost inflation, on a comparable basis. Nevertheless, the company remains optimistic about future performance, and forecasts full-year earnings above analysts’ estimates.

Adjusted net income dropped to $0.53 per share in the first quarter from $0.66 per share in the year-ago quarter. Including special items, the company reported net income of $466.8 million or $0.97 per share for Q1, compared to $319.7 million or $0.67 per share in the same period of 2024. Earnings missed Wall Street’s projection for the first time in nearly three years.

Results Miss

Profit was negatively impacted by a 3.8% year-over-year decrease in net sales to $2.79 billion in the August quarter. The top line also fell short of Wall Street’s expectations. Organic net sales dropped 3.5%, hurt by lower volumes and negative impact from the price mix, mainly due to recent investments.

From Conagra Brands’ Q1 2025 Earnings Call:

“We do expect our absorption to start to moderate and get positive. That’s really important because absorption was a headwind in Q1. That tamped down our gross margins because volumes have been down. But as volumes inflect and get positive, we’ll start to see that as more of a tailwind than a headwind. So that’s a big part of our forecast. We talked about sales mix in Q1 being unfavorable. We expect that to normalize as we move forward as well. Our productivity, we are very pleased with that in Q1 and we expect that to continue to accelerate as we move forward.”

Guidance

The management reaffirmed its adjusted earnings guidance for the whole of fiscal 2025 in the range of $2.60 per share to $2.65 per share and continues to expect organic sales to be flat to down 1.5% annually. The full-year adjusted operating margin forecast was reaffirmed in the 15.6-15.8% range, and interest expenses guidance at $415 million. The company expects volumes to pick up going forward, driving margin recovery.

On Thursday, Conagra’s stock hovered near its 12-month average value. The shares have gained nearly 3% since the beginning of the year.