Intel Corporation (NASDAQ: INTC) reported a surprise profit for the June quarter, after posting its largest-ever loss in the prior quarter, even as the semiconductor giant’s revenues remain under pressure. Of late, the company has been facing stiff competition from the like of Advanced Micro Devices and Nvidia.

Intel’s stock got a much-needed boost after it released the Q2 report last week as the better-than-expected outcome lifted investor sentiment. The current price is the best so far this year and the stock is trading close to where it was a year ago. However, the uptrend is unlikely to continue for the remainder of the year.

New Chips

Intel would most probably regain the lost strength by next year when it is expected to launch new processors, which would enable the company to compete effectively with rivals, both in GPU and CPU. The 15th-generation Arrow Lake processors are supported by a speed-boosting technology that sends electrical power through chips. Meanwhile, there are concerns that Intel might lose some of its business to others like Nvidia which are better equipped to serve the surging demand for AI chips.

From Intel’s Q2 2023 earnings call transcript:

“We are strategically investing in manufacturing capacity to further advance our IDM 2.0 strategy and overarching foundry ambitions while adhering to our Smart Capital strategy. In Q2, we announced an expanded investment to build two leading-edge semiconductor facilities in Germany, as well as plans for a new assembling and test facility in Poland. The building out of Silicon Junction in Magdeburg is an important part of our go-forward strategy. And with our investment in Poland and the Ireland sites, we already operate at scale in the region.“

Results Beat

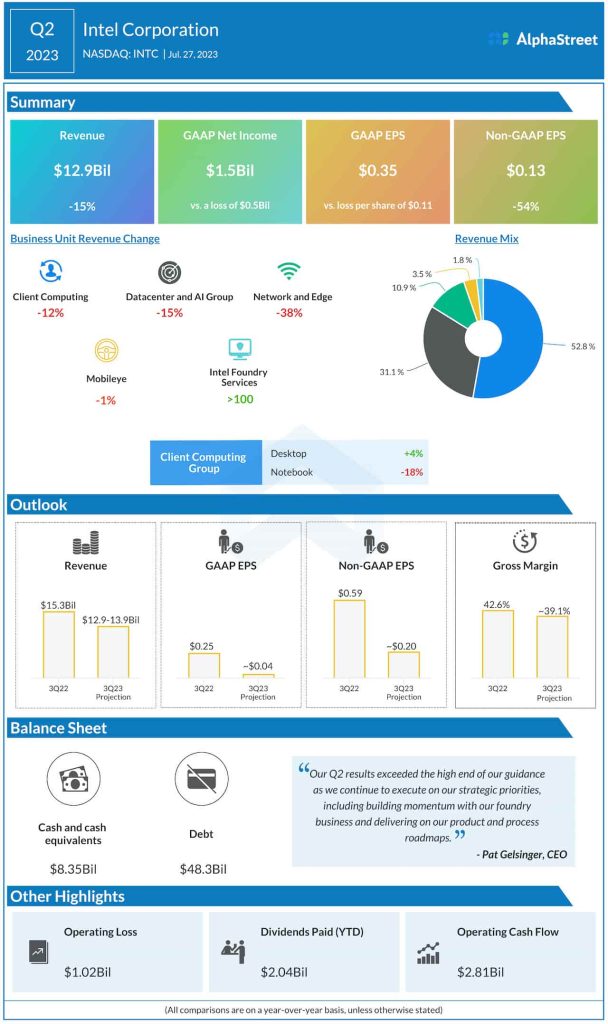

Intel’s profit, adjusted for one-off items, and revenues topped expectations for the second time in a row, after a big miss in the preceding quarter. In the latest quarter, earnings fell a dismal 53% to $0.13 per share. The bottom line was negatively impacted by a 15% fall in revenues to about $13 billion. All the main business divisions – Client Computing, Datacenter & AI Group, and Network & Edge – declined by double digits. However, the latest numbers came in above the management’s guidance.

On the revenue front, the only positive was an increase in the relatively new foundry business this time, but its revenue share is less than 2%. In a sign that the downturn would continue in the coming months, the management forecasts year-over-year declines for third-quarter profit, gross margin, and revenue. Interestingly, the guidance is above analysts’ estimates.

Intel’s stock maintained the post-earnings momentum since then but pared a part of those gains in the following sessions. It closed Monday’s session sharply lower.