Salesforce, Inc. (NYSE: CRM), the customer relationship management platform that delivered profitable growth in recent years, experienced a demand slowdown in the early part of fiscal 2025. The mixed start to the year, with modest topline performance and strong earnings growth, indicates that the deployment of artificial intelligence features across the platform is yet to translate into revenues.

Salesforce’s share price reached an all-time high in early March, more than doubling since the beginning of 2023. But, the shares suffered a dip soon after the first-quarter earnings report, reversing the momentum, as investors were disappointed by the revenue miss. Earlier this year, the company declared its first-ever quarterly cash dividend of $0.40 per share, to be paid on July 25, 2024.

Estimates

Salesforce will be publishing second-quarter 2025 earnings on Wednesday, August 28, at 4:00 pm ET. The management predicts adjusted profit in the $2.34-2.36 per share range and revenues between $9.20 billion and $9.25 billion. The guidance is above Wall Street’s earnings projection of $2.10 per share and top-line estimate of $8.24 billion. In the second quarter of 2024, the company reported earnings of $2.12 per share on revenues of $8.60 billion.

The tech firm’s leadership recently issued cautious full-year subscription and support growth guidance to reflect delays in executing large projects by customers. Currently, its growth strategy is focused on multi-cloud deals, international expansion, and data/AI innovations across the platform. Einstein, the AI-enabled smart assistant system designed to enhance customer experience, is widely used by customers across industries. The company is also expanding its footprint in international markets, with important client wins in Latin America, the Middle East/Africa, and Asia Pacific.

Stable Profitability

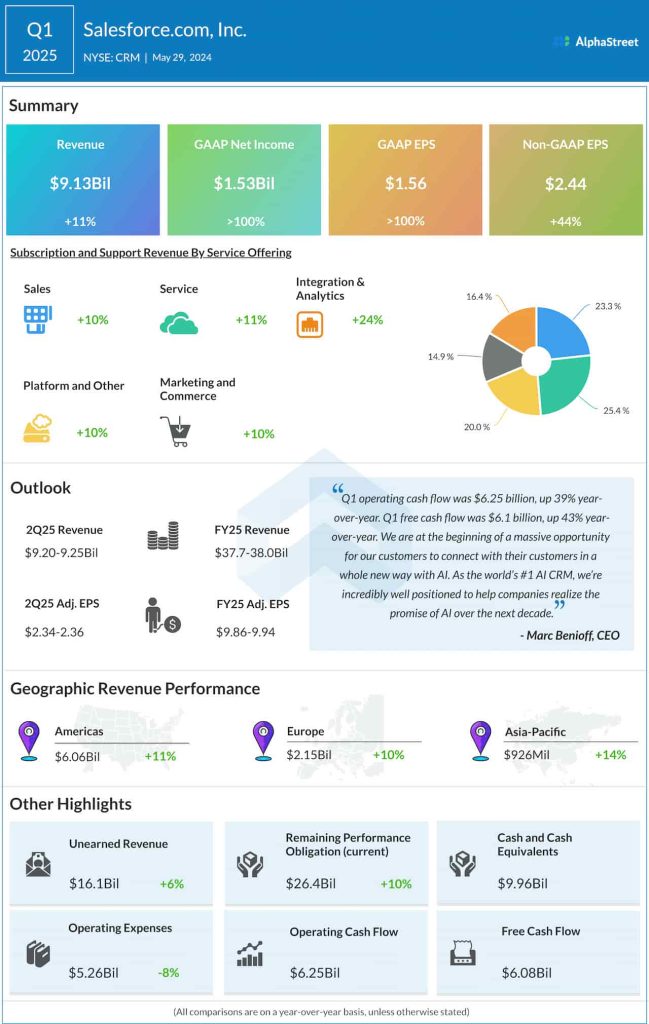

For more than a decade, Salesforce has consistently met or exceeded Wall Street’s quarterly profit projections, including in the first quarter of 2025. First-quarter profit jumped 44% annually to $2.44 per share, excluding special items. That was driven by double-digit revenue growth across all operating segments, resulting in an 11% rise in total revenues to $9.13 billion. The top line, however, fell short of expectations. The management’s full-year revenue and earnings estimates are $37.7-38.0 billion and $9.86-9.94 per share, respectively.

Commenting on the company’s AI strategy, CEO Marc Benioff said in a recent statement, “Now, we’re working with thousands of customers to power generative AI use cases with our Einstein Copilot, our prompt builder, our Einstein Studio, all of which went live in the first quarter. And we’ve closed hundreds of copilot deals since this incredible technology has gone GA. And in just the last few months, we’re seeing Einstein Copilot develop higher levels of capability. We are absolutely delighted and cannot be more excited about the success that we’re seeing with our customers with this great new capability.”

Partnership

Last month, the company signed a strategic partnership with Workday for a new AI employee service to help employees work smarter and faster. Salesforce’s new Agentforce Platform and Einstein AI, in combination with the Workday platform, will enable enterprises to create and manage agents for employee service use cases.

CRM has mostly recovered from the post-earning selloff a few months ago and is currently trading above its 12-month average. On Monday, the stock opened higher and made modest gains in the early half of the session.