Alaska Air Group Inc. (NYSE: ALK) reported fourth quarter 2025 adjusted earnings per share of $0.43, exceeding prior guidance expectations. The airline achieved single operating certificate status for Hawaiian Airlines and Alaska Airlines, marking the most significant integration milestone. Full-year 2025 adjusted earnings reached $2.44 per share with operating cash flow generation of $1.2 billion. The carrier announced its largest fleet order in company history, positioning for continued growth and profitability expansion under the Alaska Accelerate strategy.

MARKET POSITION AND COMPANY OVERVIEW

Alaska Air Group is one of the four major U.S. carriers, operating as a global airline serving network across North America and expanding international routes. The airline operates under the Alaska Airlines and Hawaiian Airlines brands following the September 2024 integration of Hawaiian Holdings. The company announced the largest fleet order in Alaska’s history in January 2026, with plans to expand to 475 aircraft by 2030 and over 550 aircraft by 2035. Alaska Air Group maintains a strong market position with premium travel experiences, enhanced loyalty program (Atmos Rewards), and diverse revenue streams.

LATEST QUARTERLY RESULTS — Q4 2025

Financial Performance Highlights

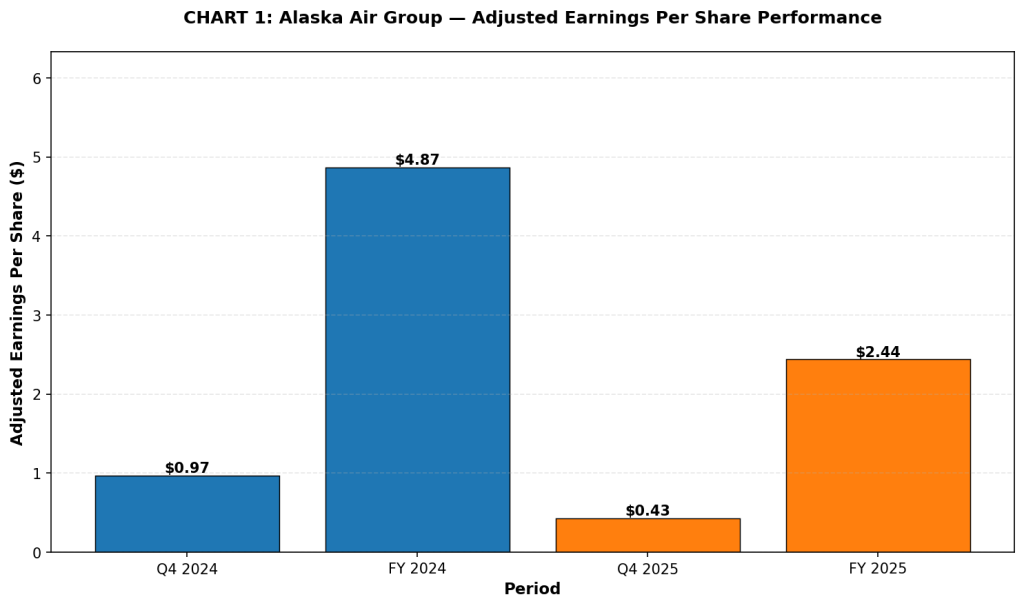

1. Adjusted Earnings Per Share: Q4 2025 adjusted earnings per share of $0.43, compared to $0.97 in the prior-year period. Full-year 2025 adjusted earnings reached $2.44 per share versus $4.87 in 2024. Reported GAAP net income was $21 million, or $0.18 per share for Q4 2025 and $100 million, or $0.83 per share for full-year 2025.

2. Revenue Performance: Q4 2025 revenue totaled $3.6 billion, resulting in 0.6% year-over-year RASM (revenue per available seat mile) increase. The carrier achieved positive unit revenue growth despite contending with temporary demand pullback from November government shutdown. Management believes Q4 unit revenue result ranked among the highest in the industry for the quarter.

3. Operating Margin: Q4 2025 reported pretax operating margin of 0.8% with adjusted pretax margin of 2.8% for full-year 2025. Unit costs excluding fuel, freighter costs, and special items increased 1.3% year-over-year, reflecting improved cost management and operational efficiency versus prior guidance.

4. Cash Generation and Capital Returns: Full-year 2025 operating cash flow generation reached $1.2 billion despite challenging economic backdrop. The airline repurchased 11.3 million shares for approximately $570 million during 2025, including 0.7 million shares for $30 million in Q4 2025.

Revenue Stream Diversification

Alaska Air Group demonstrated strong performance across diversified revenue streams during Q4 2025. Premium revenue increased 7% year-over-year, reflecting strong demand for premium cabin products and services. Cargo revenue increased 22% year-over-year, contributing meaningfully to overall operating profitability. Loyalty revenue increased 12% year-over-year, driven by record credit card acquisitions with nearly one-fourth of new signups being premium credit card products. Commercial initiatives and synergy capture remained on track for the fourth consecutive quarter.

Hawaiian Airlines Integration Progress

· Single Operating Certificate Achievement: Alaska and Hawaiian Airlines achieved single operating certificate status from the FAA, representing the most significant integration milestone. The carriers now operate as one airline in regulatory eyes, enabling streamlined operations and accelerated synergy realization across the combined entity.

· Operational Synergies: Commercial initiatives and synergy capture remained on track for the fourth consecutive quarter. The combined organization generated $1.2 billion in operating cash flow for full-year 2025, demonstrating successful integration execution despite challenging economic backdrop.

· Fleet Expansion Strategy: Alaska Air Group announced largest fleet order in company history in January 2026, including 105 Boeing 737-10 aircraft, 5 Boeing 787 aircraft, and options for 35 additional 737-10 aircraft. Fleet is scheduled to expand to 475 aircraft by 2030 and over 550 aircraft by 2035, supporting growth initiatives.

· Global Network Expansion: Commenced selling new international routes from Seattle to London and Rome, with first flights scheduled for spring 2026. The airline now sells in six foreign currencies with newly unveiled Japanese, Korean, and Italian-language websites, driving point-of-sale expansion outside the United States.

FINANCIAL TRENDS — CHARTS

The following charts present Alaska Air Group’s operating performance and financial trends.

Chart 1: Adjusted Earnings Per Share Trend

Note: Adjusted earnings per share excludes special items and other adjustments. Results demonstrate impact of Hawaiian Airlines integration on earnings profile.

Chart 2: Quarterly Revenue Comparison

Note: Q4 2025 revenue totaled $3.6 billion with 0.6% year-over-year RASM increase despite government shutdown headwinds. Management believes result ranked among highest in industry for the quarter.

BUSINESS & OPERATIONS UPDATE

· Fleet Modernization and Expansion: Alaska Air Group announced largest fleet order in company history with 105 Boeing 737-10, 5 Boeing 787, and options for 35 additional 737-10 aircraft. Took delivery of six 737-8 and one 787-9 aircraft in Q4 2025. Fleet expansion supports Alaska Accelerate strategy targeting $10 earnings per share in 2027. Unveiled new global livery for 787 fleet in January 2026, reflecting combined brand identity.

· Loyalty Program and Credit Card Innovation: Atmos Rewards loyalty program achieved 11-year streak as No. 1 airline loyalty program in customer satisfaction. Record credit card acquisitions achieved in Q4 2025, with nearly one-fourth of all signups for new premium credit card. Loyalty revenue increased 12% year-over-year, contributing to diversified revenue streams and customer engagement.

· International Route Expansion: Commenced selling new international routes from Seattle to London and Rome with first flights in spring 2026. Now selling in six foreign currencies with newly unveiled Japanese, Korean, and Italian-language websites. Point-of-sale expansion outside United States supports growth trajectory and premium customer acquisition.

· Corporate and Leisure Travel Demand: Corporate travel grew 9% year-over-year during Q4 2025, reflecting business confidence. Close-in demand remained strong throughout the quarter as bookings and yields continue to rebound from challenging earlier-year environment. Diverse customer base supports revenue stability across economic cycles.

HAWAIIAN AIRLINES INTEGRATION & SYNERGY CAPTURE

The combination of Alaska Airlines and Hawaiian Airlines achieved a critical integration milestone with single operating certificate approval from the FAA. This represents the most significant integration achievement to date, enabling Alaska and Hawaiian to operate as one airline in regulatory eyes. Commercial initiatives and synergy capture remained on track for the fourth consecutive quarter during Q4 2025. The integration progressed smoothly with strong execution across all operational areas, supporting cash flow generation and profitability objectives. The combined entity positions itself to compete effectively as one of four major U.S. global carriers.

COST MANAGEMENT & OPERATIONAL EFFICIENCY

Unit costs excluding fuel, freighter costs, and special items increased 1.3% year-over-year in Q4 2025, better than prior guidance and signaling teams’ renewed focus on cost control. The airline achieved cost savings across several areas of the business through enhanced cost management focus. Economic fuel cost per gallon averaged $2.57 for Q4 2025 as West Coast refining margins remained elevated throughout the quarter. Adjusted pretax margin reached 2.8% for full-year 2025, reflecting operational efficiency improvements despite challenging economic backdrop.

BALANCE SHEET STRENGTH & CAPITAL ALLOCATION

Alaska Air Group maintains strong balance sheet with debt-to-cap ratio of 61% and adjusted net debt to EBITDAR at 3.0x. Full-year 2025 operating cash flow generation reached $1.2 billion, demonstrating strong cash generation despite challenging economic environment. The airline returned capital to shareholders through share repurchase program, repurchasing 11.3 million shares for approximately $570 million during 2025. Capital expenditures expected in range of $1.4 to $1.5 billion for full-year 2026, supporting fleet modernization and strategic growth initiatives.

GUIDANCE AND OUTLOOK CONSIDERATIONS

· 2026 Capacity Growth: Capacity (ASMs) expected to increase 2% to 3% for full-year 2026, with Q1 2026 showing 1% to 2% growth. Growth supports Alaska Accelerate strategic initiative.

· 2026 Earnings Guidance: Full-year 2026 adjusted earnings per share guidance of $3.50 to $6.50. Q1 2026 adjusted earnings guidance of ($1.50) to ($0.50) per share, reflecting seasonal first quarter dynamics.

· Fleet Transformation: Largest fleet order in Alaska history announced January 2026 supports long-term growth strategy. Fleet expansion to 475 aircraft by 2030 and 550+ aircraft by 2035 positions for competitive advantage.

· Alaska Accelerate Strategy: Targets $10 earnings per share by 2027 enabled by $1 billion in incremental profit. Infrastructure investments support future growth and profitability expansion.

· Industry Position: Management believes Alaska Air Group positioned to compete as one of four major U.S. global airlines. Expanding global network and premium experiences support competitive market positioning.

PERFORMANCE SUMMARY

Alaska Air Group delivered strong Q4 2025 results with adjusted earnings per share of $0.43, exceeding prior guidance expectations. Full-year 2025 adjusted earnings reached $2.44 per share with $1.2 billion in operating cash flow generation. The airline achieved single operating certificate for Hawaiian Airlines and Alaska Airlines, the most significant integration milestone. Revenue performance with 0.6% year-over-year RASM growth ranked among industry highest for the fourth consecutive quarter. Commercial initiatives and synergy capture remained on track with 12% loyalty revenue growth and 22% cargo revenue growth. Fleet modernization and expansion announced in January 2026 positions the organization for long-term competitive advantage. Balance sheet strength with 61% debt-to-cap and strong cash generation supports capital allocation flexibility. Alaska Accelerate strategy targets $10 earnings per share by 2027 enabled by $1 billion in incremental profit. Management momentum accelerating in 2026 as the Alaska-Hawaiian combination gains full strength.