LEAD PARAGRAPH

Alcoa Corporation (NYSE: AA; ASX: AAI) reported fourth-quarter 2025 results on January 22, 2026. The Pittsburgh, Pennsylvania-based global industry leader in bauxite, alumina and aluminum reported consolidated net income of $226 million. The stock traded on both the New York Stock Exchange and the Australian Securities Exchange with moderate price movement. Market capitalization reflected strong operational performance across global production facilities.

MARKET CAPITALIZATION

As of January 22, 2026, Alcoa Corporation maintained a dual listing on the New York Stock Exchange (ticker: AA) and the Australian Securities Exchange (ticker: AAI). The company serves global markets as a diversified producer of bauxite, alumina and aluminum products with operations across multiple continents.

LATEST QUARTERLY RESULTS — Q4 2025

Consolidated Financial Performance

1. Total Revenue: Reported revenue of $3.4 billion, representing 15 percent sequential increase from third quarter 2025, reflecting higher aluminum and alumina shipments with improved pricing environment.

2. Net Income: Recorded net income of $226 million, or $0.85 per common share, reflecting operational improvements and aluminum pricing strength.

3. Adjusted EBITDA: Adjusted EBITDA excluding special items totaled $546 million, a sequential increase of $276 million primarily due to higher aluminum prices and carbon dioxide compensation recognition.

Year-Over-Year Comparison

Full year 2025 results demonstrated significant improvement versus prior year. Full year net income reached $1.2 billion compared to $60 million in 2024. Adjusted net income for 2025 increased to $1.0 billion. Revenue growth of 8 percent to $12.8 billion reflected higher aluminum prices and improved operational execution across segments.

Segment Highlights

· Alumina Segment: Produced and shipped alumina with third-party revenue of approximately $3.7 billion for full year 2025. Production increased 1 percent sequentially in fourth quarter. Supply chain optimization and external sourcing supported customer commitments. Average realized price per metric ton reflected commodity market dynamics.

· Aluminum Segment: Aluminum production increased 4 percent sequentially to 604,000 metric tons in fourth quarter, primarily due to progress on San Ciprián smelter restart in Spain. Full year aluminum production increased 5 percent with smelter restart initiatives at multiple facilities. Higher average realized aluminum prices improved segment performance.

· Bauxite Operations: Global bauxite production and sales contributed to integrated operations across Australian and other international operations. Third-party bauxite shipments and sales supported both internal alumina production and external customer commitments throughout 2025.

FINANCIAL TRENDS — CHARTS

The following charts present Alcoa’s quarterly revenue performance and adjusted EBITDA trends.

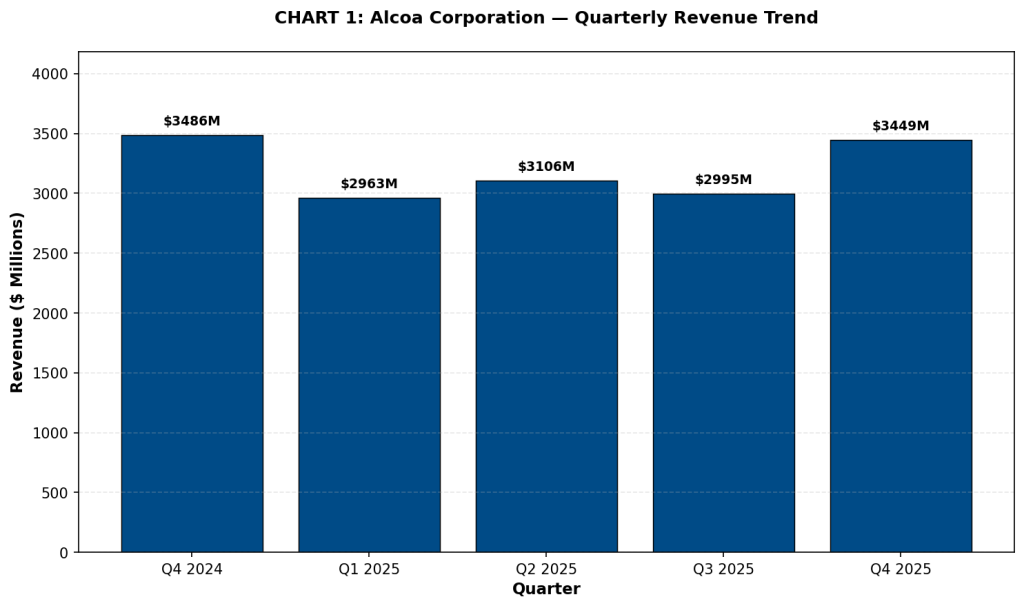

Chart 1: Quarterly Revenue Trend

Note: Revenue data represents total third-party sales across Alumina, Aluminum, and Bauxite segments. Q4 2025 revenue increased 15 percent sequentially from Q3 2025.

Chart 2: Adjusted EBITDA Trend (Excluding Special Items)

Note: Q4 2025 adjusted EBITDA increased $276 million sequentially from Q3 2025, primarily due to higher aluminum prices and carbon dioxide compensation recognition.

BUSINESS & OPERATIONS UPDATE

· Smelter Restart Progress: Alcoa advanced restart initiatives at San Ciprián smelter in Spain and other facilities. Aluminum production increased 4 percent sequentially with progress on multi-facility restart program. Operational execution reflected capital investment and strategic focus on capacity additions.

· Alumina Refinery Operations: Global alumina refineries operated across Australian and international locations. Production increased 1 percent sequentially with focus on productivity improvements. The company completed permanent closure of Kwinana refinery in Australia with managed transition.

· Commodity Market Environment: Aluminum pricing demonstrated strength throughout fourth quarter with average realized price of $3,749 per metric ton. Alumina pricing reflected commodity dynamics with average realized price of $341 per metric ton. Carbon dioxide compensation recognized in Spain and Norway operations improved financial results.

· Capital Allocation: Company generated $1.2 billion cash from operations during 2025 and reduced total debt to $2.4 billion. Capital expenditures totaled $618 million supporting smelter restart and productivity initiatives. Free cash flow reached $567 million for the year.

MERGERS, ACQUISITIONS & STRATEGIC DEVELOPMENTS

During 2025, Alcoa completed significant strategic initiatives. The company closed the sale of interest in the joint venture with Saudi Arabian Mining Company (Ma’aden), generating gains reflected in financial results. A favorable decision was received in an Australian tax dispute. The company formed a joint venture with IGNIS Equity Holdings, SL to support continued operation of the San Ciprián complex in Spain. These strategic initiatives supported value creation while maintaining operational focus on integrated production.

INSTITUTIONAL RESEARCH COVERAGE

Alcoa Corporation benefits from extensive research coverage from institutional investment analysts focusing on commodity producers. Analysts generally evaluate the company based on aluminum pricing trends, operational efficiency metrics, capital management strategies, and execution of smelter restart initiatives. Coverage emphasizes aluminum market dynamics, global supply-demand balances, and ESG considerations relevant to commodity industries. No specific equity research ratings or price targets are referenced within this factual report.

GUIDANCE AND OUTLOOK CONSIDERATIONS

· Alumina Production: 2026 guidance for total Alumina segment production ranges between 9.7 and 9.9 million metric tons, an increase from 2025 due to productivity improvements. Alumina shipments expected between 11.8 and 12.0 million metric tons.

· Aluminum Production: 2026 total Aluminum segment production expected to range between 2.4 and 2.6 million metric tons, an increase from 2025 due to smelter restart efforts. Aluminum shipments expected to range between 2.6 and 2.8 million metric tons.

· Q1 2026 Guidance: First quarter 2026 Alumina Segment Adjusted EBITDA expects sequential unfavorable impacts of $30 million due to maintenance cycles. Aluminum Segment Adjusted EBITDA expects sequential unfavorable impacts of $70 million due to absence of carbon dioxide compensation and San Ciprián restart costs.

· Commodity Pricing: Financial performance subject to aluminum and alumina commodity price volatility. Energy costs and global market conditions may impact operating margins and profitability.

PERFORMANCE SUMMARY

Alcoa Corporation achieved significant operational and financial improvements during 2025. Fourth quarter results reflected continued strength in aluminum pricing and operational execution across global facilities. Full year net income of $1.2 billion compared to prior year $60 million demonstrated substantial improvement. The company advanced strategic initiatives including smelter restart programs and portfolio optimization. Global production records were set at five aluminum smelters and one alumina refinery during 2025. Capital management remains disciplined with debt reduction and cash generation. Forward outlook reflects productivity improvements and continued execution of strategic initiatives within commodity market context.