For Chinese tech companies, 2022 was a tough year when business was hit by the government’s strict COVID restrictions and economic slowdown. Alibaba Group Holding Limited (NYSE: BABA), which is often referred to as China’s Amazon, was also affected, with the tightening regulatory environment and persistent supply chain hurdles adding to the problem.

The e-commerce behemoth’s US-listed stock has declined around 70% since peaking more than two years ago. After falling to a multi-year low last year, the shares shifted to recovery mode but failed to maintain the momentum. The weakness can be attributed to the continuing COVID-related uncertainties in China, the company’s primary market that is yet to come out of the grip of coronavirus.

In Recovery Mode

However, the market is reopening fast from the latest phase of the shutdown, after the authorities eased the zero COVID policy. Sales growth is expected to accelerate this year as the reopening gathers steam. The stock looks headed for a major upswing in the coming months, aided by the sales-driven rise in investor confidence. Those looking to invest in BABA might not get an opportunity to buy the stock cheaper this year. Long-term investors can look for decent returns, going by experts’ bullish views on the stock.

AMZN Earnings: All you need to know about Amazon’s Q4 2022 earnings results

The economy is showing signs of a rebound and regulatory curbs on the tech sector are easing. That could have a positive effect on revenues, and enable the company to achieve its goal of creating long-term, sustainable shareholder value. Alibaba’s sales, which almost flattened in mid-2022, should get a boost from the recovery in household consumption amid improving consumer sentiment.

The company’s cloud business remains a bright spot, given the growing demand for cloud services and the pandemic-induced digital transformation. At the same time, margins have started benefiting from the management’s efforts to improve profitability through initiatives like cost control and long-term investments in the business.

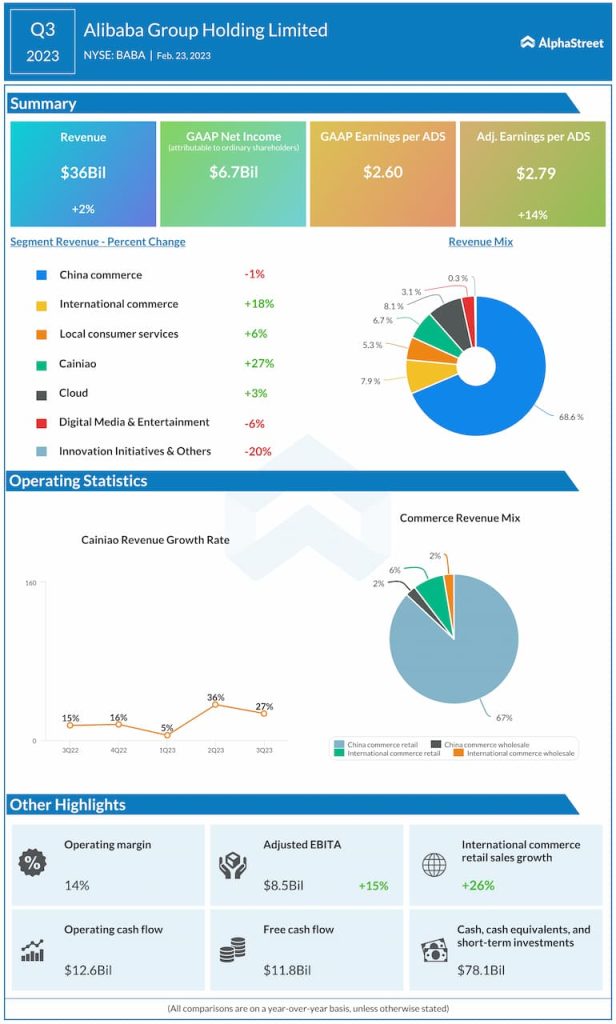

Earnings Beat

Alibaba’s profit, on a per-ADS basis, exceeded estimates for the fifth consecutive quarter while revenues topped the Street view for the third time. Third-quarter earnings increased 14% annually to $2.79 per ADS, driven by a 2% increase in revenues to $36 billion. Earnings beat estimates by a wide margin. Higher sales at the non-core business segments more than offset weakness in the core China Commerce division, which was hurt by a decline in the ‘marketing’ the company sells to merchants on the Taobao and Tmall e-commerce platforms.

Check this space to read management/analysts’ comments on quarterly reports

Commenting on the results, Alibaba’s CFO Toby Xu said, “during the past quarter, we continued to improve operating efficiency and cost optimization that resulted in robust profit growth. Our net cash position remains strong and we continue to generate healthy cash flow. During the quarter that ended December 31, 2022, we repurchased 45.4 million ADSs for approximately US$3.3 billion under our share repurchase program as part of our ongoing commitment to improving our shareholder return.”

Though BABA rallied on Thursday morning after the company posted stronger-than-expected third-quarter results, the momentum waned as trading progressed. The stock traded down 2% in the afternoon.