Taking a cue from the AI frenzy, Amazon.com Inc. (NASDAQ: AMZN) has adopted a growth strategy focused on expanding generative AI capabilities, through initiatives like the recent expansion of its collaboration with AI research firm Anthropic. While the e-commerce giant performed well across all business segments last year, Amazon Web Services stood out, delivering accelerated growth in quarterly sales.

Last month, Amazon’s shares reached a new high of $232.93. Market watchers foresee significant growth potential for the stock, which is expected to reach nearly the $250 mark this year. In 2024, the stock outperformed the industry and the S&P 500 index by a wide margin. Considering the company’s aggressive AI push, rapidly expanding cloud business, and improving efficiency in the retail business, AMZN looks like a compelling investment. However, the stock’s valuation appears to be relatively high.

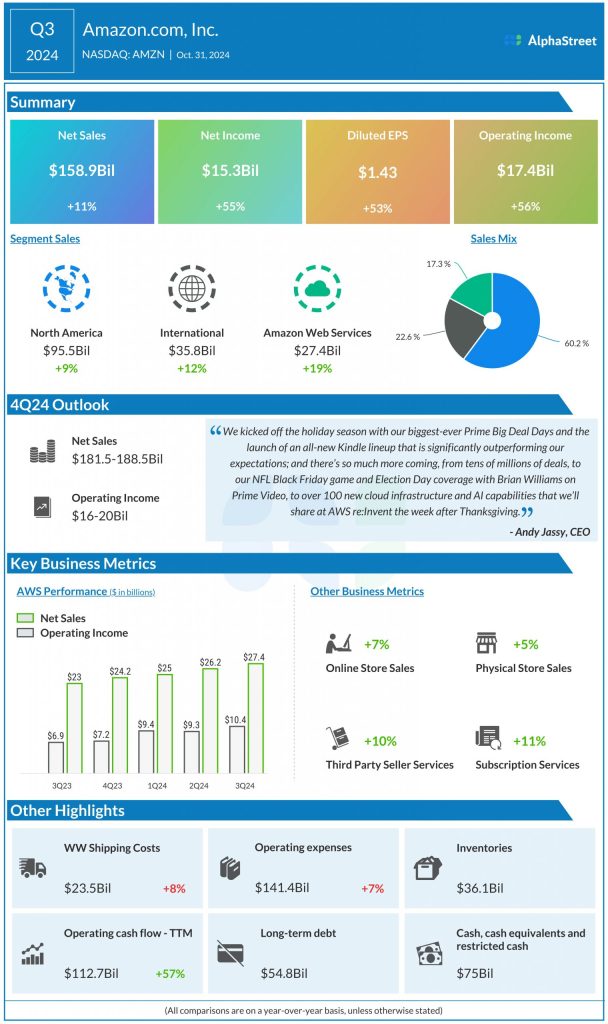

Strong Q3

In the third quarter, Amazon’s profit rose sharply to $15.3 billion or $1.43 per share from $9.9 billion or $0.94 per share in the year-ago period and topped expectations, marking the seventh consecutive beat. The bottom line benefitted from an 11% year-over-year increase in net sales to $158.9 billion. Sales in North America, the company’s largest market that accounts for more than 60% of its sales, grew 9%. The top line beat estimates, triggering a stock rally soon after the announcement.

From Amazon’s Q3 2024 earnings call:

“In the last few months, we’ve made hundreds of changes to our U.S. inbound network and opened more than 15 inbound buildings. While still relatively early in this re-architecture, we’ve already improved our ability to spread inventory across our fulfillment centers by 25% year over year, allowing us to have more of the requisite items in fulfillment centers closest to the customer so we can compile shipments and ship to customers even more quickly.”

Ad Power

Amazon has been revamping its retail business, especially in the domestic market, with a focus on improving efficiency and expanding its physical store network by incorporating facilities like same-day delivery and just-walk-out checkout. In e-commerce, the company is likely to maintain its dominance in the foreseeable future. Growing sales volumes and healthy cash flows allow it to invest heavily in other areas of the business.

The advertising business is growing steadily, with revenues increasing by double digits in recent quarters. AWS and advertising, the fastest-growing business segments, have contributed significantly to profits lately. Last year, the company expanded its strategic partnership with Nvidia to provide advanced infrastructure, software, and services to drive customers’ generative AI innovations.

Outlook

In the fourth quarter, the company expects net sales to be in the range of $181.5 billion to 188.5 billion, representing a 7-11% annual growth. The forecast for full-year operating income is between $16 billion and $20 billion. The Q4 report is scheduled for release on January 30, after the closing bell. Analysts forecast a double-digit year-over-year increase in sales and profit to $187.26 billion and $1.47 per share, respectively.

AMZN traded lower Tuesday morning after opening the session at $227.61, which is sharply above its long-term average price. The value increased by about 48% in 2024.