Advanced Micro Devices, Inc. (NASDAQ: AMD) is experiencing a steady increase in the demand for its artificial intelligence chips and processors for high-performance computing. However, the semiconductor firm’s performance in the stock market was not very impressive in 2024, mainly reflecting cautious outlook for the stock and weakness in non-core areas like the Gaming segment.

AMD’s stock has lost around 30% in the past six months, continuing the downtrend that began early last year. Market watchers are generally optimistic about the stock’s prospects, forecasting a 50% growth this year. Considering the relatively low valuation, after experiencing high volatility in recent years, AMD looks like a good long-term investment.

AI Push

The firm’s primary strength is its ability to innovate. By ramping up its AI processor portfolio, AMD is striving to catch up with market leaders like Nvidia, which enjoys an upper hand in the GPU space. The company looks well-positioned to tap into new opportunities in artificial intelligence, amid heavy enterprise spending on AI infrastructure.

It is worth noting that the chipmaker has significantly expanded its footprint in data center, grabbing market share from Intel and ending the latter’s prolonged dominance in the server chip market. Meanwhile, AMD is yet to meaningfully expand its market in other areas like gaming and CPU, where the company falls behind market leader Intel.

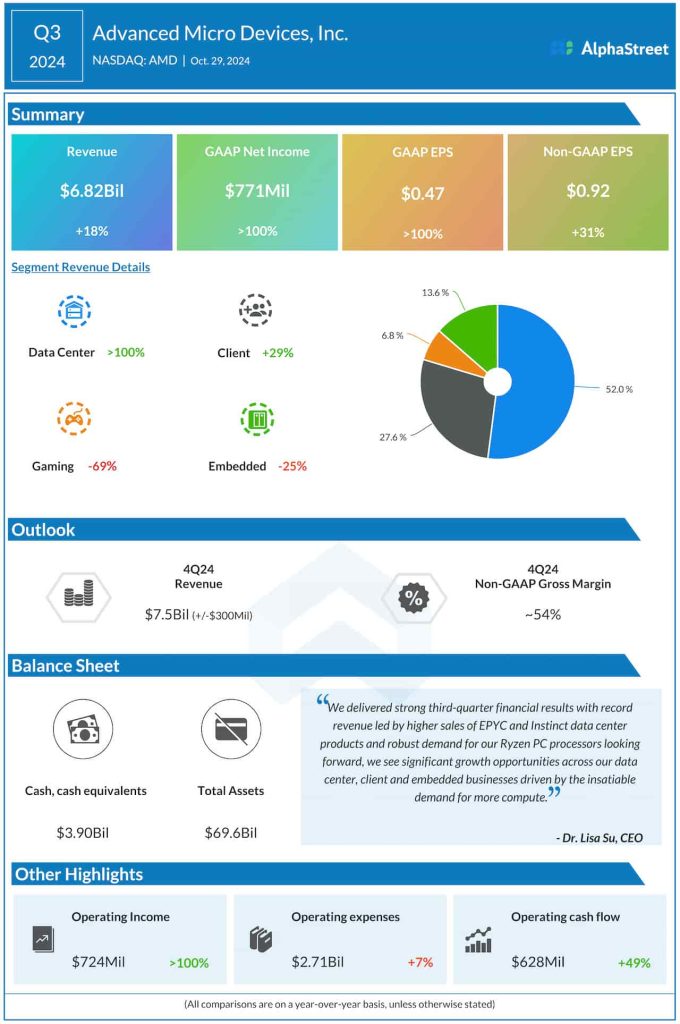

Guidance

The tech firm’s management targets a 20% growth in fourth-quarter revenue to approximately $7.5 billion — which is slightly below the market’s estimates — and forecasts an adjusted gross margin of around 54%. The company has raised its full-year revenue guidance for Data Center GPU from $4.5 billion to $5 billion, based on the completion of certain customer milestones. Recently, AMD joined hands with Dell to launch PCs powered by its Ryzen AI PRO chips.

Adjusted earnings rose to $0.92 per share in the third quarter of 2024 from $0.70 per share in the corresponding period in the prior year, matching analysts’ estimates. On a reported basis, net income was $771 million or $0.47 per share in Q3, compared to $299 million or $0.18 per share in Q3 2023.

Strong Revenues

The positive bottom-line performance reflected an 18% increase in revenues to $6.82 billion in the September quarter, vs. $5.8 billion in the prior year quarter, amid continued recovery in chip demand. The top line exceeded the market’s projection. Data Center revenue, representing around half of the total, more than doubled. The Client business, the second largest segment, grew by 29% in Q3.

Commenting on the Q3 results, AMD’s CEO Lisa Su said, “Looking ahead, we are very well positioned for continued growth in share gains based on the strength of our broad EPYC portfolio and the momentum we have built with cloud and enterprise customers. We also took a major step in the quarter to advance the x86 architecture, forming an ecosystem advisory group with Intel, several industry luminaries, and the largest cloud PC and enterprise leaders to accelerate innovation by driving consistency and compatibility across both the x86 instruction set and architectural interfaces …”

AMD shares traded lower in the early hours of Thursday, extending the weakness seen in the previous sessions. Hovering slightly above $120, the stock’s value is below its 52-week average.