AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Wall Street is looking for American Water Works Company to deliver $1.09 per share in earnings on $1.12B in revenue when the nation’s largest publicly traded water utility reports first-quarter 2026 results on April 30. Seven analysts cover the stock, with EPS estimates ranging from $1.05 to $1.16 and revenue projections tightly clustered between $1.11B and $1.12B. The narrow range on the top line reflects the regulated nature of the business, where revenue visibility remains high given multi-year rate case approvals and contracted customer bases.

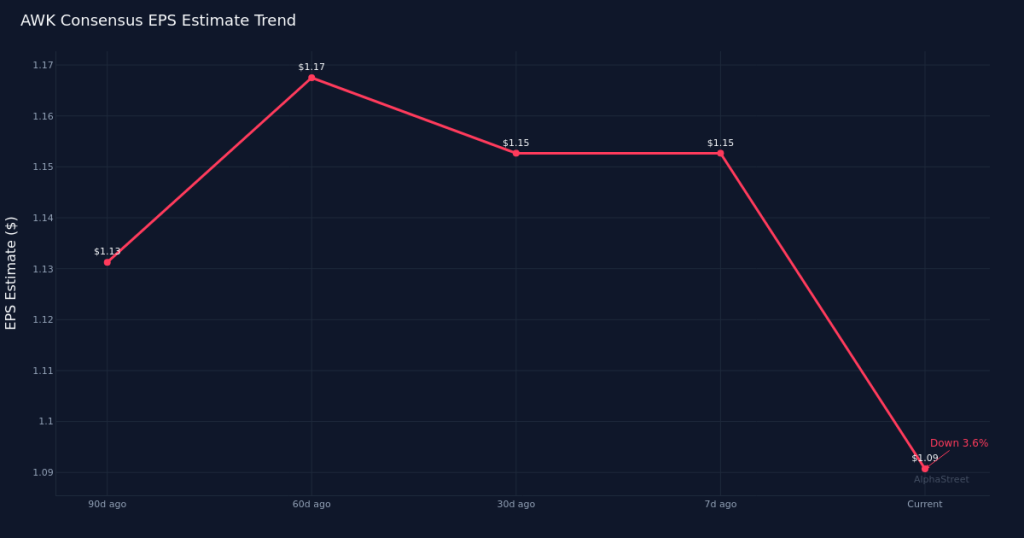

Analysts have grown more cautious heading into the print. The consensus EPS estimate has drifted down 5.2% over the past month from $1.15, and down 3.5% over the past three months from $1.13. The steady downward revision pattern suggests Wall Street is recalibrating expectations, possibly reflecting concerns about cost pressures, regulatory timing, or operational headwinds that have emerged as the quarter progressed. For a utility with predictable cash flows and transparent rate structures, this degree of estimate compression merits attention.

The year-over-year comparison shows modest earnings growth against a declining revenue base. Consensus calls for EPS to rise 6.9% from the $1.02 reported in the year-ago quarter, while revenue is expected to decline 1.8% from $1.14B in Q1 2025. That dynamic—earnings growth coupled with revenue contraction—points to margin expansion as the key driver of profitability. Last year’s first quarter produced $205.0M in net income and an 18.0% net margin, establishing the baseline for year-over-year comparisons. The ability to extract more profit from a smaller revenue base will hinge on whether rate increases and operational efficiencies can offset volume declines or customer mix shifts.

The revenue decline warrants particular focus in a sector typically characterized by steady, if unspectacular, growth. Water utilities generally benefit from contracted customer relationships and inflation-linked rate adjustments, making top-line contraction unusual absent portfolio divestitures or extraordinary weather impacts. Whether the expected decline reflects customer attrition, lower consumption driven by weather patterns, regulatory lag in implementing approved rate increases, or the disposition of non-core assets will be critical context for investors assessing the company’s organic growth trajectory.

Margin performance emerges as the pivotal narrative for this quarter. With revenue expected to move backward while earnings advance, the company must demonstrate that its rate case wins and cost management initiatives are more than offsetting volume pressures. The 18.0% net margin posted a year ago provides the benchmark—any expansion would validate the efficiency thesis, while compression could signal that inflationary costs in labor, chemicals, and infrastructure maintenance are outpacing the company’s ability to recover them through rates.

The stock’s positioning heading into the report will influence how investors react to any surprises. For regulated utilities, earnings volatility tends to be lower than for cyclical sectors, but estimate revisions and execution against rate case timelines can still drive meaningful share price movements. The market will be pricing in both the consensus figures and the recent negative estimate drift, meaning any upside surprise could be amplified if the company demonstrates that the caution was overdone.

Infrastructure investment levels and regulatory progress will command attention beyond the headline numbers. American Water operates in a capital-intensive industry where maintaining and upgrading aging water systems requires consistent spending. The balance between capital deployment, rate recovery, and return on equity will shape the investment thesis. Commentary on pending rate cases, approval timelines, and the regulatory environment across the company’s footprint will provide forward visibility that often matters more than a single quarter’s results.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.