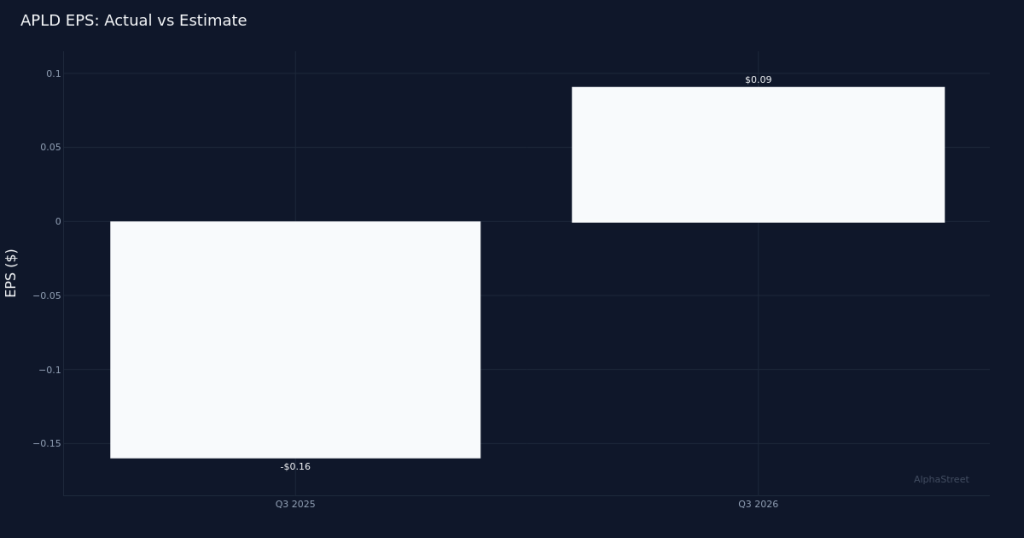

Applied Digital delivered a dramatic turnaround in Q3 2026, posting adjusted earnings of $0.09 per share versus a year-ago loss of $0.01 per share, marking a YoY change of +88%. Revenue surged +139% to $126.6M from $52.9M in the prior-year quarter, driven primarily by the company’s HPC Hosting segment which generated $71.0M. The stock rallied 10.4% to $27.79 on the results, reflecting investor enthusiasm for the top-line acceleration and return to profitability on an adjusted basis. Yet beneath the headline beat lies a more complex profitability story that warrants careful scrutiny.

The revenue trajectory shows genuine acceleration, with sequential momentum building across recent quarters. The four-quarter trend data shows Q3 2026 revenue of $126.6M versus Q3 2025 revenue of $52.9M, representing the +139% year-over-year change. This dramatic expansion reflects the company’s pivot toward high-performance computing hosting services, but the sustainability of this growth rate depends heavily on continued contract wins and capacity buildouts. Management’s commentary highlighted the magnitude of this shift: “We reported total revenues of $126.6 million, a 139% increase from the comparative prior quarter.” The company now operates 286 megawatts, providing scale context for the revenue generation, though the revenue-per-megawatt efficiency metrics would require additional operational disclosure to fully assess.

Segment dynamics reveal HPC Hosting as the dominant growth engine while legacy Data Center operations provide stability. HPC Hosting generated $71.0M, representing 56% of total revenue and clearly driving the overall growth narrative. Data Center Hosting, which management described as “our crypto data centers,” delivered $37.5M with 7.0% year-over-year growth—a more modest but consistent contributor. Management noted, “The Data Center segment, which operates our crypto data centers, had another strong quarter with $37.5 million in revenue, up 7% year-over-year.” Cloud Services rounded out the portfolio at $18.1M. The stark contrast between HPC’s explosive contribution and Data Center’s single-digit growth illustrates a business in transition, shifting mix toward higher-value AI and machine learning workloads and away from cryptocurrency mining hosting. The concentration risk in HPC cannot be ignored—any slowdown in that single segment would immediately pressure consolidated results.

The contracted revenue backlog provides unprecedented forward visibility, with $16B in commitments anchored by two major customers. Management revealed: “So today, we have $16 billion of total contracted revenue, and that splits $11 billion of CoreWeave and $5 billion to an investment-grade hyperscaler.” This backlog dwarfs the current quarterly run rate and represents years of revenue visibility, assuming successful execution on capacity builds and operational delivery. The concentration in just two customers—CoreWeave representing $11B and an unnamed hyperscaler contributing $5B—presents both opportunity and risk. While the hyperscaler contract adds an investment-grade counterparty to the mix, the CoreWeave relationship alone accounts for nearly 69% of the backlog. Management also indicated near-term lease prospects, noting “with Delta Forge 1, you should expect — I expect — I’ll say that, I expect a lease in the near term on that for hitting that goal,” suggesting additional capacity monetization ahead.

The stock’s 10.4% rally to $27.79 reflects optimism about the contracted backlog and capacity expansion, but the valuation now embeds significant execution risk. Investors are clearly looking past current profitability challenges and betting on the $16B backlog converting to sustainable, eventually profitable revenue. The market is rewarding the top-line momentum and the shift from quarterly losses to adjusted profitability, interpreting the SG&A explosion as investment in growth infrastructure rather than structural inefficiency. However, the stock reaction also suggests expectations are now elevated—any stumbles in capacity delivery, customer concentration issues, or continued margin pressure could trigger sharp reversals.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.