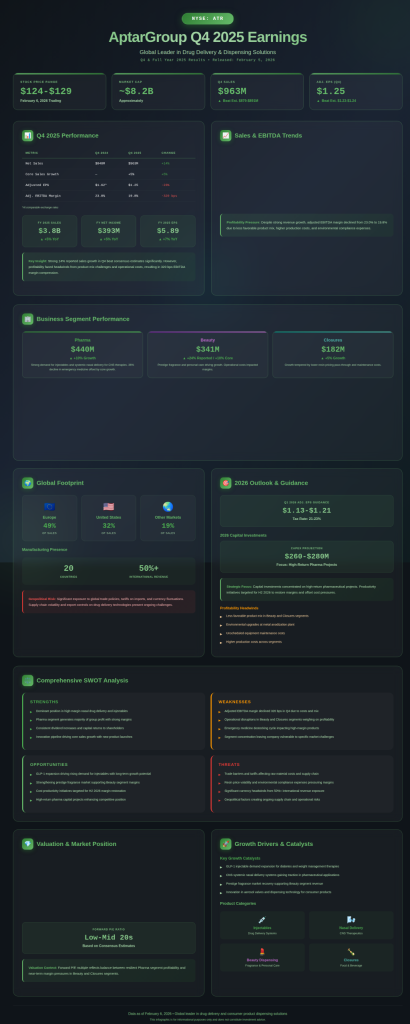

Shares of AptarGroup, Inc. (ATR) advanced modestly following the release of fourth-quarter and full-year 2025 results on February 5, 2026, with trading in the $123–$129 range on February 6. The stock remains within a recent range reflecting ongoing market dynamics. Investors focused on strong reported sales growth of 14% in the quarter, which offset profitability headwinds from product mix and operational costs in Beauty and Closures segments.

Company Description: AptarGroup is a global leader in drug delivery and consumer product dispensing solutions. The company operates three primary segments: Pharma, Beauty, and Closures, providing aerosol valves, pumps, and elastomer packaging components to the pharmaceutical, personal care, and food and beverage industries. With significant manufacturing footprints in 20 countries, Aptar derives approximately 49% of its sales from Europe and 32% from the United States.

Current Stock Price: ~$124–$129 (as of February 6, 2026 trading)

Market Capitalization: Approximately $8.1–$8.4 billion

Valuation: Aptar trades at a forward P/E ratio in the low-to-mid 20s range based on consensus estimates. This multiple reflects a balance between resilient Pharma segment profitability and near-term margin pressures in other segments.

Fourth Quarter and Full Year 2025 Financial Performance

Aptar reported fourth-quarter sales of $963 million, surpassing consensus estimates around $879–$891 million. Adjusted earnings per share (EPS) of $1.25 beat consensus of approximately $1.23–$1.24. For the full year 2025, reported sales rose 5% to $3.8 billion, while reported net income increased 5% to $393 million and EPS rose 7% to $5.89.

| Metric | Q4 2024 | Q4 2025 | YoY Change |

| Net Sales | $848M | $963M | +14% |

| Core Sales Growth | — | +5% | — |

| Adjusted EPS | $1.62* | $1.25 | -23% |

| Adj. EBITDA Margin | 23.0% | 19.8% | -320 bps |

*At comparable exchange rates.

Pharma Segment: Sales increased 10% to $440 million. Demand for injectables and systemic nasal delivery for CNS therapies offset a 36% decline in emergency medicine sales amid destocking.

Beauty Segment: Reported sales grew 24% to $341 million, with core growth of 10% in prestige fragrance and personal care.

Closures Segment: Sales rose 5% to $182 million, tempered by lower resin pricing pass-through.

Sector Pressures and Strategic Outlook

Profitability faced headwinds from less favorable product mix, higher production costs, environmental upgrades at a metal anodization plant, and unscheduled equipment maintenance in Beauty and Closures.

2026 Guidance: Aptar expects Q1 2026 adjusted EPS between $1.13 and $1.21, assuming an effective tax rate of 21% to 23%. Capital investments for the year are projected at $260 million to $280 million, focused on high-return pharma projects.

Geopolitical and Tariff Risk: Aptar faces exposure to global trade policies and raw material costs, including potential impacts from tariffs on imports and supply chain volatility. Over 50% of revenue is international, increasing sensitivity to currency fluctuations and export controls on drug delivery technologies.

AptarGroup (ATR) SWOT Analysis

Strengths

- Pharma Leadership: Dominant position in high-margin nasal drug delivery and injectables; Pharma generates the majority of group profit.

- Shareholder Returns: Consistent dividend increases and capital returns.

- Innovation Pipeline: New product launches drive core sales growth.

Weaknesses

- Margin Volatility: Adjusted EBITDA margin declined 320 bps in Q4 due to costs and mix.

- Segment Concentration: Operational disruptions in Beauty and Closures weighed on profitability.

- Emergency Medicine Cycle: Destocking in high-margin emergency products.

Opportunities

- GLP-1 Expansion: Rising demand for injectables provides long-term growth.

- Prestige Recovery: Strengthening fragrance market supports Beauty margins.

- Productivity Gains: Cost initiatives targeted for H2 2026 margin restoration.

Threats

- Trade Barriers: Tariffs and geopolitical factors affect raw material and supply chain costs.

- Raw Material Volatility: Resin price fluctuations and environmental compliance expenses.

- Currency Headwinds: Significant international exposure to translation risks.