Shares of Altria Group, Inc. (NYSE: MO) stayed green on Thursday. The stock has gained 8% over the past three months. The tobacco company is scheduled to report its earnings results for the third quarter of 2025 on Thursday, October 30, before market open. Here’s a look at what to expect from the earnings report:

Revenue

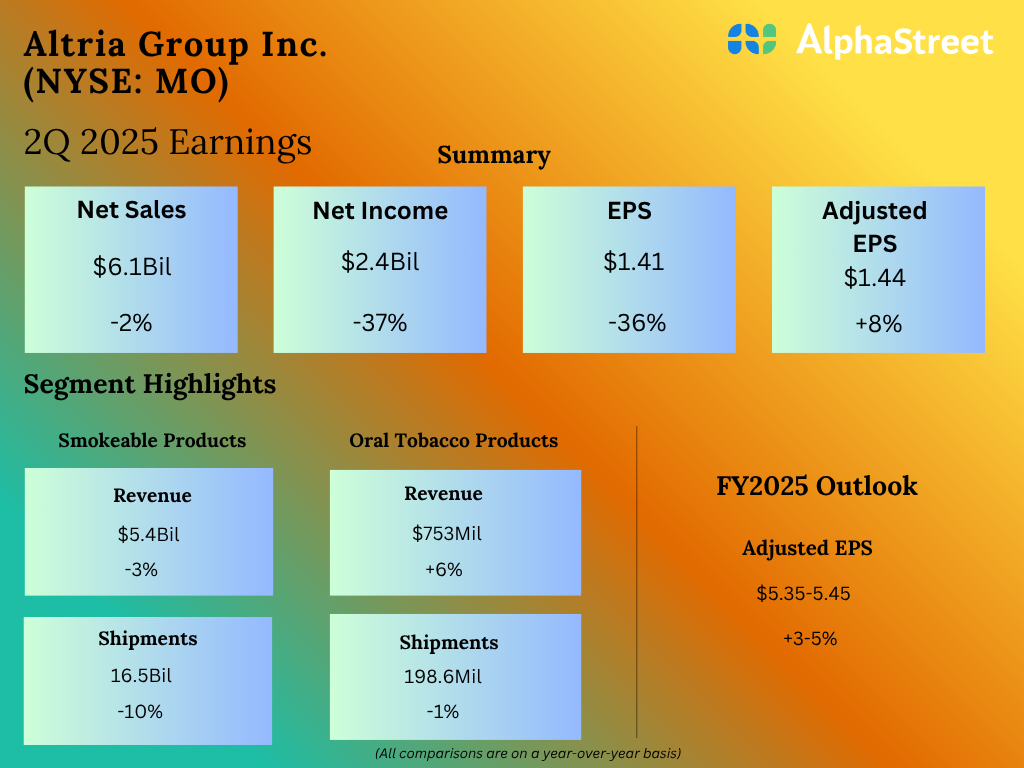

Analysts are projecting revenue of $5.31 billion for Altria in the third quarter of 2025. This indicates a slight dip from revenue of $5.34 billion reported in the third quarter of 2024. In the second quarter of 2025, revenues net of excise taxes rose slightly year-over-year to $5.3 billion.

Earnings

The consensus target for earnings per share in Q3 2025 is $1.45, which indicates an increase of nearly 5% from the year-ago period. In Q2 2025, adjusted EPS rose 8% YoY to $1.44.

Points to note

Altria is likely to continue facing challenges in its smokeable products segment due to continued volume declines. In Q2, domestic cigarette shipment volume decreased 10.2%, mainly due to a rise in illicit e-vapor products, and discretionary income pressures on customers.

Shipment volume of Marlboro and other premium brands fell double-digits last quarter, while inflationary pressures led to an increase in the discount segment, which saw volume growth in the double-digits. These trends may have continued in the third quarter.

Within its e-vapor business, Altria is working on a modified NJOY ACE solution that could help address the patent issues. It is also building a broader portfolio of vapor products that can cater to the changing demands of consumers.

Meanwhile the oral tobacco segment is performing well, led by on! nicotine pouches, which grew shipment volume by 26.5% in Q2, even as the other brands witnessed volume declines. Total US oral tobacco category share for on! nicotine pouches grew 0.7 share points to 8.7% in Q2. This segment is likely to have maintained its momentum in the third quarter.