The specialty ingredients manufacturer lowered the top end of its annual profit outlook citing operational delays and weather disruptions. First-quarter results showed declining sales across most segments, partially offset by resilient demand in pharmaceutical applications and improved cash flow generation.

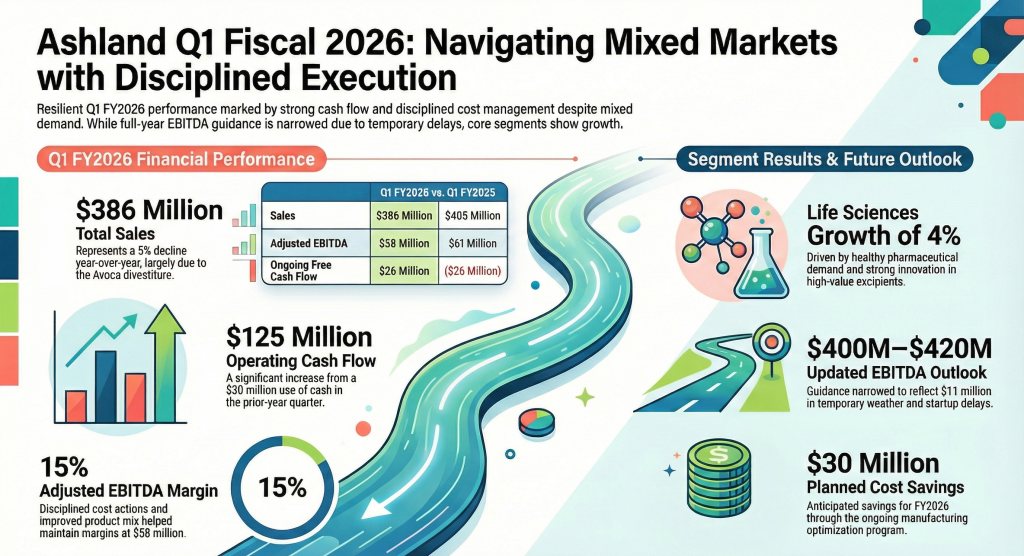

Ashland Inc. (NYSE: ASH) reported a net loss for the first quarter of fiscal 2026 and revised its full-year Adjusted EBITDA guidance downward at the top end. The company’s performance was impacted by the divestiture of its Avoca business and temporary operational hurdles, including a startup delay at its Calvert City facility. While overall sales declined 5% to $386 million, management identified signs of demand resilience in core consumer-focused segments and realized early benefits from restructuring and cost-optimization initiatives.

Updated Outlook Reflects Temporary Operational Impacts

The primary driver of the updated outlook is a narrowing of the fiscal 2026 Adjusted EBITDA guidance to a range of $400 million to $420 million, compared to the previous range of $400 million to $430 million. This adjustment reflects approximately $11 million in temporary impacts from the Calvert City startup delay and recent weather-related disruptions, both of which were isolated to the second quarter. Additionally, the divestiture of the Avoca business, completed previously, reduced first-quarter sales by approximately $10 million or 2%.

Financial Performance

For the quarter ended December 31, 2025, Ashland reported a net loss of $12 million, or $0.26 per diluted share, an improvement from a loss of $165 million in the prior-year period which was heavily impacted by a non-cash impairment charge. Adjusted EBITDA reached $58 million, representing a 15% margin, down 5% from $61 million a year ago.

Revenue performance varied by segment:

• Life Sciences: Sales rose 4% to $139 million, driven by higher volumes in pharmaceutical applications.

• Personal Care: Sales fell 8% to $123 million, primarily due to the Avoca divestiture; excluding that action, sales declined 1%.

• Specialty Additives: Sales dropped 11% to $102 million, reflecting weakness in global architectural coatings markets.

• Intermediates: Sales declined 6% to $31 million amid a persistently oversupplied market.

The company’s financial position was bolstered by a $103 million tax refund received in October 2025.

Cash flows from operating activities rose to $125 million, while ongoing free cash flow turned positive at $26 million, compared to a $26 million outflow in the prior-year quarter.

Business Outlook and Strategy

Management’s strategy focuses on expanding high-value globalized platforms, including biofunctional actives, microbial protection, and pharmaceutical excipients. The company is currently executing a manufacturing optimization program expected to yield $30 million in cost savings during fiscal 2026, as part of a total $90 million initiative. Capital expenditures for the full year are projected at approximately $100 million. The company anticipates a typical seasonal cadence for the remainder of the year, with stronger performance expected in the second half as commercial activity and operational efficiencies build.

Sector and Macro Trends

Ashland operates in a mixed macroeconomic environment where consumer-focused end markets like pharmaceuticals and personal care remain stable, while industrial sectors face ongoing pressure. The Life Sciences segment has moved past prior customer inventory control actions, leading to three consecutive quarters of volume gains. Conversely, the Specialty Additives segment continues to face headwinds from coatings weakness in China and North America, alongside competitive intensity in the Middle East, Africa, and India. The Intermediates segment remains in trough-like conditions due to oversupply in the butanediol (BDO) value chain.

Investment Thesis

Bull Case

• Resilient Core Segments: The Life Sciences division achieved an 11% increase in Adjusted EBITDA and a 22% margin, supported by robust demand for high-value cellulosic excipients and injectables.

• Operational Efficiency: Restructuring and cost-optimization efforts are beginning to impact the bottom line, with Adjusted Operating Income rising to $14 million from $11 million despite lower sales.

• Strong Cash Generation: The transition to positive ongoing free cash flow in a seasonally weak quarter, combined with a strengthened balance sheet from tax refunds, provides financial flexibility for disciplined capital allocation.

Bear Case

• Guidance Revision: The narrowing of EBITDA guidance due to the Calvert City delay and weather issues highlights the company’s vulnerability to unforeseen operational disruptions.

• Industrial Weakness: Persistent double-digit sales declines in Specialty Additives underscore the impact of a slow recovery in global housing and architectural coatings. • Pricing Pressures: Across several segments, carry-over adjustments and a competitive oversupplied market in Intermediates have led to pricing declines, which may continue to pressure margins if volumes do not recover significantly.