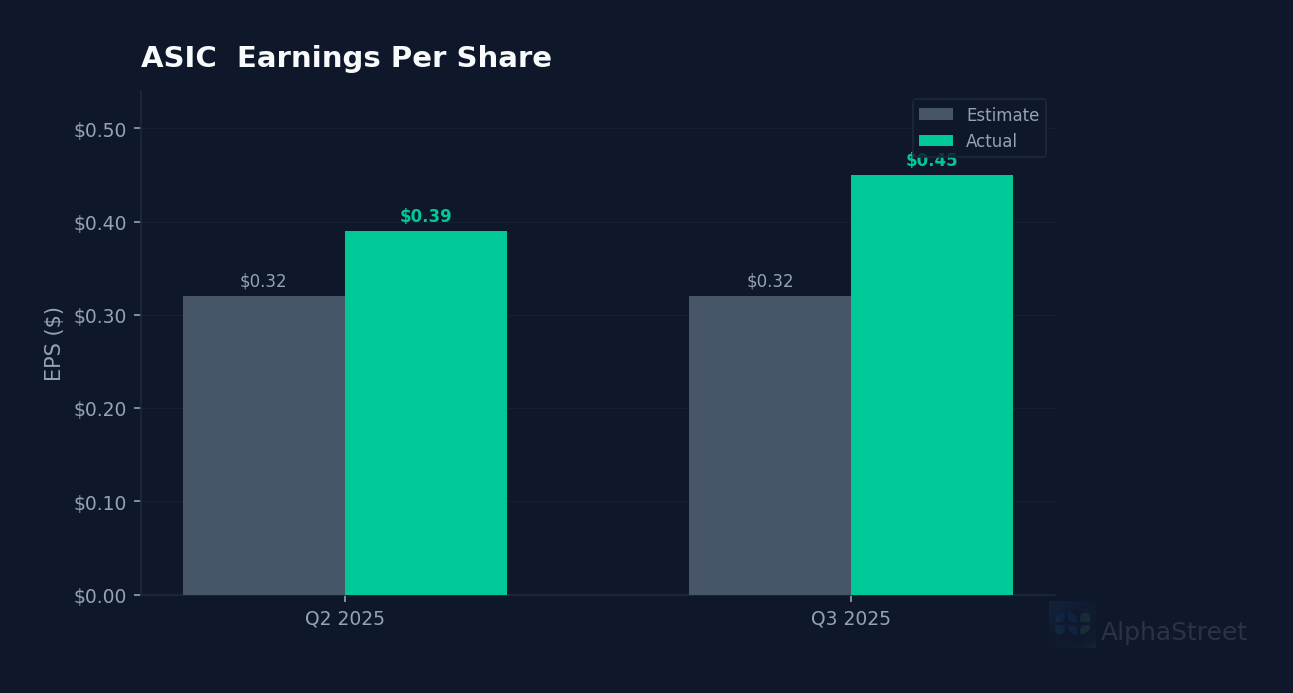

Market shrugs off massive beat. Ategrity Specialty Insurance Company Holdings (ASIC) posted Q4 2025 EPS of $0.45, crushing the $0.32 consensus by 40.6%. Despite the outsized earnings surprise, shares slipped 1.3% in after-hours trading to $17.53, extending the stock’s recent decline from its late-December peak of $21.48. The muted reaction suggests investors are focusing on valuation concerns after the specialty insurer’s remarkable run—revenue surged 30.8% year-over-year to $405.7 million.

Underwriting discipline drives margins. The company’s 17.3% profit margin and 25.9% operating margin reflect its differentiated approach in property and casualty insurance. Management highlighted during last quarter’s call that the strategy is “resonating in the current market,” with President Chris Schenck noting 30% top-line growth alongside margin expansion. CFO Neelam Patel pointed to “improving margins and higher investment income” as key drivers, with adjusted net income reaching $22.8 million in Q3 versus $12.9 million in the prior-year period.

Sequential momentum builds. The $405.7 million revenue figure for fiscal 2025 represents acceleration from the quarterly pace seen throughout the year. Q3 revenue hit $116.1 million, up from $101.8 million in Q2 and $88.7 million in the year-ago quarter—a consistent pattern of double-digit sequential gains. Net income followed the same trajectory, climbing from $4.9 million in Q2 2024 to $17.6 million in Q2 2025 and $22.7 million in Q3 2025.

Valuation gap persists. Trading at 12.2x trailing earnings and 9.5x forward earnings, ASIC remains well below the sector average despite consecutive quarters of 20%-plus EPS beats. The analyst target price of $25.60 implies 46% upside from current levels. The company’s book value expanded to $588.6 million by September 2025 from $398.3 million at year-end 2024, providing a strengthening foundation for further premium growth.

Growth trajectory intact. During Q3’s earnings call, analysts pressed management on whether the company could sustain growth “about 20% above the industry” through 2026 and beyond. While management declined to provide formal 2026 guidance, they affirmed “this is the way we think about the business.” With total assets reaching $1.45 billion—up 29% from $1.12 billion at the start of 2025—the company has the balance sheet capacity to maintain aggressive expansion in specialty lines.

This article was generated using AlphaStreet’s proprietary financial analysis technology and reviewed by our editorial team.