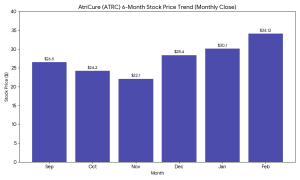

Shares of AtriCure, Inc. (Nasdaq: ATRC) rose 6.4% to $34.12 in Wednesday morning trading after the medical device maker reported fourth-quarter earnings that swung to a profit and exceeded analyst expectations for revenue.

The stock has traded in a 52-week range of $21.45 to $38.90. Today’s advance continues a recovery trend from mid-2025 lows, though the shares remain approximately 12% below their yearly peak as the medical technology sector faces broader pressure from volatile hospital capital equipment budgets.

Quarterly and Full-year Performance

AtriCure reported fourth-quarter worldwide revenue of $140.5 million, a 13.1% increase compared to $124.2 million in the same period last year. U.S. revenue climbed 12.6% to $114.3 million, driven by demand for the cryoSPHERE MAX probe and AtriClip FLEX-Mini appendage management device. International revenue grew 15.3% to $26.2 million.

The company posted fourth-quarter net income of $1.8 million, or $0.04 per diluted share, compared to a net loss of $15.6 million, or $0.33 per share, in the prior-year quarter. Adjusted EBITDA rose to $19.9 million from $12.7 million a year ago. Gross margin for the quarter was 75.0%, up 45 basis points year-over-year, supported by a more favorable product mix.

For the full year 2025, total revenue reached $534.5 million, representing 14.9% growth over 2024. The annual net loss narrowed significantly to $11.4 million, compared to a loss of $44.7 million in the previous year.

Sector Context

While AtriCure operates in the med-tech space, its valuation remains sensitive to macro pressures affecting high-growth “SaaS-adjacent” technology stocks. High interest rates have continued to weigh on growth-oriented equities, leading to tighter valuation multiples across the software and medical technology sectors. Despite these pressures, AtriCure management issued 2026 guidance projecting full-year revenue of $600 million to $610 million, representing approximately 12% to 14% growth.

Operational Outlook

Management attributed the improved profitability to operational leverage and cost efficiencies. The company ended 2025 with a stronger balance sheet, positioning it to fund ongoing clinical trials, including the LeAAPs and BoxX-NoAF studies.

However, the company remains subject to regulatory and competitive risks. Any shifts in FDA clearance timelines for new product iterations or increased competition from catheter-based technologies could impact its 2026 growth targets. Management expects continued positive cash generation through 2026.