T|EPS $0.57 vs $0.55 est (+3.6%)|Rev $31.51B vs $31.24B est (+0.9%)|Net Income $3.80B

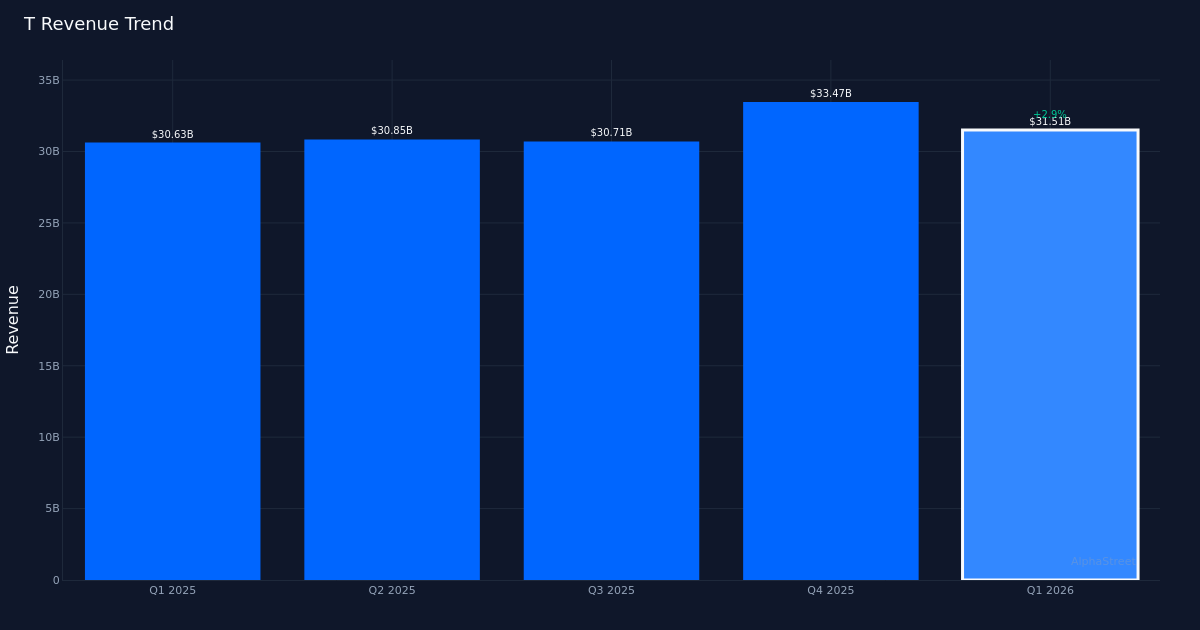

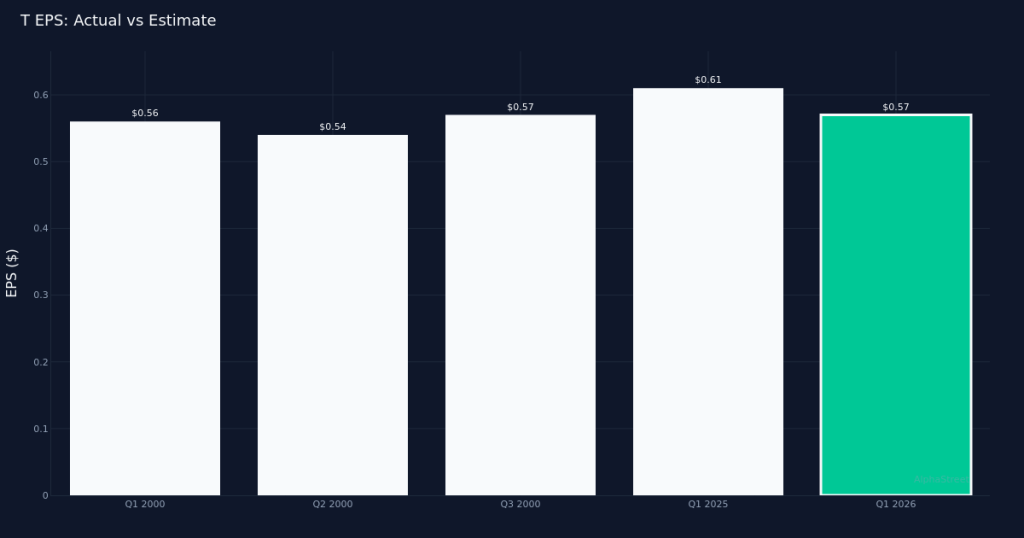

T|EPS $0.57 vs $0.55 est (+3.6%)|Rev $31.51B vs $31.24B est (+0.9%)|Net Income $3.80BSolid beat. AT&T Inc. (NYSE:T) delivered Q1 2026 adjusted EPS of $0.57, surpassing Wall Street’s $0.55 estimate by 3.6% based on projections from 17 analysts. Revenue reached $31.51B, climbing 0.9% above the $31.24B consensus and marking a 2.9% increase from the $30.63B recorded in Q1 2025. Net income reached $3.8B for the quarter, demonstrating the telecom giant’s ability to convert top-line growth into bottom-line profitability. The earnings beat appears fundamentally sound, driven by genuine revenue expansion rather than cost-cutting maneuvers, which should provide institutional investors confidence in the sustainability of results.

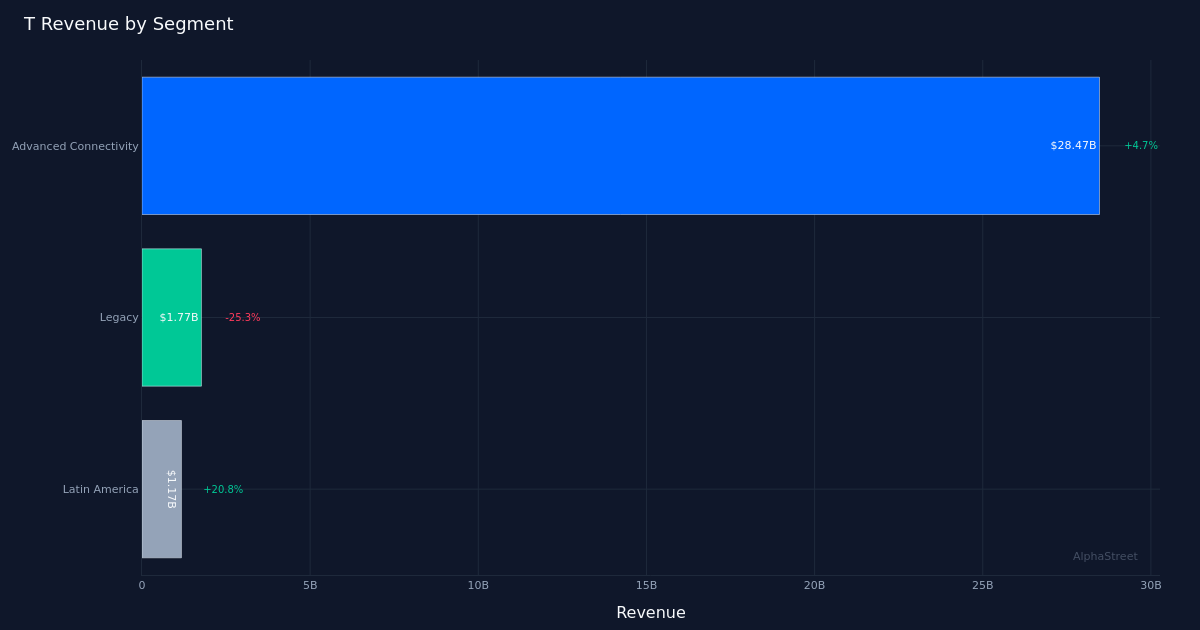

Fiber momentum continues. The company’s Advanced Connectivity segment led performance with $28.47B in revenue, up 4.7% year-over-year, underscoring strength in AT&T’s core infrastructure business. Internet net adds reached 584,000 units for the quarter, reflecting continued customer acquisition momentum in the company’s fiber buildout strategy. The telecom operator now reaches 37M total fiber locations at quarter end, expanding its addressable market for high-margin broadband services. This operational metric demonstrates management’s execution on its capital-intensive fiber deployment plan, positioning AT&T to capture share in the lucrative residential and business connectivity markets.

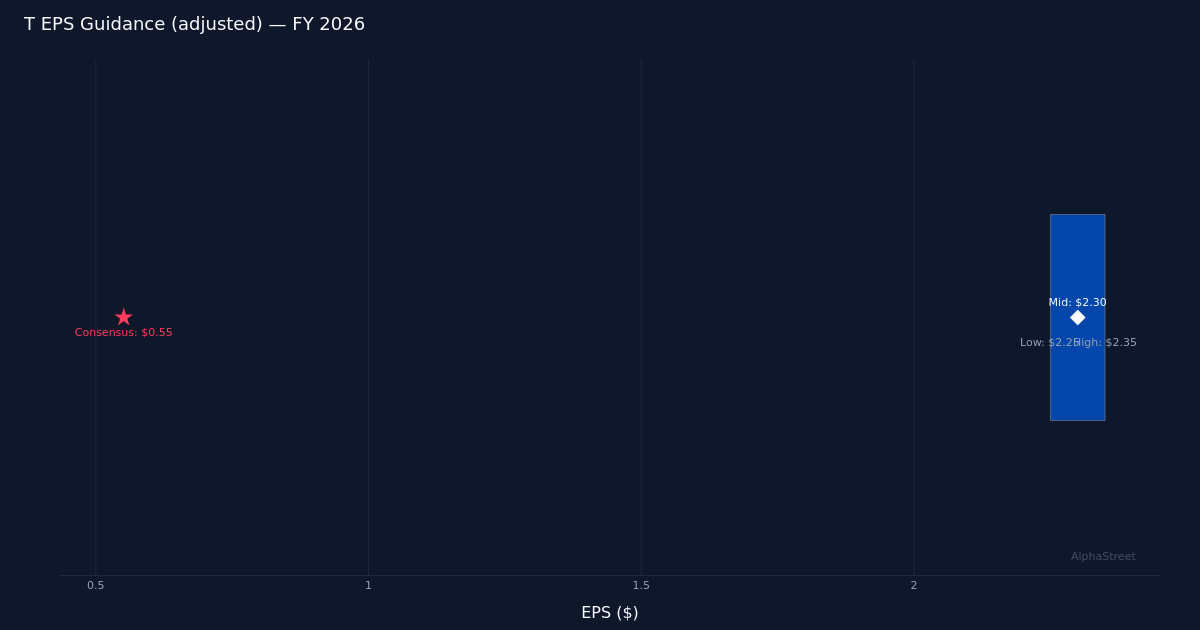

Conservative guidance. Management expects FY 2026 adjusted EPS of $2.25 to $2.35, providing investors with a roadmap for full-year expectations. At the midpoint of $2.30, this guidance suggests management anticipates steady performance through the remaining three quarters, though the range leaves room for quarterly fluctuations in a competitive telecom landscape. The guidance framework will be critical for investors modeling cash flow generation and dividend sustainability, particularly given AT&T’s historical focus on returning capital to shareholders through its dividend program.

Muted market reaction. Despite the earnings beat and revenue growth, shares traded at $25.35, down 2% following the report. The negative price action suggests investors may be digesting the full-year guidance range or concerned about competitive dynamics in the telecom sector that could pressure margins. Wall Street consensus currently stands at 12 buy ratings and 13 hold ratings with 0 sell recommendations, indicating a balanced but slightly cautious view on the stock’s near-term prospects. The mixed sentiment reflects ongoing debates about AT&T’s growth trajectory relative to its capital expenditure requirements and leverage profile.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.