AlphaStreet Newsdesk powered by AlphaStreet Intelligence

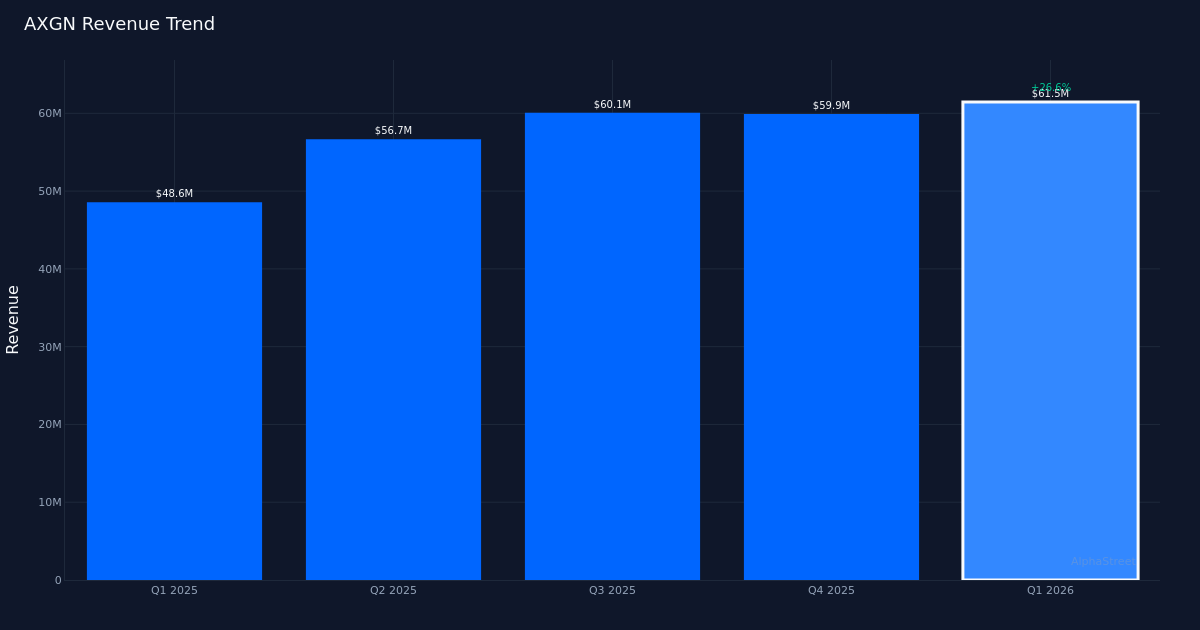

In-Line Quarter. Axogen, Inc. (NASDAQ: AXGN) delivered Q1 2026 adjusted EPS of $0.07, meeting the Street’s $0.07 estimate, as the medical device company posted solid revenue growth and maintained profitability in its peripheral nerve repair franchise. Revenue totaled $61.5M for the quarter, up 26.6% from $48.6M in Q1 2025, reflecting continued adoption of the company’s nerve reconstruction portfolio. Adjusted net income reached $4.1M for the quarter, demonstrating the company’s ability to convert strong top-line momentum into bottom-line results. The stock traded largely unchanged following the report, suggesting investors had largely anticipated the in-line performance.

Revenue-Driven Growth. The quality of Axogen’s quarter appears robust, with the 26.6% year-over-year revenue expansion driving results rather than relying on cost-cutting measures. This organic growth trajectory in the medical device space is particularly noteworthy as it reflects underlying demand for the company’s peripheral nerve repair solutions. The company maintained a gross margin of 75.2% for the quarter, indicating strong pricing power and operational efficiency in manufacturing its nerve graft and repair products. This margin profile provides substantial leverage as the company scales, allowing revenue growth to flow through to profitability while preserving room for continued investment in commercial expansion and product development.

Full-Year Outlook. Management provided full-year revenue guidance of $270.0M, establishing a clear target for fiscal 2026 performance. This guidance framework gives investors visibility into management’s expectations for sustained growth momentum throughout the year, though the company did not specify an upper bound for the range. The revenue target will serve as a key benchmark for investors monitoring Axogen’s ability to maintain its growth trajectory in the peripheral nerve repair market, particularly as the company navigates broader medical device market dynamics and reimbursement considerations that can impact procedure volumes.

Street Sentiment. Wall Street remains decidedly positive on Axogen’s prospects, with analyst consensus standing at 11 buy ratings, 1 hold, and 0 sell recommendations. This overwhelming bullish tilt reflects confidence in the company’s market position within peripheral nerve reconstruction, a niche but growing segment of the medical device industry where Axogen has established meaningful differentiation. The lack of any sell ratings suggests analysts view the current valuation and growth trajectory as sustainable, even as the company transitions from high-growth emerging player to more established commercial-stage operator.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.