The coronavirus outbreak came as a major blow to American Express Company (NYSE: AXP) as the travel restrictions resulted in widespread flight cancellations and hotel closures. But things changed for the better this year as disruptions eased amid market reopening, and the payment services provider looks well-equipped to deal with the macro headwinds.

Shares of the Buffalo-based credit card company peaked in the early weeks of the year, but soon entered a volatile phase. Nevertheless, they outperformed the sector and the S&P 500 quite often during that period. The stakeholders will be closely following the upcoming earnings report, looking for cues on the company’s post-pandemic prospects. While a section of analysts is cautious in their recommendations, there are many who believe AXP is a good long-term bet. That said, it is advisable to wait until the earnings release as it would help prospective investors take informed decisions.

Bullish on AXP

It is worth noting that Warrant Buffett has held on to his near-20% stake in American Express even during times of uncertainty, thanks to the company’s strong fundamentals and growing market share. While most of its peers struggled with high loan losses during the crisis, the losses of American Express remained relatively low because the company mainly caters to higher-income customers.

American Express Company Q2 2022 Earnings Call Transcript

The company’s extensive exposure to the aviation and tourism market has enabled it to stand out among peers, while creating a consistent revenue stream. However, the company hardly faces any direct competition due to its distinct business model – existing rivals Mastercard Inc. (NYSE: MA) and Visa Inc. (NYSE: V) do not finance credit card transactions directly, rather they operate as intermediaries. Also, the brand power and differentiated products of American Express are strong enough to act as a barrier for new entrants.

Good Show

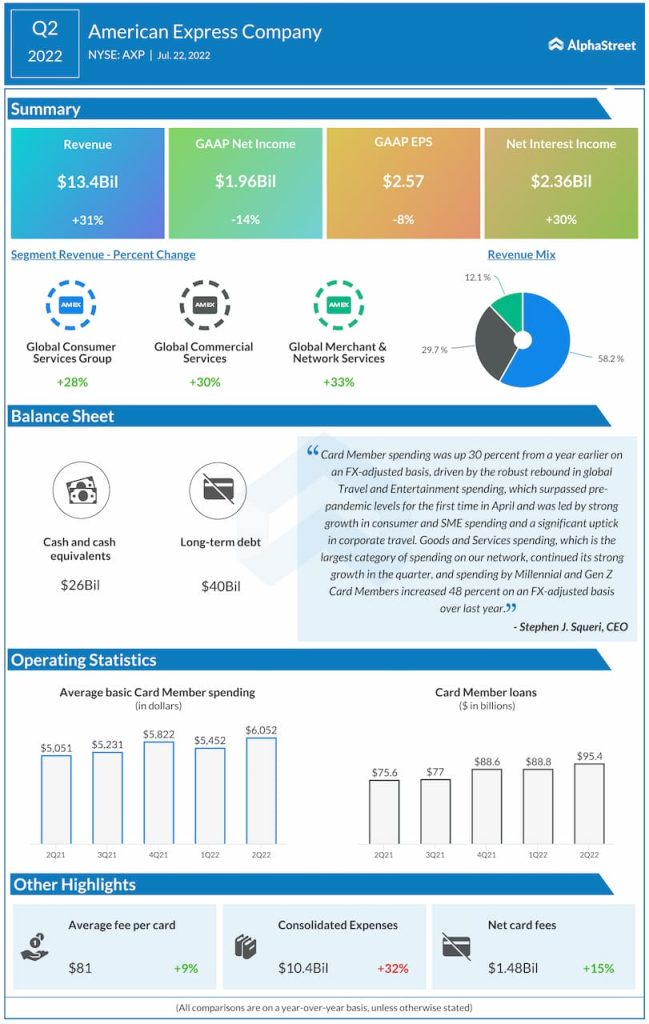

Another factor that gives the company an edge is the full-fledged payments network, an additional revenue stream that allows it to effectively deal with potential headwinds to the core business. Over the past five years, every quarter it generated strong net profit that exceeded the forecast. In the most recent quarter, the top line also surpassed consensus estimates, continuing the recent trend. Second-quarter earnings, however, dropped 8% annually to $2.57 per share despite a 31% increase in revenues to $13.4 billion.

From American Express’ Q2 2022 earnings conference call:

“Looking forward, as I’ve emphasized many times before, we run the company for the long term and our investment strategy is grounded in this principle. As we sit here today, we have an abundance of great opportunities and we will continue to make our decisions with a longer-term view like we did during the pandemic. That means we will continue to invest at high levels in those areas that will drive sustainable growth, including our brand, value propositions, customers, colleagues, technology, and coverage.”

Q3 Earnings on Tap

The management has been on a hiring spree this year. Last month, it revealed plans to expand the workforce further by recruiting hundreds of new technical employees. The announcement elicited much investor interest as it came ahead of the third-quarter earnings release, which is scheduled for October 21 before the opening bell. Interestingly, the latest estimates point to a 6% increase in net earnings to $2.41 per share, on revenues of $13.5 billion.

Infographic: Highlights of PayPal’s Q2 2022 earnings report

This week, American Express’ stock traded down 24% from the levels seen twelve months ago. It made strong gains during Monday’s regular session and traded slightly above $140 in the afternoon.