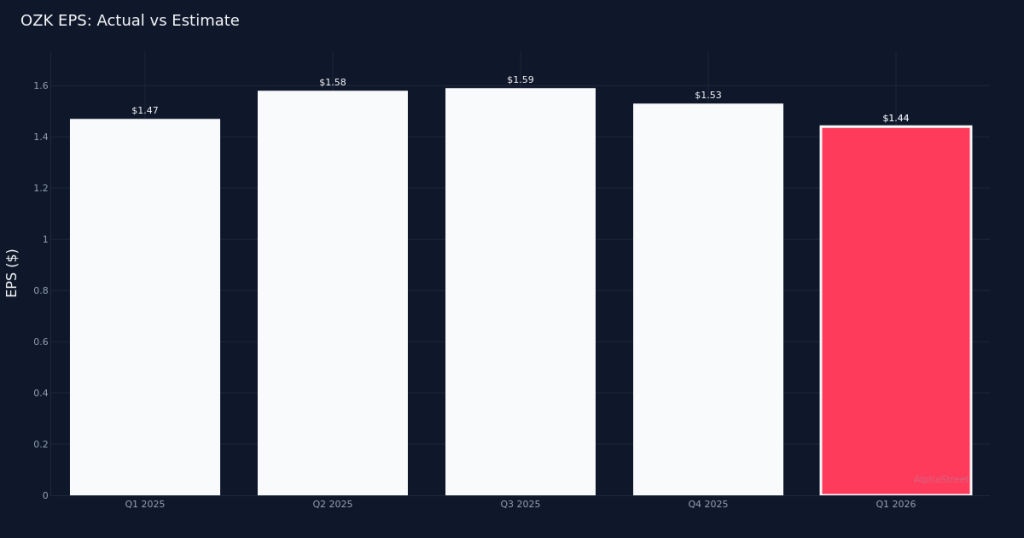

In-Line Quarter. Bank OZK (NASDAQ:OZK) delivered Q1 2026 diluted earnings of $1.44 per share, precisely matching Wall Street’s consensus estimate of $1.44, though results reflected a modest 2.0% year-over-year decline from the $1.47 per share earned in Q1 2025. The regional bank generated $159.3 million in net income for the quarter. The performance suggests the Little Rock-based lender continues navigating a challenging operating environment marked by interest rate pressures and evolving credit dynamics.

Muted Profit Growth. The year-over-year earnings compression, while relatively modest, signals headwinds that merit attention from institutional investors. With the bank meeting but not exceeding expectations, the results lack the positive surprise that typically drives multiple expansion in the regional banking space. The sequential earnings trajectory and underlying drivers of the profitability decline—whether net interest margin compression, elevated provisioning, or fee income weakness—will be critical factors for investors parsing the earnings quality. Without accompanying revenue or loan growth data, it’s difficult to assess whether operational momentum remains intact or if the bank faces more structural profitability challenges.

Branch Network Steady. Bank OZK maintained its physical footprint of 268 banking offices at quarter end, reflecting a stable distribution strategy in an era when many regional banks continue rationalizing branch networks. This suggests management remains committed to its community banking model and geographic markets, though investors will want to understand the productivity metrics and cost-to-income ratios associated with this retail presence. The branch count provides some context for the bank’s scale and market penetration across its operating territories.

Market Reaction Negative. Shares declined following the earnings release, indicating investors found little to celebrate in the in-line results. The negative price action despite meeting expectations suggests either disappointment with the year-over-year decline, concern about forward guidance or underlying trends, or broader sector weakness weighing on regional bank valuations. The stock’s post-earnings performance underscores that simply meeting the bar may be insufficient when earnings are moving backward on a year-over-year basis.

Analyst Sentiment Mixed. Wall Street’s view on Bank OZK remains balanced, with analyst consensus standing at 5 buy ratings and 6 hold ratings, with no sell recommendations. The tilt toward neutral reflects cautious optimism, suggesting the Street sees value but lacks conviction for aggressive accumulation at current levels. This split recommendation profile is typical for regional banks facing uncertain macro conditions but maintaining solid fundamentals.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.