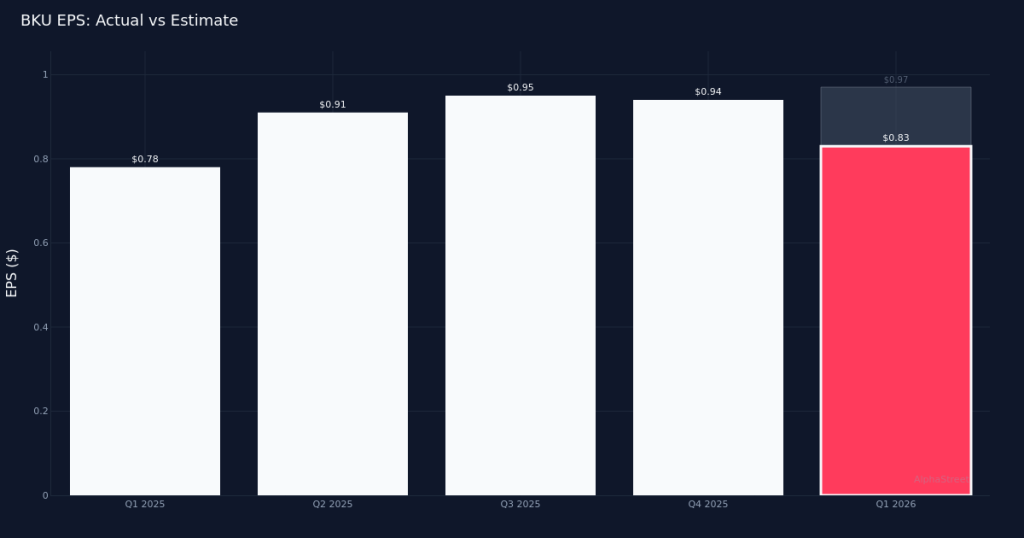

BKU|EPS $0.83 vs $0.97 est (-14.4%)|Net interest income $422.2M|Net Income $61.9M

BKU|EPS $0.83 vs $0.97 est (-14.4%)|Net interest income $422.2M|Net Income $61.9MEarnings Miss. BankUnited, Inc. (NYSE: BKU) reported Q1 2026 diluted earnings of $0.83 per share, falling short of the $0.97 consensus by 14.4%. The regional bank posted net income of $61.9M on net interest income of $422.2M for the quarter, as the company navigated a challenging operating environment. Shares declined 1.2% to $46.77 following the release, reflecting investor concern over the bottom-line shortfall despite year-over-year EPS growth.

Mixed Performance. While the earnings miss captured headlines, the underlying trends presented a more nuanced picture. EPS was up 6.4% from $0.78 in Q1 2025, demonstrating year-over-year profitability improvement. However, net interest income totaled $422.2M, down 4.9% from $443.7M in the prior-year quarter. This top-line contraction against expanding per-share earnings suggests the company may be managing costs aggressively to protect margins, though the magnitude of the consensus miss indicates those efforts weren’t sufficient to offset revenue headwinds or other operating pressures during the quarter.

Asset Quality Concerns. The company’s non-performing loan ratio stood at +0.8% for the quarter, a metric institutional investors will scrutinize closely given the current credit cycle. For a regional bank operating $35.4 billion in total assets at quarter-end, even a modest deterioration in loan quality can have material implications for provisioning requirements and future profitability. This asset quality indicator, combined with the earnings shortfall, raises questions about the health of BankUnited’s loan portfolio and whether management is adequately reserved for potential credit losses in the quarters ahead.

Analyst Positioning. Wall Street consensus currently stands at 6 buy, 6 hold, and 1 sell rating, reflecting a balanced but cautious view on the stock. This evenly split buy-hold distribution suggests the Street is taking a wait-and-see approach to BankUnited’s prospects, particularly as the company works through revenue challenges while maintaining earnings growth. The Q1 miss may prompt some analysts to reassess their models and price targets, especially if management’s commentary failed to provide a clear pathway to reaccelerating revenue growth or stabilizing asset quality metrics.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.