Credit card firm American Express Company (NYSE: AXP) bounced back quickly from the slowdown that followed the widespread travel ban more than two years ago. With the post-COVID reopening gathering steam across markets, the company’s volumes are once again where they were before the coronavirus outbreak.

Unlike most Wall Street stocks, AXP stayed unaffected by the recent market selloff to a great extent and its value is above the 52-week average now. In recent weeks, the stock traded mostly sideways, after paring its initial gains this year. The valuation is just right – not very high for the fast-growing company that has constantly enhanced shareholder returns through regular dividend hikes and share buybacks. It is a safe investment that has the potential to reward investors handsomely, especially those who hold the stock for a long time.

Resilience

If the New York-based company’s stable performance in the past is any indication, it has what it takes to effectively deal with the macroeconomic uncertainties and weak consumer sentiment. The Amex management is looking for a 15-17% growth in full-year revenues and expects to deliver earnings in the range of $11.00 per share to $11.40 per share. Naturally, there would be a corresponding momentum in the performance of the stock, which is expected to gain in double digits this year.

The stable recovery and volume growth can be attributed primarily to the increase in card fees and higher card spending, which rose to a record high in the most recent quarter. The positive data underscores that American Express, with its business model focused on travel and entertainment, serves cardholders who belong to the higher-income group and have better credit scores than the customers of its competitors.

From American Express’ Q4 2022 earnings call:

“We operate in the most attractive segments and geographies of the fast-growing payment space. As highlighted by our leadership positions with premium consumers, including millennials and Gen Zs, small and medium-sized businesses, as well as serving the largest corporations in the world. We bring to this space a number of advantages that are very difficult for our competitors to replicate. These include our brands, our unique membership model, our premium global customer base, and an integrated payments model.”

Q1 Estimates

Going by experts’ analysis, the company’s financial performance in the early months of fiscal 2023 was mixed. The earnings projection for the first quarter is $2.66 per share, which is down 3%. It is estimated that revenues grew about 20% to $14.03 billion in the March quarter, for which results will be published on April 20 before the opening bell.

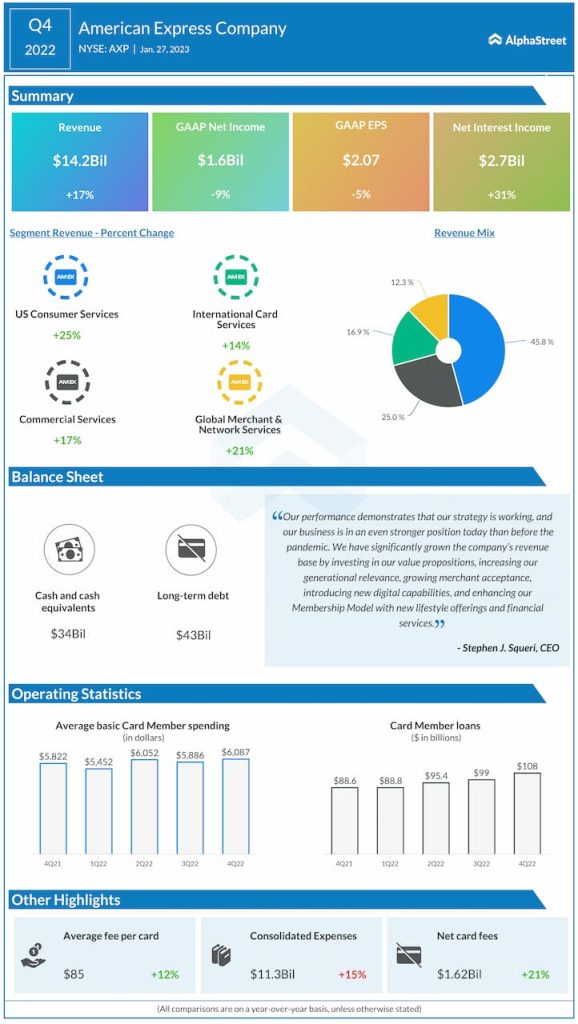

In the fourth quarter, net profit dropped 5% to $2.07 per share and missed expectations for the first time in more than six years. While the bottom line performance looks unimpressive on the face of it, the weakness is due to non-operational factors like variations in card provisions and costs related to Amex Venture’s losses.

Meanwhile, revenues grew by 17% to $14.2 billion. The highlight was double-digit revenue growth across all four business segments, reflecting the continued strong volume growth and reopening in key markets like China. The Amex leadership is optimistic about extending the uptrend into the current fiscal year.

After a strong start to Friday, shares of American Express ended the session slightly higher. It is up 10% since the beginning of the year.