Shares of Beyond Meat, Inc. (NASDAQ: BYND) were down over 2% on Friday. The stock has dropped 11% over the past three months. The company reported its third quarter 2024 earnings results earlier this week, delivering its first revenue growth in two years. It also narrowed its losses compared to the year-ago period. However, it lowered its guidance for the full year of 2024, which was a dampener. Here are a few points of note on its Q3 performance:

Revenue growth

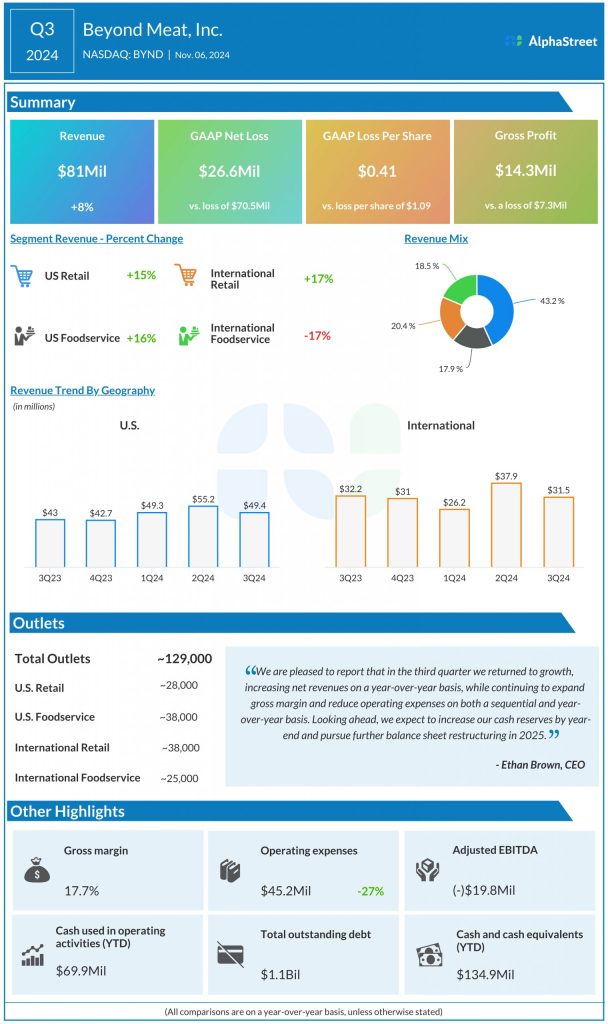

Beyond Meat’s net revenues increased 7.6% year-over-year to $81 million in Q3 2024, marking the first quarter of revenue growth since 2022. The rise in the top line was driven by a 15.8% increase in net revenue per pound, which in turn was fueled by price hikes on some products, lower trade discounts, and changes in product sales mix. These benefits were partly offset by a 7.1% drop in volume.

Narrower losses

The plant-based meat products maker reported a net loss of $26.6 million, or $0.41 per share, for the third quarter, which was narrower than the loss of $70.5 million, or $1.09 per share, reported in the year-ago period. The decrease in net loss was mainly driven by a reduction in loss from operations.

Loss from operations in Q3 narrowed to $30.9 million from $69.6 million last year, helped by higher gross profit and lower operating expenses. Although the reduction in losses is a positive, Beyond Meat is yet to achieve profitability and this remains a concern.

Margin improvement and cost reduction

Beyond Meat achieved a gross profit of $14.3 million in Q3 compared to a loss of $7.3 million in the year-ago quarter. Gross margin was 17.7% compared to a negative 9.6% last year. This improvement was driven by higher revenue per pound and lower cost of goods sold per pound.

Segment performance

BYND saw revenues increase in both its retail and foodservice channels in the US in Q3 2024. Revenues grew 14.6% YoY to $35 million in retail, driven mainly by a 22.6% increase in net revenue per pound, fueled by price increases and lower trade discounts. However, weak category demand and price elasticity led to a 6.6% drop in volume.

US foodservice revenues grew 15.5% to $14.5 million, driven by growth in volume and net revenue per pound. Volume growth was led by sales of chicken products to a US quick service restaurant customer that was absent in the prior-year period.

International retail revenues grew 17% to $16.6 million, helped by increases in net revenue per pound and volume. Volume growth was driven by distribution gains and higher demand in certain regions, while net revenue per pound benefited from lower trade discounts and changes in product sales mix.

Revenues in international foodservice fell 17.2% YoY to $15 million, mainly due to a 22.1% decrease in volume, partly offset by a 6.2% increase in net revenue per pound. The decrease in volume was mainly due to lower sales of burger and chicken products to a large QSR customer in Europe. Net revenue per pound was driven by lower trade discounts and price increases.

Guidance cut

Beyond Meat lowered its revenue guidance for the full year of 2024 and now expects net revenues to range between $320-330 million versus the previous range of $320-340 million. Gross margin is expected to be in the mid-teens range.