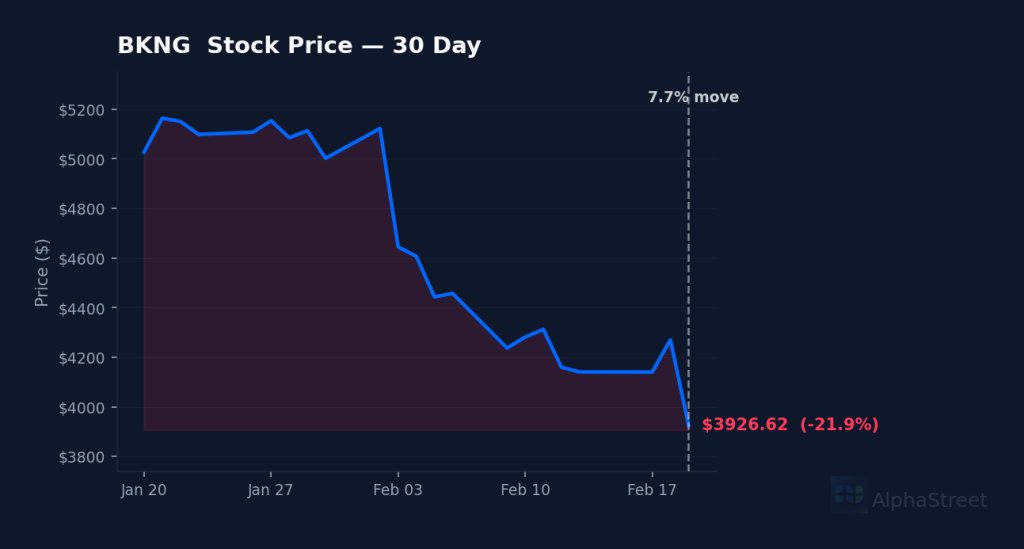

Earnings beat fails to impress investors. Booking Holdings shares plunged 7.65% to $3,925.75 after the online travel giant reported Q4 2025 EPS of $48.80, topping the $48.67 consensus by a slim 0.27%. The muted reaction followed yesterday’s after-hours earnings release—a stark contrast to the company’s recent track record of beating estimates by 3.7% to 41%.

The selloff accelerates existing weakness. BKNG has now fallen 25.8% from its late-January high of $5,248.61, trading well below both its 50-day average of $5,074 and 200-day average of $5,296. The stock collapsed through the psychologically critical $4,000 level in today’s session, hitting an intraday low of $3,890—a level not seen since mid-2024.

Volume tells a troubling story. Today’s 141,133 shares traded represents just 30% of the recent average daily volume, suggesting the decline came on relatively thin participation. More concerning: the stock has traded in elevated volume every day since February 3, when it first broke down below $5,000 on 634,000 shares—nearly 3x normal volume.

Valuation disconnect widens. At current prices, BKNG trades at 12.5x forward earnings versus a trailing P/E of 25.5x, implying the market expects 2026 EPS of $312.99. Yet analysts maintain a $6,040 price target—54% above current levels—and a consensus “buy” rating. The company’s 19.4% profit margin and 44.9% operating margin remain industry-leading, but revenue growth of 12.7% may be slowing from post-pandemic peaks.

Technical damage compounds fundamental doubts. The travel services sector faces mounting headwinds as consumer spending signals weaken across discretionary categories. BKNG’s inability to hold gains even after beating estimates suggests investors are pricing in deceleration ahead. The $3,890 low established today now becomes critical support—a break below could trigger stops toward the $3,600-3,700 zone.

This article was generated using AlphaStreet’s proprietary financial analysis technology and reviewed by our editorial team.