The education technology is one field that has grown rampantly in recent times, especially after the impact of the global pandemic. Newly emerging innovative technologies in educational institutes have led to an increase in the ed tech service providers. Let’s analyze what the future holds for ed tech firm Boxlight (NASDAQ: BOXL).

Overview

Boxlight sells interactive education products, including flat panels, projectors, whiteboards and peripherals to the education market. The Atlanta, Georgia-based firm also distributes science, technology, engineering and math (STEM) products, including a portable science lab. All these products are integrated into Boxlight’s classroom software suite that provides tools for learning, assessment and collaboration.

Boxlight generates revenue from the sale of its software and interactive displays to the K-12 US education market.

Financial performance

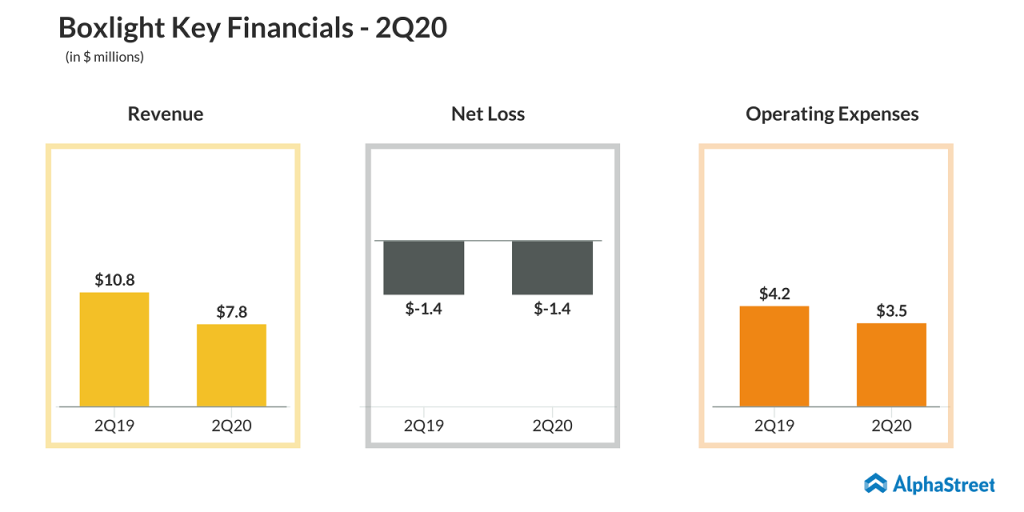

For the second quarter ended June 30, 2020, Boxlight’s loss remained flat at $1.4 million. Revenue declined by 28% to $7.8 million, hurt by the school closures as a result of the ongoing COVID-19 global pandemic.

For the year ending December 31, 2019, the loss widened to $9.4 million from $7.2 million in the prior year. Lower sales volume and an increase in costs in 2019 resulted in a higher loss. Revenue slipped 13% in 2019 to $33 million, hurt by a decrease in hardware sales.

Samsung partnership

Last week, Boxlight joined hands with Samsung Electronics America to bundle classroom displays, classroom software and professional development for the education market. With Samsung’s expansive resources, Boxlight expects sales to grow in the future quarters.

During the Q2 earnings call, CEO Michael Pope said,

“We’re hesitant to put numbers behind it, but you could imagine, if we’re successful with Samsung in education, the amount of business we could generate would be substantially more than even where we are today.”

Outlook

There is a risk related to the modification of the traditional classroom setting that may result in reduced demand for Boxlight’s classroom solutions, including reduced demand for the company’s interactive displays due to extended or indefinite distance and digital learning.

With the way of teaching methods getting transformed of late, technology is helping for that transformation, especially during this pandemic-affected period. Ed tech demand has been growing dramatically. Boxlight stated that there was a growth in Q2 and the company expects substantial demand growth in Q3 and beyond.

Also read: Boxlight (BOXL) Q2 2020 Earnings Call Transcript

In Q2, interactive panels for education dropped by about 20% in the US. Globally, excluding China, they dropped about 20%. Boxlight expects this to narrow down in Q3. In Q4 and beyond, Boxlight expects the demand to pick up, and looks for growth in interactive flat panel demand for next year and the following years.

For this year, Boxlight expects double-digit growth in software and services divisions. The company also expects good growth internationally.

Summary

COVID-19 has reduced demand and spending across all the businesses. The education technology sector is also not immune to that and it will adversely impact the operations, financial performance of the company as well as on the operations and financial performance of many of its customers and suppliers in the education technology sector.

With most of the educational institutions shifting toward online platforms, Boxlight is expected to face the headwinds created by the pandemic until the world returns to normalcy. Until then BOXL stock will be a darling for traders. Those who consider BOXL for long-term, can wait for the dust to settle down and then make a decision.

____

Disclaimer: The views and opinions presented here are of the author alone and does not represent the views of AlphaStreet