The financial technology provider increased its adjusted earnings outlook for fiscal 2026 as recurring revenue grew 9% in the second quarter. Strong organic expansion and digital asset gains offset a decline in event-driven activity and margin pressure from rising distribution costs.

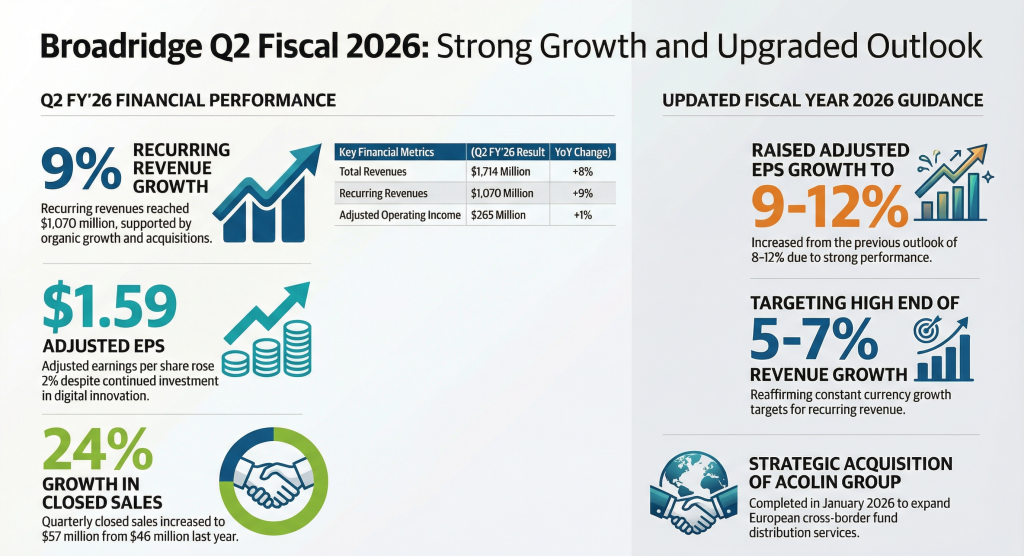

Broadridge Financial Solutions, Inc. (NYSE: BR) reported a 9% increase in recurring revenue for the second quarter of fiscal year 2026, leading the company to raise its full-year adjusted earnings guidance. Total revenues reached $1.714 billion for the period ended December 31, 2025, while GAAP net earnings were significantly bolstered by non-operating gains related to digital asset holdings.

Digital Assets Lift Reported Profits

The company reported diluted earnings per share of $2.42, a 102% increase over the prior year period. This surge was primarily driven by a $137 million unrealized gain on digital assets and a $53 million realized gain related to the contribution of Canton Coins to the Canton Digital Asset Treasury 4. On an adjusted basis, which excludes these valuation changes and other non-recurring items, earnings per share rose 2% to $1.59.

Revenue Expansion Offset by Margin Decline

Total revenues rose 8% to $1.71 billion compared to $1.59 billion in the prior year quarter. Recurring revenues, a key metric for the firm, reached $1.07 billion, supported by 7% organic growth and contributions from acquisitions 3, 5. Event-driven revenues fell 27% to $91 million, a decline attributed to lower mutual fund proxy activity 8. Distribution revenues increased 14% to $553 million, influenced by higher communication volumes and a $32 million impact from postage rate increases.

Operating income decreased 2% to $206 million, with GAAP margins contracting to 12.0% from 13.3% 3, 8. The Investor Communication Solutions (ICS) segment saw pre-tax margins fall to 11.1% from 15.1% due to lower event-driven revenue and an 12% rise in operating expenses 9, 10. Conversely, the Global Technology and Operations (GTO) segment reported a pre-tax margin increase to 16.1% from 11.3%.

Higher Earnings Forecast and Expansion Plans

Management raised its fiscal year 2026 guidance for adjusted earnings per share growth to a range of 9% to 12%, up from the previous 8% to 12%. The company reaffirmed its outlook for recurring revenue growth at the higher end of the 5% to 7% range on a constant currency basis and maintained its closed sales target of $290 million to $330 million.

The stated operational strategy focuses on the digitization of investing, modernization of wealth management, and innovation in trading platforms. Capital allocation remains directed toward initiatives in tokenization and digital communications, as well as strategic M&A, exemplified by the $70 million acquisition of Acolin Group in January 2026 to expand European fund distribution services.

Sector and Macro Trends

Broadridge’s performance occurred against a backdrop of increased investor participation, with equity revenue positions growing 11% and mutual fund/ETF positions rising 15%. However, macroeconomic factors such as postage rate hikes and higher float income negatively impacted adjusted operating margins by 40 basis points during the quarter. The company’s results also reflect a growing institutional integration of digital assets, as evidenced by its substantial gains from the Canton Digital Asset Treasury.

Investment Thesis

Bull Case

- Strong Organic Growth: The company achieved 7% organic recurring revenue growth and a 24% increase in quarterly closed sales, indicating healthy demand for core services.

- Position Growth: Double-digit increases in equity and ETF positions suggest a robust environment for the company’s investor communication business.

- Strategic Expansion: The acquisition of Acolin and the growth of digital asset revenues point toward successful diversification into new geographic markets and technologies.

Bear Case

- Margin Compression: Operating margins are facing pressure from higher technology costs, volume-related expenses, and a 14% increase in distribution costs.

- Volatility in Event-Driven Revenue: A 27% drop in event-driven revenue highlights the unpredictable nature of this segment, which can significantly weigh on overall ICS profitability.