Conagra Brands, Inc. (NYSE: CAG) has reported mixed results for the final three months of fiscal 2024 and issued weak guidance for 2025, sending the stock lower on Thursday morning. Fourth-quarter earnings came in above analysts’ estimates but revenues missed, with both numbers declining from the year-ago quarter.

Post-earnings, the stock traded down 3.5%, reversing the upturn seen ahead of the announcement. The management’s cautious guidance added to investors’ concerns. CAG has frequently underperformed the market recently, losing 15% over the past year while the S&P 500 gained 27%. Shareholders do not have much to cheer about the stock right now, but Conagra is unlikely to disappoint long-term investors.

What’s in Cards

It is worth noting that the company has remained resilient to recent economic uncertainties to a large extent, in a testament to its solid fundamentals. The diversified product portfolio and stable margin performance, aided by higher average price per unit, should help Conagra shrug off the present weakness and return to the high-growth path. According to the company’s leadership, recent investments — focused on enhancing the brands — have started yielding results, such as volume growth in areas like Domestic Retail, Frozen, and Snacks.

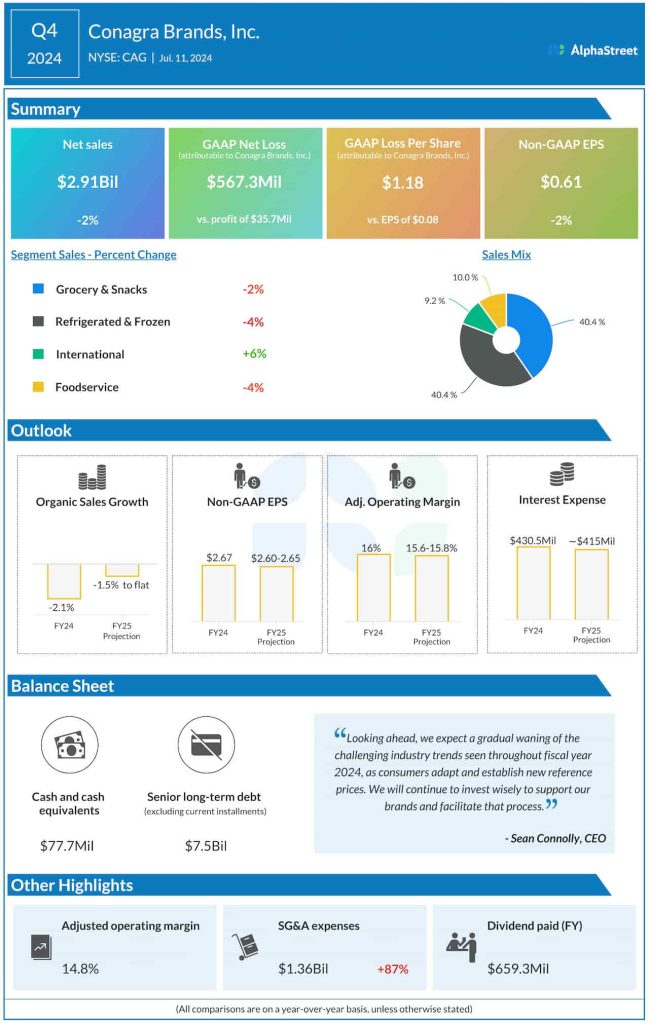

Net sales decreased 2% year-over-year to $2.91 billion in the fourth quarter, mainly due to muted performance by the Grocery and Frozen segments. That was partially offset by a 6% increase in international sales. Organic net sales were down 2.4%. Consequently, earnings, adjusted for special items, decreased to $0.61 per share in Q4 from $0.62 per share in the corresponding quarter a year earlier. The bottom line came in above the market projection, a trend seen every quarter in the past two years.

Weak Results

On an unadjusted basis, the bottom line was negatively impacted by certain non-cash goodwill and brand impairment charges. Including those items, the company reported a net loss of $567.3 million or $1.18 per share for the quarter, vs. net income of $37.5 million or $0.08 per share in the prior-year period. In the whole of fiscal 2024, total free cash flow more than doubled to $1.6 billion.

Anticipating the weakness to extend into the next fiscal year, the management expects organic sales to be flat to down 1.5% in FY25. The estimated full-year adjusted EPS is $2.60-$2.65 per share, the mid-point of which is below the prior-year number. The top-line guidance is lower than analysts’ consensus estimates. Adjusted operating margin is forecast to be between 15.6% and 15.8%.

“In terms of how we expect the year to progress, we expect Q1 to deliver the lowest volume, top line, and adjusted gross margin of any quarter. While we still receive the benefit from pricing put in place in fiscal 24, Q1 will be impacted by continued brand-building investments and wrapping on our highest top-line quarter in the prior year. We are planning for sequential volume improvement each quarter after Q1 to achieve our full-year sales guidance,” said David Marberger, chief financial officer of Conagra Brands.

On Thursday, Conagra’s stock traded at a four-month low, after going through a series of ups and downs since the beginning of the year. It has lost about 13% in the past twelve months.