Shares of Campbell Soup Company (NYSE: CPB) stayed red on Monday. The stock has dropped over 8% in the past one month. The food company delivered sales and earnings growth for the third quarter of 2024. Its top line received a boost from the Sovos Brands acquisition in Q3 and further top and bottom line benefits are anticipated going forward.

Sales and earnings growth

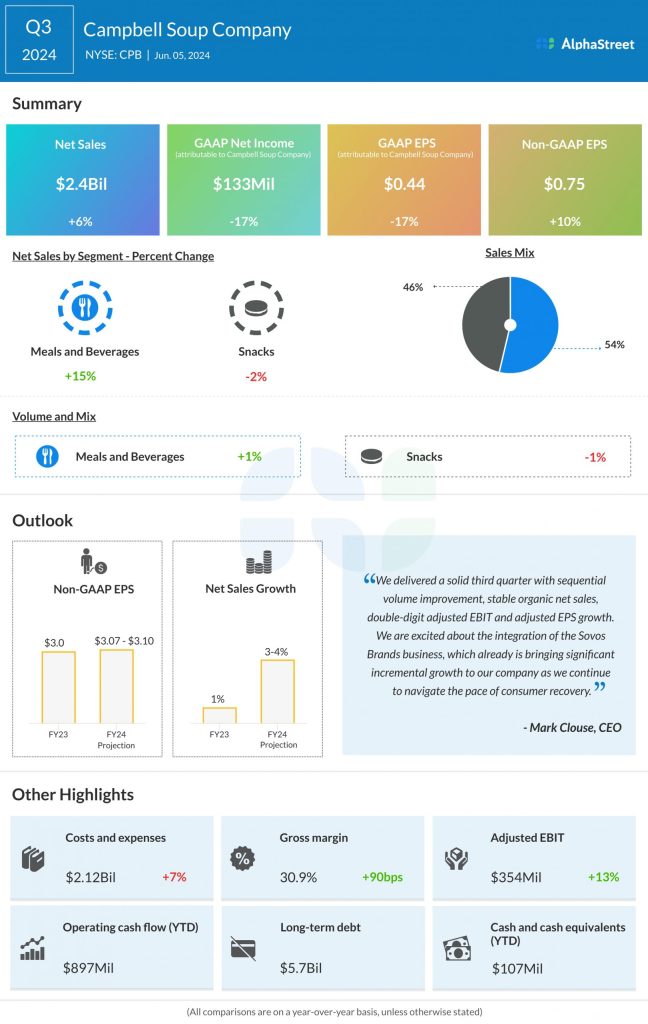

Campbell’s net sales increased 6% year-over-year to $2.4 billion in Q3 2024, driven by contributions from the Sovos Brands acquisition. Organic sales remained flat versus the year-ago period. The company saw volumes improve sequentially in Q3 and expects this trend to continue into Q4. Adjusted EPS increased 10% to $0.75, helped by higher adjusted EBIT.

Strength in Meals & Beverages

In Q3, net sales in Campbell’s Meals & Beverages segment increased 15% YoY to $1.3 billion, boosted by the Sovos Brands acquisition. Organic sales remained flat as gains in foodservice were offset by declines in US retail products.

As mentioned on the quarterly call, US soup sales saw a growth of 2% in the quarter, as strength in broth partly offset weakness in ready-to-serve and condensed soups. Customers looking to prepare stretchable meals helped drive demand within the soup category. Despite pressures in the ready-to-serve category, the addition of Rao’s ready-to-serve soup business yielded gains during the quarter.

Strength in Prego pasta sauces and the addition of Rao’s Italian sauce is driving momentum in Campbell’s sauce business. The company’s frozen meal business benefited from gains in its frozen pizza portfolio.

Snacks resilience

Sales in the Snacks segment fell 2% year-over-year to $1.1 billion in the third quarter. Organic sales dipped 1% due to declines in third-party partner brands, contract manufacturing, frozen products and fresh bakery. These declines were partly offset by a 2% growth in power brands, driven by gains in cookies, crackers, and salty snacks.

On its call, Campbell attributed the slowdown in snacking to economic pressures that have been taking a toll on low and middle income consumers. Despite the near-term pressures, the company remains confident in the resilience of this business as it has seen very little price elasticity and its slowdown has been modest compared to other edible categories.

In addition, the upcoming summer holiday period is expected to drive meaningful demand for snacks and Campbell is already seeing a pickup in this segment. The company expects to see a recovery in Snacks over the next couple of quarters and significant growth over the long term.

Outlook

Campbell updated its full year 2024 guidance to reflect the impact of the Sovos acquisition. Net sales are expected to grow 3-4% in FY2024. Organic sales growth is tracking to the midpoint of the updated range of approx. flat to down 1%. Adjusted EPS is expected to grow 2-3% to $3.07-3.10.

The company expects organic sales growth in the fourth quarter of 2024 to moderately increase sequentially from the third quarter. Adjusted EPS is expected to increase double digits in Q4, driven by higher adjusted EBIT.