Shares of Campbell Soup Company (NYSE: CPB) gained over 7% on Wednesday, following the announcement of the company’s first quarter 2024 earnings results. The stock has dropped 23% year-to-date. The company also reaffirmed its guidance for the full year of 2024. Here are the main takeaways from the report:

Profits beat, sales in-line

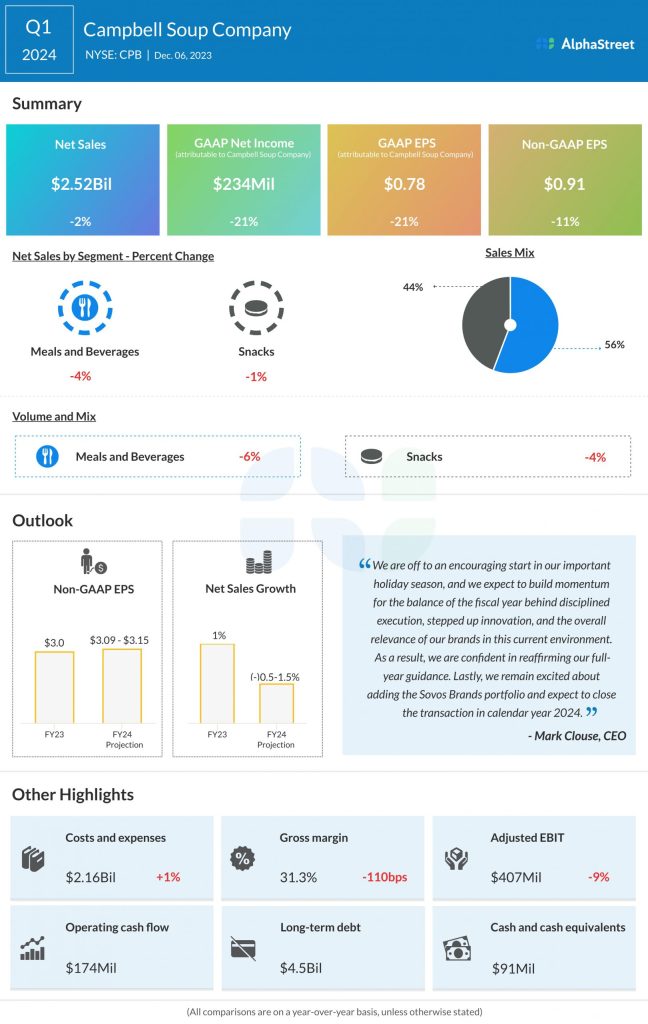

Campbell Soup’s net sales for Q1 2024 decreased 2% year-over-year to $2.52 billion but were in line with estimates. Organic sales were down 1%. GAAP EPS fell 21% YoY to $0.78. Adjusted EPS of $0.91 dropped 11% versus last year but managed to surpass projections.

Segment performance

In Q1, net sales in the Meals & Beverages segment decreased 4% on a reported basis and 3% on an organic basis, due to declines in US retail products, mainly soup and beverages. This was partly offset by an increase in foodservice. Weakness in the condensed and ready-to-serve categories, partly offset by growth in broth, led to a 5% drop in sales for US soup. Volume/mix within the segment declined 6%, partly offset by net price realization of 2%.

In the Snacks segment, net sales decreased 1%. Excluding impacts from the Emerald nuts business divestiture, organic sales grew 1%. This growth was driven by a 5% increase in sales of its 8 power brands. The segment benefited from gains in cookies and crackers, particularly Lance sandwich crackers and Goldfish crackers. Net price realization of 5% was partly offset by volume/mix declines of 4%.

Outlook

Campbell reaffirmed its guidance for the full year of 2024. Net sales growth is expected to range between down 0.5% to up 1.5% YoY. Organic sales are expected to grow 0-2%. The top line guidance reflects volume declines in 1H24 with sequential improvement anticipated to result in positive volume trends in the latter half of the year. Net sales growth for the year is also expected to reflect lower contribution from pricing.

The company expects a modest progress in earnings and margin in FY2024, weighted to the second half, reflecting a moderation in inflation and productivity improvements. Adjusted EPS is expected to range between $3.09-3.15, representing a growth of 3-5% from the previous year.