Campbell Soup Company (NYSE: CPB) ended fiscal 2023 on a mixed note, reporting an increase in sales and lower adjusted profit for the final three months of the year. The management has exuded confidence that lower costs and strong demand for the company’s snacks would drive earnings growth going forward, offsetting the inflation-induced cutback on consumer spending.

The post-earnings performance of CPB has not been encouraging, as the stock continued the recent downtrend after the announcement. The market will be keeping track of the company’s future financial performance, even as the management predicts an improvement in volumes and margin growth, aided by its cost-reduction measures.

On Track

Going forward, continued improvement in the Snacks division and business expansion should enable the company to meet its growth targets. In the near term, the Meals & Beverages business is seen gaining momentum, while the overall performance is expected to gather stream by the latter half of fiscal 2024. Also, the planned acquisition of Sovos Brands will help strengthen and diversify the business, thereby catalyzing revenue growth.

The demand for soup, Campbell’s core product, is often influenced by the seasonal nature of consumption – sales were down in the summer and are expected to pick up in the fall and winter. The company has been constantly innovating and expanding capacity to meet the growing demand, while also enhancing its capabilities in supply chain and marketing.

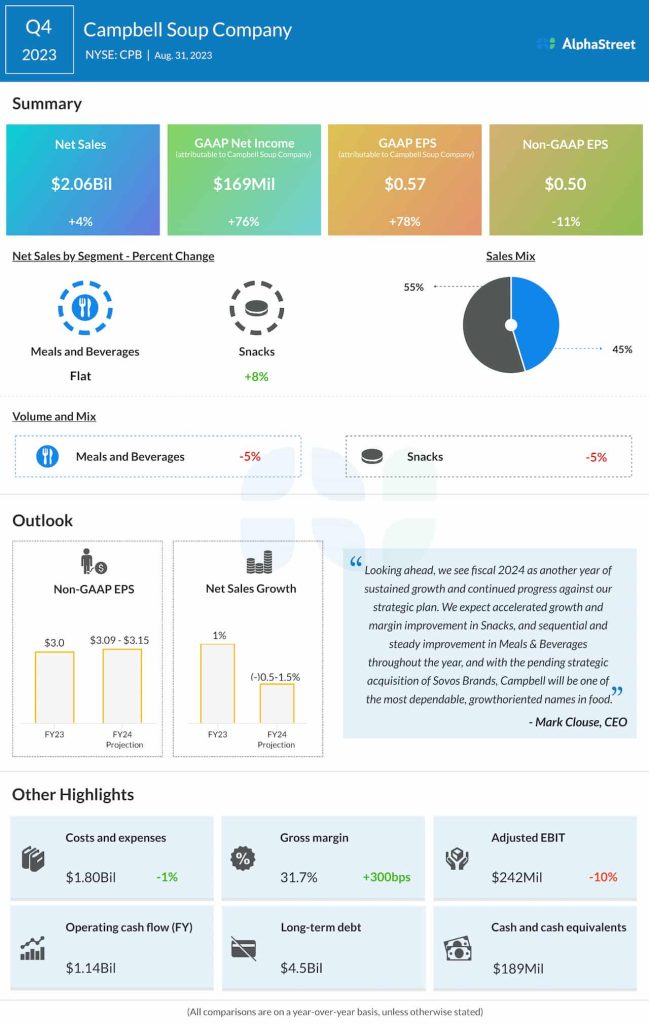

Outlook

The Campbell leadership expects fiscal 2024 earnings, adjusted for one-off items, to be in the range of $3.09 per share to $3.15 per share, which represents an increase from the FY 2023 profit of $3.00 per share. The guidance is above Wall Street’s projection. Full-year sales are expected to increase, but modestly because consumers tend to go for cheaper alternatives due to financial uncertainties.

Campbell’s CEO Mark Clouse said at the earnings call, “I’m excited and very optimistic as we enter the new year with proven strategies and strong fundamentals and advantaged strong supply chain and arguably one of the most focused portfolio stories in the industry. Within snacks, we continue to expect accelerated growth and to build on the margin trajectory from this year. And in meals and beverages, we expect to continue to strengthen the business with sequential and steady improvement throughout the year.”

Q4 Outcome

In the July quarter, net sales increased 4% annually to $2.1 billion. Organic net sales were up 5%. On a reported basis, fourth-quarter net income was $169 million or $0.57 per share, compared to $96 million or $0.32 per share in the corresponding period of 2022. Excluding special items, net income decreased 11% year-over-year to $0.50 per share. There was a modest decrease in operating expenses, reflecting the management’s cost-cutting efforts, while the gross margin rose an impressive 300 basis points.

Campbell’s stock traded slightly lower on Friday afternoon, after falling 26% in the past eight months. It experienced weakness after the earnings release and underperformed the market.