Shares of Campbell Soup Co. (NYSE: CPB) have dropped 5% since the start of the year and 7% over the past one month. The stock stayed in red territory on Thursday after falling over a lacklustre third quarter 2021 earnings report and a bleak outlook provided by the company a day ago. The downside is, the challenges faced by the company during its just-ended quarter are likely to continue over the coming months.

Revenue decline

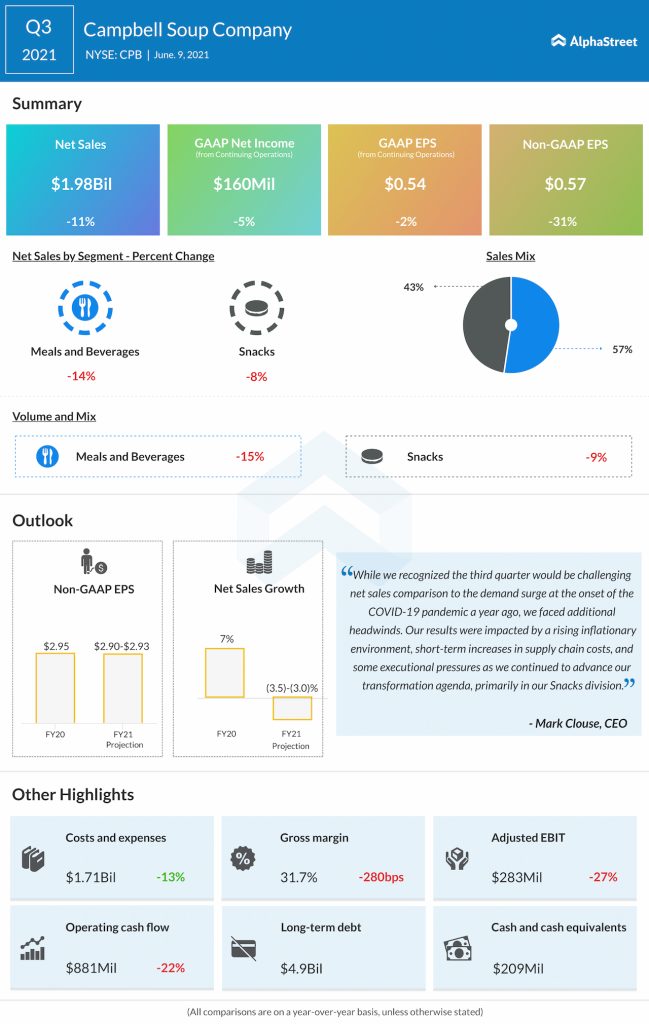

Campbell’s net sales fell 11% year-over-year in Q3 to $1.98 billion, falling short of market estimates. Organic sales dropped 12% compared to a 17% growth in the same period a year ago when the company saw demand spike due to pantry-loading as a result of the COVID-19 pandemic.

Campbell saw sales drop across both its segments during the quarter as it lapped strong demand and consumption during the year-ago period amid the pandemic. Meals & Beverages sales dropped 14% while Snacks sales declined 8% year-over-year.

Although the company saw some momentum for its retail products and a recovery in its foodservice business, it was not enough to offset the sales decline. Looking ahead, as the restrictions ease, it is likely that people will begin to dine outside more and this could lead to a dip in at-home meal preparation.

The pandemic-related lap is expected to continue for the rest of the year leading to a decline in organic sales for the fourth quarter of 2021. Campbell also expects its reported sales for the full year of 2021 to decrease 3-3.5% and organic sales to drop 1.2% to 0.7%.

Gross margins

Campbell’s margins during the third quarter were pressured by high costs, supply chain disruptions and changes to its Snacks unit. Gross margins fell to 31.7% from 34.5% in the year-ago quarter. The decline was larger than what the market had expected.

Margins were impacted by higher costs brought on by bad weather in Texas, which impacted the supply chain and temporarily closed down a facility, as well as lower fixed cost leverage, labor challenges and changes within the Snacks division.

Most of the pressure on margins were caused by transitional costs as the company works its way out of the pandemic situation and even though the impact of these costs are expected to moderate going into Q4, they will still weigh on margins in the near-term.

The negative impact on gross margins led to a decrease in adjusted EPS which amounted to $0.57, missing market expectations.

Inflation

Campbell stated that its results were hurt by a rising inflationary environment as well as short-term increases in supply chain costs. Cost inflation was around 4% on a rate basis in Q3, which was higher than expected and mainly driven by freight rates. The company expects inflation to remain high in the fourth quarter as pricing actions take hold at the start of FY2022.

Click here to read the full transcript of Campbell Soup Q3 2021 earnings conference call