Shares of The Campbell’s Company (NASDAQ: CPB) stayed green on Monday after the company reported its third quarter 2025 earnings results. The top and bottom line numbers beat expectations. The soup giant benefited from a rise in at-home cooking but was pressured by choosy snacking trends. The company reaffirmed its outlook for the full year, but it anticipates earnings to come at the low end of the guidance range due to the slow recovery in its snacks business.

Better-than-expected results

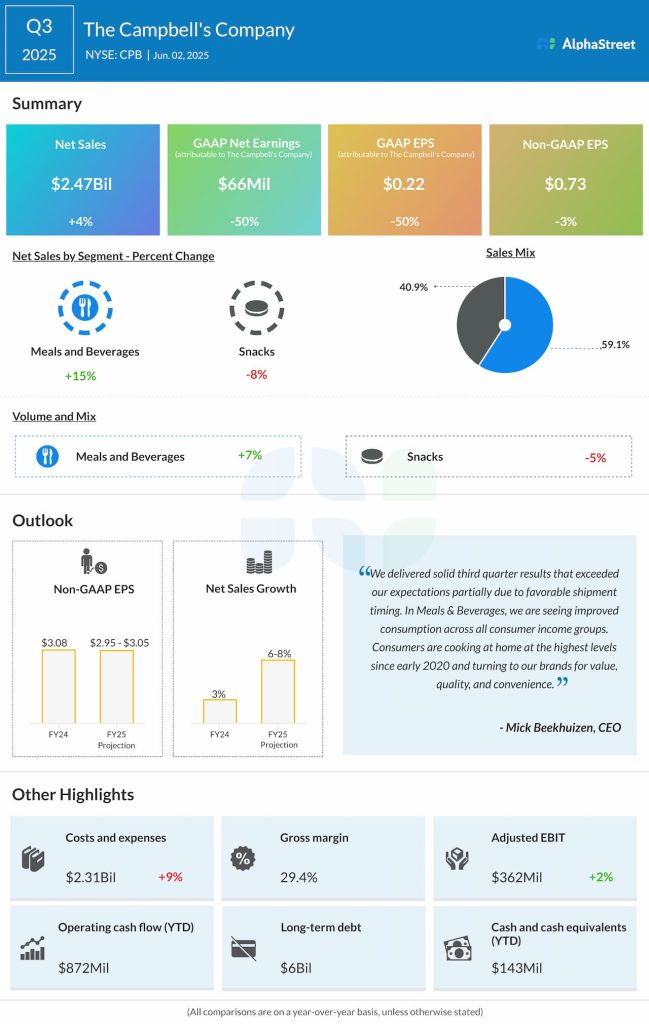

In the third quarter of 2025, Campbell’s net sales increased 4% year-over-year to $2.47 billion, beating estimates of $2.43 billion. Organic sales grew 1%, led by volume growth. The top line benefited from strength in the Meals & Beverages division and the Sovos Brands acquisition. Adjusted earnings per share dropped 3% YoY to $0.73 but surpassed projections of $0.66.

Meals vs. Snacks

In the third quarter, Campbell’s business delivered a mixed performance, with strong growth in its Meals & Beverages segment offsetting softness in the Snacks business. This performance was driven mainly by shifts in consumer behavior.

Against a dynamic macroeconomic backdrop, consumers are cooking more meals at home and choosing products that allow them to stretch their food budgets. They are also increasingly conscious about their discretionary snack purchases and prefer to spend on healthier options while making those purchases. These trends were a tailwind for the Meals & Beverages division and a headwind for the Snacks division.

In Q3, sales in the Meals & Beverages segment grew 15% YoY to $1.46 billion. Organic sales rose 6%. The soup portfolio performed well in the quarter with growth in the wet soup, condensed cooking soup, and broth categories. Brands such as Swanson, Chunky, Pacific and Rao’s delivered gains during the quarter.

The Snacks segment saw sales decline 8% YoY to $1 billion, due to continued category softness and heavy competition. Organic sales were down 5%. The company faced headwinds in discretionary categories like crackers and chips. CPB is focusing on product innovation and managing its assortment as it tries to regain momentum in this segment.

Outlook

Campbell’s expects net sales to grow 6-8% YoY in fiscal year 2025. Organic sales are expected to be down 2% to flat versus the prior year. Adjusted EPS is expected to be $2.95-3.05, representing a decline of 4% to 1% from the previous year. The company now expects adjusted EPS to be at the low end of the guidance range due to the slower-than-expected recovery in the Snacks business.