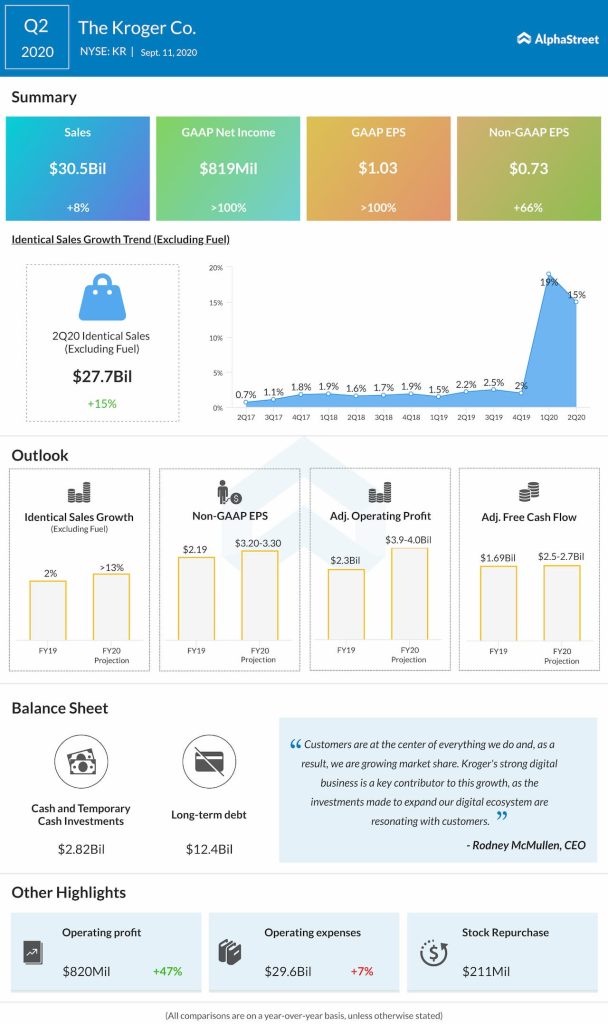

It is estimated that customers who adopted e-commerce during the pandemic are unlikely to go back to their old shopping habits and those who already shop online are increasing their orders. While benefiting from the new trend, retailers like Kroger Co. (NYSE: KR) are also cashing in on customers’ newfound affinity for private labels.

For the Ohio-based supermarket chain, one of the key growth drivers has been the high demand for its own brands like Simple Truth, and the trend has come in handy during the pandemic days. Kroger’s recent sales performance shows it is benefiting from the unique product mix.

Investing in KR

The impressive earnings performance in recent quarters is yet to fully reflect on the performance of the stock, which on Monday traded slightly above $32. Analysts’ consensus estimate on the stock is hold and the average target price points to a 10% growth in the 12-month period. Though the stock is affordable, it makes sense to wait until next month’s earnings release before buying or selling.

From Kroger’s Q2 2020 earnings conference call:

“Our data insights show customers are rediscovering their passion for cooking at home and have an aspiration to eat more healthy foods as a result of COVID. When we talk to our customers they tell us they plan to continue to prepare and eat more meals at home. As children return to school many families are telling us they plan to make breakfast in the morning and prepare lunch for their children to take school.”

Online Shift

The company’s main priority in its response to the pandemic was to ramp up the digital platform and the initiative continues to bear fruit. It needs to be noted that it had a seamless digital ecosystem even before the pandemic, which helped in offering a superior customer experience by combining the e-commerce site and the network of pickup and delivery locations.

At the same time, margins have benefited from the management’s cost-saving efforts that gathered pace after an initial delay. The positive momentum is expected to continue for the rest of the year and beyond. With food products representing a sizable share of its sales, the company also expects to leverage the shift from food consumed away from home to food consumed at home during the crisis days.

Headwinds

Meanwhile, the pressure on the fuel business could remain a concern as far as profit is concerned, mainly due to the COVID-driven disruption. Also, the bottom line could be impacted by higher pension and healthcare costs.

“Kroger’s financial model has proven to be resilient throughout the economic cycle. We continue to generate strong free cash flow and maintain strong liquidity. We are committed to investing in the business to drive profitable growth, maintaining our investment-grade debt rating, and returning excess free cash to investors via share repurchases and the growing dividend over time,” said Kroger’s CFO Gary Millerchip during his post-earnings interaction with analysts a few months ago.

Bullish Outlook

When the company reports its third-quarter financial results on December 4, analysts will be looking for a 38% growth in earnings to $0.65 per share on revenues of about $30 billion, which represents a 10% year-over-year increase.

Read management/analysts’ comments on Kroger’s Q2 earnings

After dipping to a five-month low in early November, Kroger’s stock has bounced back and recouped the loss since then. The stock has gained 21% since last year and 6% in the past six months.