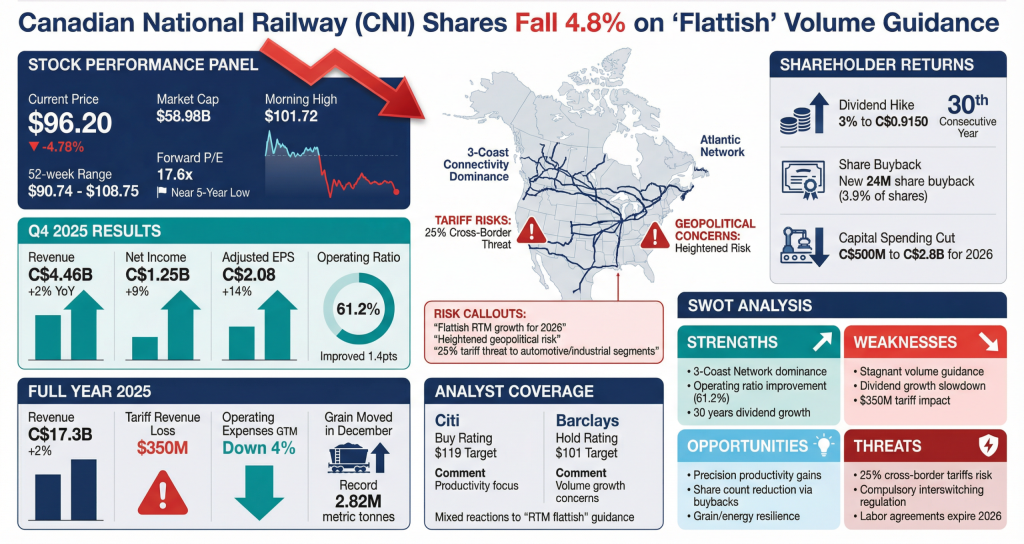

Canadian National Railway Company (CNI): SWOT Analysis

Strengths

- 3-Coast Network: Unique transcontinental reach remains a dominant competitive advantage in North America.

- Profitability Record: Delivered a 1.4-point improvement in operating ratio (61.2%) during a volatile quarter.

- Shareholder Loyalty: 30 years of dividend growth and a new 24M share repurchase mandate.

Weaknesses

- Stagnant Volume Guidance: “Flattish” RTM projections for 2026 suggest a lack of organic catalysts.

- Dividend Growth Slowdown: The 3% increase is a deceleration from previous years.

- Tariff Vulnerability: Already sustained a $350M revenue hit in 2025 due to trade friction.

Opportunities

- Precision Productivity: Continued reduction in cost per GTM provides margin protection in a low-growth era.

- Share Count Reduction: The new buyback program could provide a significant floor for EPS.

- Grain/Energy Resilience: Record grain movement capacity offers a hedge against weakness in consumer goods.

Threats

- 25% Cross-Border Tariffs: Potential new duties could cripple automotive and manufacturing carload volumes.

- Compulsory Interswitching: Potential Canadian regulatory changes could increase competition and pressure pricing.

- Labor Expiration: Collective agreements for conductors and engineers expire at the end of 2026, posing strike risks.