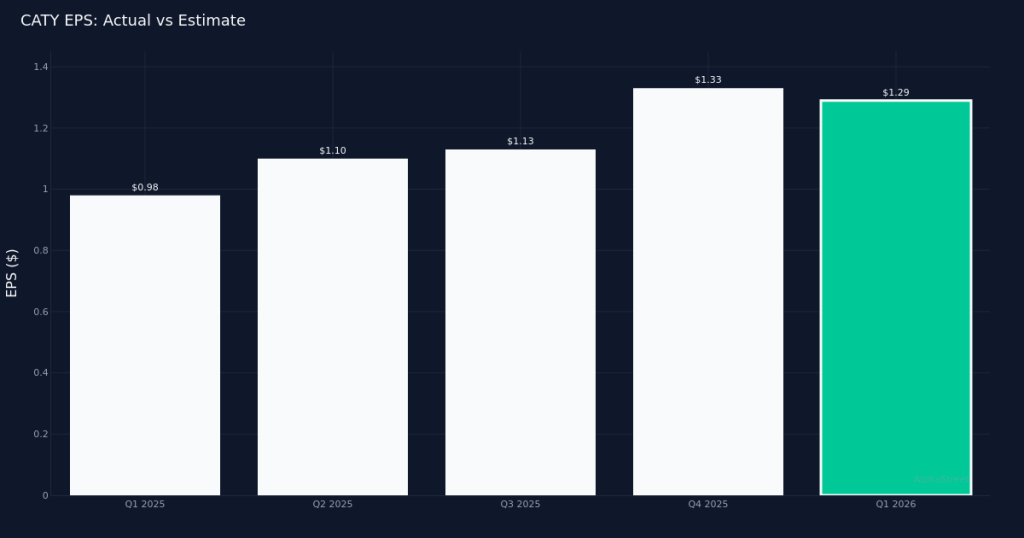

Earnings Beat. Cathay General Bancorp (CATY) posted Q1 2026 diluted EPS of $1.29, topping Wall Street’s $1.24 estimate by 4.0%. The company earned $86.9M in net income, reflecting strong operational execution in a challenging regional banking environment. Year-over-year, EPS moved up 31.6% from the $0.98 posted in Q1 2025, demonstrating meaningful momentum in profitability despite headwinds facing the broader banking sector.

Management Commentary. Leadership struck a confident tone on the quarter’s performance. “We delivered solid financial performance in the first quarter, reporting net income of $86.9 million and diluted earnings per share of $1.29,” management noted in prepared remarks. The company’s focus on its core banking strategy appears intact, with emphasis on disciplined loan growth and relationship-based lending driving results.

Loan Portfolio Expansion. The bank’s lending operation showed steady expansion, with management highlighting that “period-end loans of $20.2 billion grew 0.2% linked quarter, reflecting our focus on relationship lending.” The company operated 20,170,000,000 total loans, excluding loans held for sale at quarter end. This measured growth approach suggests disciplined underwriting standards rather than aggressive volume chasing, a positive signal for asset quality in an uncertain credit environment.

Net Interest Income. Net interest income before provision for credit losses was $194 for the quarter, representing a key revenue driver for the regional bank. This metric remains critical for assessing the bank’s core profitability and ability to generate income from its lending and investment activities amid fluctuating interest rate conditions.

Muted Stock Reaction. Shares traded largely unchanged following the report, suggesting the earnings beat was largely anticipated by the market or overshadowed by broader sector concerns. The modest stock movement despite a 4.0% EPS beat indicates investors may be taking a wait-and-see approach on the bank’s ability to sustain momentum, particularly as the regional banking sector faces continued scrutiny around deposit costs and credit quality.

Analyst Sentiment. Wall Street consensus stands at 0 buy, 5 hold, 2 sell, reflecting a cautious stance on the regional bank. The absence of any buy ratings despite the solid earnings performance and 31.6% year-over-year EPS growth suggests analysts remain concerned about the sustainability of net interest margin expansion or potential headwinds from the competitive deposit environment.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.