Shares of Chewy, Inc. (NYSE: CHWY) gained over 1% on Monday. The stock has dropped 10% in the past three months. The pet products seller delivered solid results for the third quarter of 2025 and expects to see continued growth for the remainder of the year. Here’s a look at a couple of factors that work in its favor:

Steady revenue growth

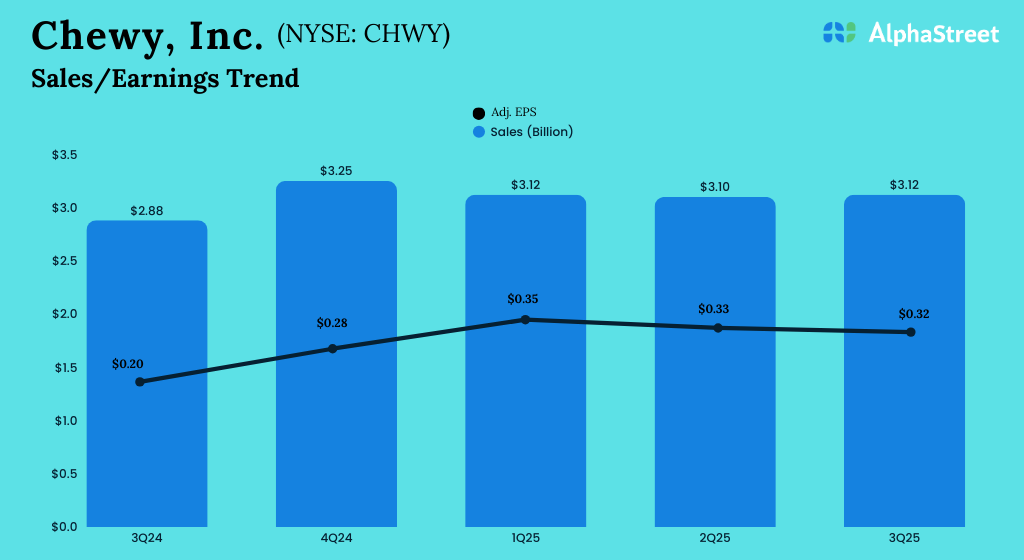

Chewy has delivered steady sales growth through this fiscal year. In Q3, net sales increased 8.3% year-over-year to $3.12 billion. Autoship customer sales increased 13.6% to $2.61 billion and accounted for nearly 84% of net sales in the quarter.

As mentioned on its earnings call, revenues generated from the Autoship subscription program are largely predictable, and this allows Chewy to cut its costs and grow margin in a way that gives it a competitive edge. Active customers grew nearly 5% YoY to 21.1 million while net sales per active customer was also up around 5% to $595.

Chewy forecasts net sales for the fourth quarter of 2025 to grow approx. 7-8% YoY to $3.24-3.26 billion. For fiscal year 2025, the company narrowed its sales outlook to $12.58-12.60 billion, representing a YoY growth of 8%, excluding the impact of the 53rd week in FY2024.

Profitability

Chewy’s earnings, on an adjusted basis, have seen continued growth. In the third quarter of 2025, adjusted net income grew 60% YoY to $135.7 million, or $0.32 per share. On a GAAP basis, net income jumped to $59.2 million, or $0.14 per share, from $3.9 million, or $0.01 per share, reported in the same period last year. Gross margin increased 50 basis points YoY to 29.8% in Q3. For the fourth quarter of 2025, CHWY expects adjusted earnings per share to range between $0.24-0.27.

Diverse revenue streams

Chewy continues to benefit from its diverse revenue streams such as its Chewy+ membership program, health offerings, and new product launches.

As mentioned on the earnings call, Chewy+ continues to perform well with strong order frequency, category engagement, mobile app adoption, and Autoship participation. At the end of October, the company raised its annual fee to $79 from the earlier price of $49 and the early response has been positive with continued growth and strong conversion from free to paid memberships. CHWY remains optimistic on the growth and margin potential of this program.

Chewy Vet Care (CVC) continues to outperform, with each clinic helping in customer acquisition and retention. CHWY opened two new locations in Q3, including one in Phoenix, bringing its total to 14 locations across five states. The company plans to open two more clinics, putting it on track with its goal to open 8-10 locations this fiscal year.

Chewy has launched Get Real, a new brand of fresh dog food, which is anticipated to see growth with strong consumer demand. In Q3, the company announced the acquisition of leading equine health brand, SmartEquine. This deal will broaden Chewy’s range of premium health and nutraceutical offerings and help it expand into higher-margin health and wellness verticals, thereby providing significant opportunity to boost sales and margins.