Chubb Limited (CB) delivered a modest earnings beat in Q1 2026, reporting adjusted EPS of $6.82 versus the $6.80 consensus estimate, a narrow 0.3% surprise that landed with a muted market response. The stock traded largely unchanged following the report, suggesting investors had already priced in the insurer’s strong underlying momentum. With net premiums written reaching $14.00B and net income climbing to $2.32B, the quarter reflected both top-line expansion and margin improvement—a combination that speaks to operational leverage rather than financial engineering.

The quality of this earnings beat derives primarily from genuine topline expansion paired with margin improvement, not cost-cutting artifice. Net margin expanded to 16.6% from 13.6% a year ago, a gain of 2.9 percentage points that signals improving profitability on each premium dollar collected. Operating margin reached 12.8%, while operating cash flow of $3.95B demonstrates the cash-generative nature of the business model. The year-over-year EPS surge of 85.3% from $3.68 to $6.82 dramatically outpaced the topline growth, confirming that Chubb isn’t merely growing larger—it’s growing more profitable. This margin expansion against a backdrop of double-digit revenue growth represents the hallmark of a well-underwritten insurance franchise operating in favorable market conditions.

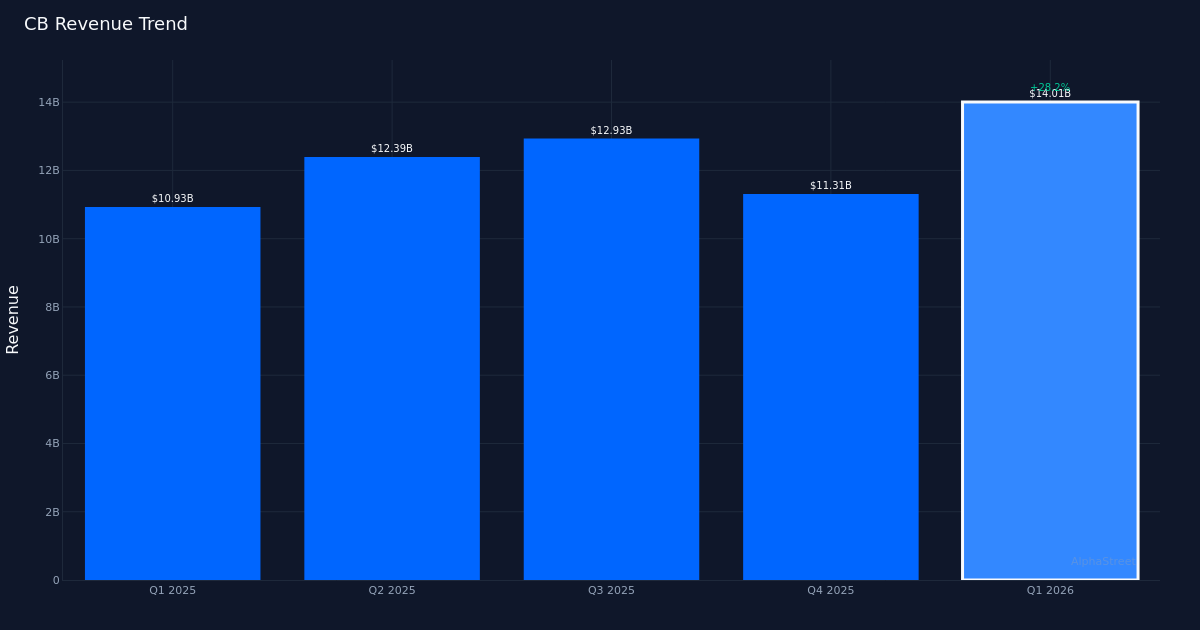

Revenue trajectory reveals strong momentum but sequential volatility that warrants scrutiny. The four-quarter trend shows Q1 2026 revenue of $14.00B, representing the highest quarterly figure in the series, surpassing Q3 2025’s $12.93B and Q4 2025’s $11.31B. However, the pattern is decidedly mixed: revenue oscillated from $12.39B in Q2 2025 to $12.93B in Q3 2025, then dropped to $11.31B in Q4 2025 before rebounding to the current $14.00B. Management highlighted this growth explicitly, noting “Total Company net premiums grew 10.7% for the quarter to more than $14 billion.” The 10.7% year-over-year growth rate as reported indicates sustained momentum, though the sequential volatility suggests quarterly comparisons may be distorted by premium recognition timing, catastrophe losses, or renewal cycles inherent to the property and casualty business.

Segment performance reveals a tale of two businesses with dramatically different growth trajectories. The P&C Insurance segment generated $11.72B with 7.2% growth. The combined ratio of 84.0% indicates the segment is writing profitable business with a 16-point underwriting margin before investment income—a strong result in an industry where breaking 100% separates winners from losers. Meanwhile, Life Insurance posted $2.29B in revenue with explosive 33.1% growth, suggesting either aggressive expansion, favorable market conditions, or easier year-ago comparisons. Management noted “Our life division produced $316 million of pre-tax income in the quarter, up 8.5%,” revealing that while revenue surged 33.1%, profitability growth of 8.5% lagged substantially. This divergence implies mix shift toward lower-margin products or elevated acquisition costs that bear monitoring. The company’s presence across 54 countries and territories provides geographic diversification, though the segment disclosure doesn’t break out regional contribution.

Balance sheet management reflects conservative stewardship in an uncertain rate environment. Management’s commentary on capital allocation emphasized opportunistic funding: “During the quarter, we issued CHF200 million, or approximately $250 million, of six-year debt at a very attractive cost of 1%.” Locking in 1% funding costs for six years provides a hedge against potential rate volatility while maintaining financial flexibility. The company also highlighted credit portfolio discipline, stating, “This discipline is further evident in our very modest exposure to software, which at less than $150 million or 4% of the direct lending portfolio, is a fraction of the 20% average across the sector and less than a quarter percent of our total investment portfolio.” This risk management stance positions Chubb defensively, should the software sector stress materialize.

The Worksite Benefits commentary suggests underappreciated growth in an ancillary segment. Management noted, “The Chubb Worksite Benefits, the 16% growth there, that’s pretty solid, I think, especially after a similar growth last year,” indicating sustained double-digit expansion in voluntary employee benefits. While not broken out as a separate reportable segment, consecutive years of 16% growth in this category suggests a competitive advantage in distribution or product that deserves investor attention as a potential value driver beyond the core P&C and Life segments.

The muted stock reaction despite strong results and the 100% beat rate over the last quarter signals either full valuation or investor skepticism about sustainability. A company posting 85.3% EPS growth and 10.% revenue expansion while improving margins would typically draw more enthusiastic market response. The unchanged stock price suggests either that expectations had already incorporated these results, concerns about near-term headwinds not yet visible in the numbers, or valuation levels that leave little room for multiple expansion. The 100% beat rate covers only the most recent quarter, providing insufficient track record to assess consistency.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.