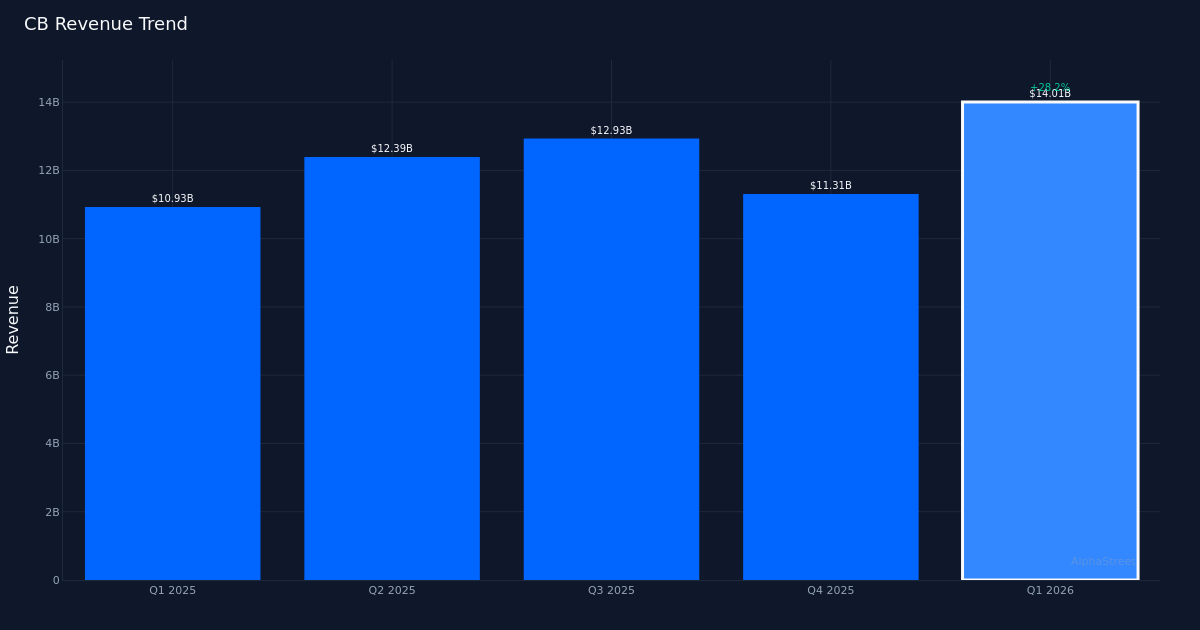

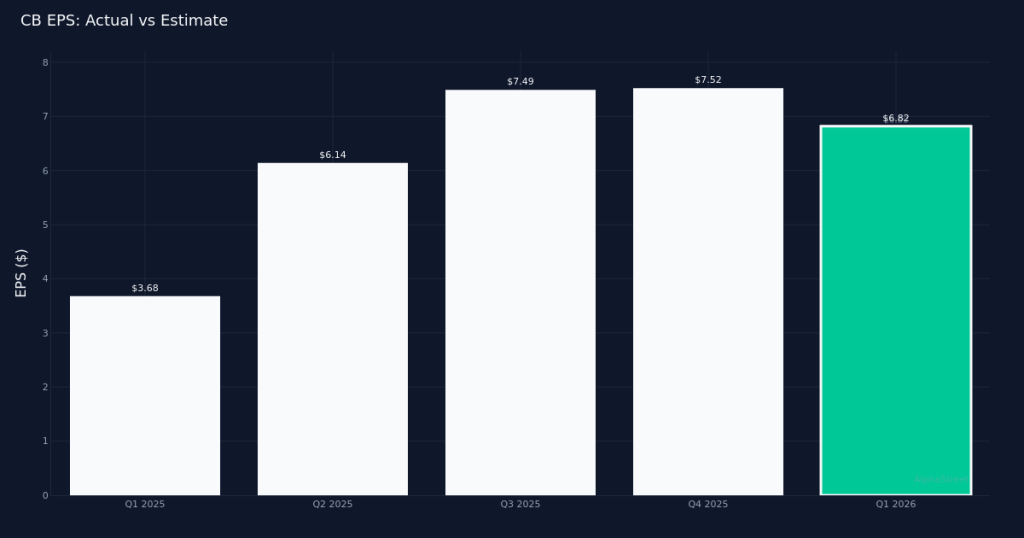

In-Line Quarter. Chubb Limited (CB) delivered Q1 2026 core operating income earnings of $6.82 per share, essentially matching the $6.80 consensus estimate in a quarter characterized by solid revenue momentum and disciplined underwriting execution. Revenue totaled $14.01B for the quarter, up 10.7% from $12.65B in Q1 2025, demonstrating the property and casualty insurer’s ability to capitalize on favorable pricing dynamics and strong commercial demand across its global platform. Bottom-line profit came in at $2.69B, reflecting the quality of earned premiums flowing through the income statement.

Underwriting Excellence. The P&C combined ratio of 84.0% for the quarter underscores Chubb’s continued underwriting discipline in an environment where many competitors have sacrificed profitability for growth. This metric, which measures claims and expenses as a percentage of premiums earned, indicates the company is generating underwriting profits well above industry averages while simultaneously expanding its top line. The combination of revenue growth and favorable combined ratio positioning suggests this is a revenue-driven performance rather than one reliant on cost reductions, a materially higher-quality outcome that should support sustained margin expansion.

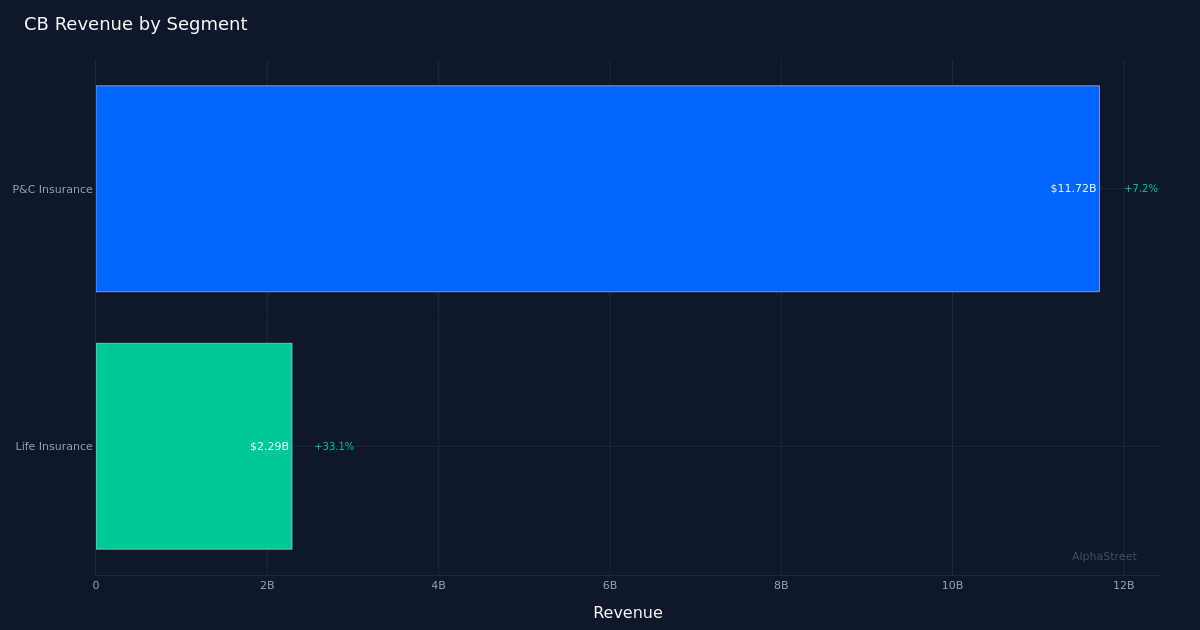

Segment Performance. P&C Insurance led the company’s diversified portfolio with $11.72B in revenue, up 7.2% year-over-year, demonstrating the strength of Chubb’s core commercial and specialty lines business. This segment’s performance reflects the company’s global footprint, with operations spanning 54 total countries and territories at quarter end, providing both geographic diversification and exposure to varying rate environments. The segment’s growth trajectory suggests pricing remains rational in key markets while volume trends support continued premium expansion.

Muted Market Reaction. Shares traded largely unchanged following the report, a response that likely reflects the in-line earnings result offering limited surprises relative to investor expectations heading into the print. While the revenue growth and combined ratio performance were constructive, the lack of an earnings beat provided no catalyst for multiple expansion in a stock that has already priced in much of the company’s operational excellence.

Analyst Positioning. Wall Street consensus stands at 11 buy, 14 hold, and 1 sell, a distribution that suggests moderate conviction in the name with the majority of analysts maintaining neutral stances. This relatively balanced view may reflect questions about valuation following the stock’s strong multi-year run, even as fundamental trends remain supportive of the underwriting franchise.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.