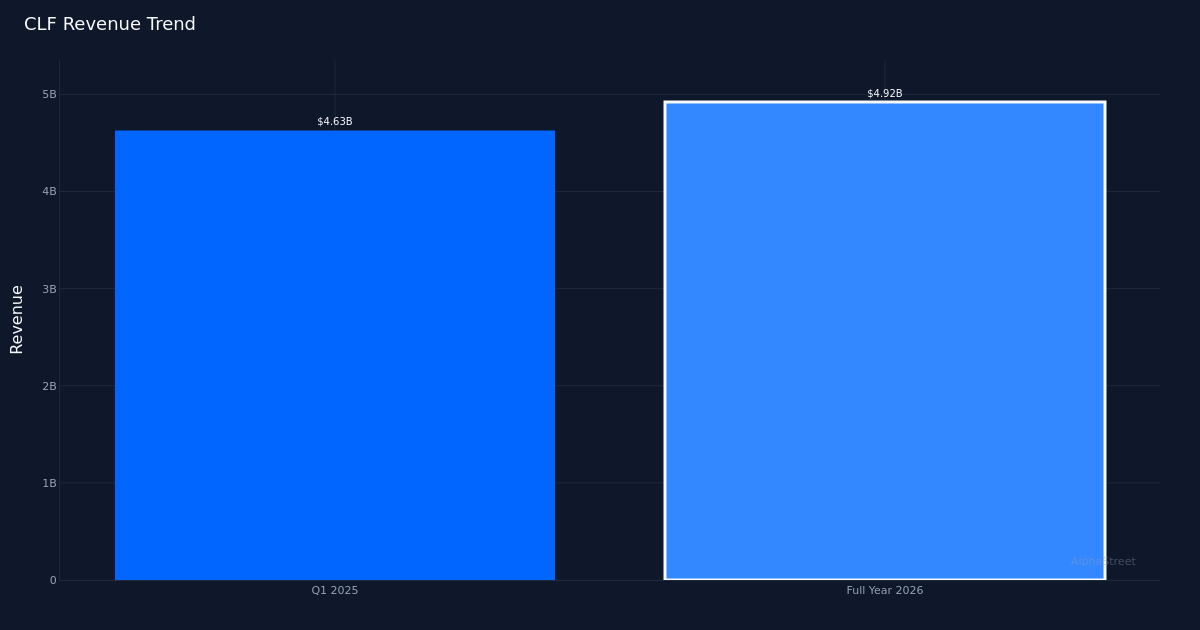

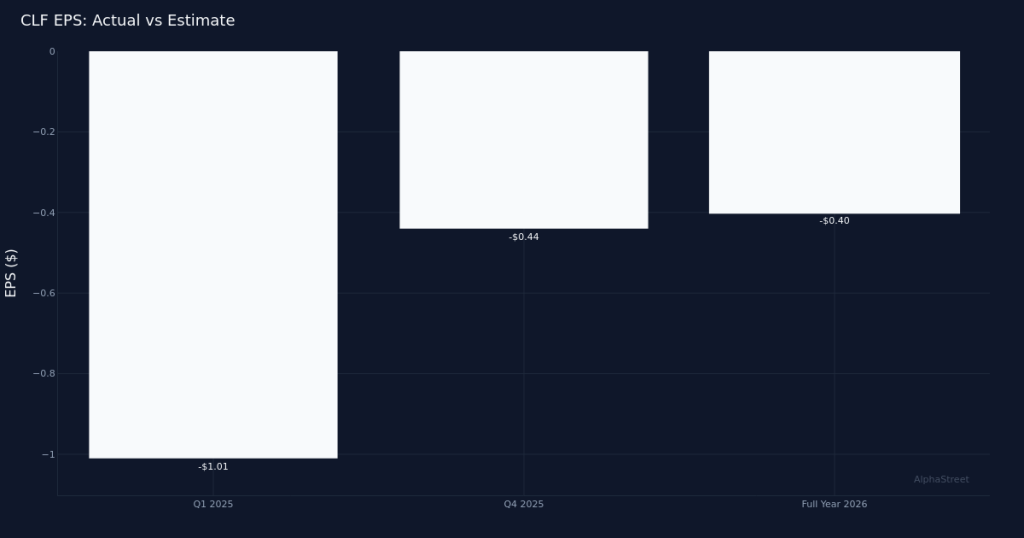

Steep Loss Reported. Cleveland-Cliffs Inc. (NYSE:CLF) posted a Q1 2026 adjusted loss of $0.40 per share, marking another challenging quarter for the vertically integrated steel producer as margin pressures persist across the domestic steel industry. The bottom line showed a net loss of $229.0M, underscoring the difficult operating environment facing North American steelmakers amid weak pricing power and elevated input costs. Revenue totaled $4.92B for the quarter, up 6.3% from $4.63B in Q1 2025, though the top-line growth proved insufficient to offset operating headwinds that compressed profitability.

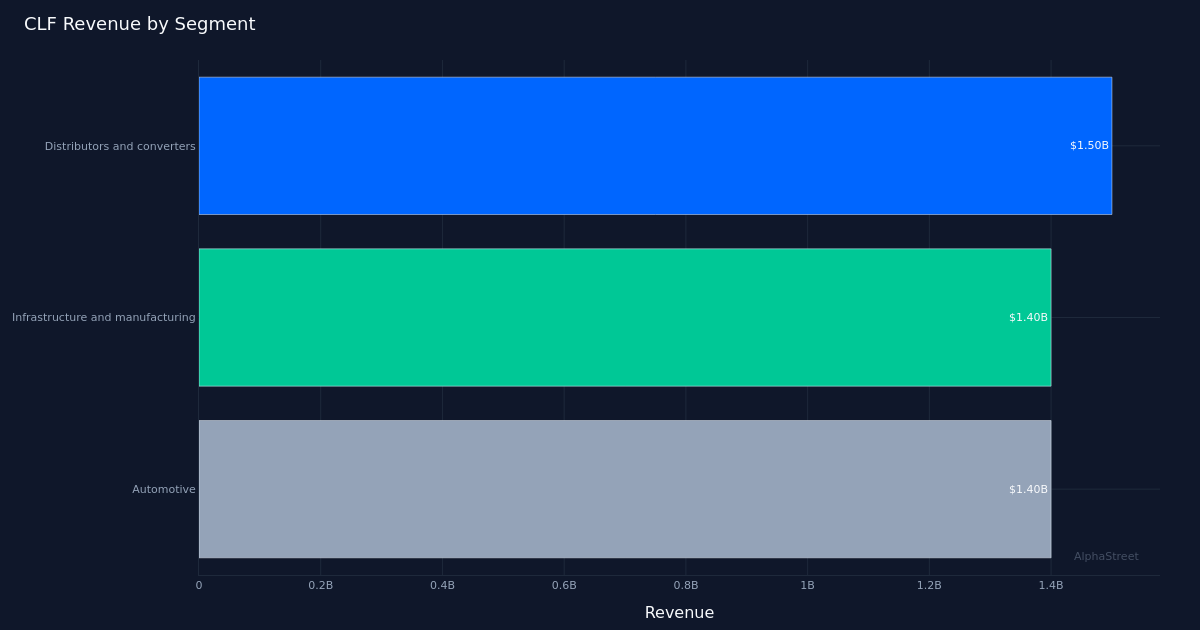

Volume Growth Outpaces Pricing. The revenue expansion reflects primarily volume-driven improvements rather than pricing strength, with steel product sales volumes reaching 4,108,000 net tons for the quarter. The company operated 4,100,000 steel shipments in net tons at quarter end, demonstrating operational throughput despite market softness. Distributors and converters remained the largest customer segment, generating $1.50B in revenue for the quarter, accounting for 31% of total sales. The volume trajectory suggests Cleveland-Cliffs maintained market share, though the inability to translate higher volumes into profitability highlights the competitive pricing dynamics that continue to pressure the entire steel sector.

Market Remains Cautious. Wall Street consensus reflects persistent skepticism about the steel cycle, with analyst ratings standing at 2 buy, 13 hold, and 6 sell recommendations. The bearish tilt underscores concerns about sustained margin compression and the timing of any potential industry recovery. Despite the quarterly loss, shares rose following the release, suggesting investors may have braced for worse results or are beginning to price in expectations for sequential improvement as the year progresses. The modest positive reaction indicates the market may be looking past current weakness toward potential second-half recovery catalysts.

Structural Challenges Persist. The year-over-year loss deepening comes despite revenue growth, pointing to fundamental margin structure issues that volume alone cannot remedy. Cleveland-Cliffs’ vertically integrated model—spanning iron ore mining through finished steel production—provides supply chain advantages but also creates fixed cost exposure during demand weakness. The company’s ability to return to profitability hinges on either sustained pricing improvement across steel products or significant operational cost reductions, neither of which appears imminent given current industry conditions and the substantial capital intensity inherent in steel manufacturing.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.