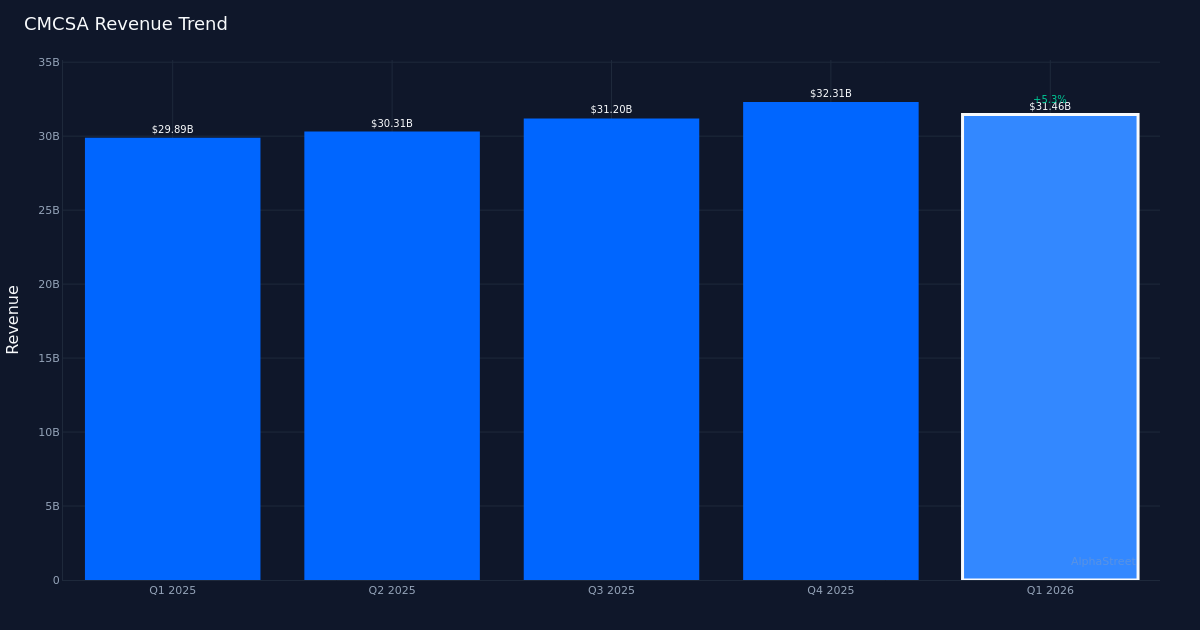

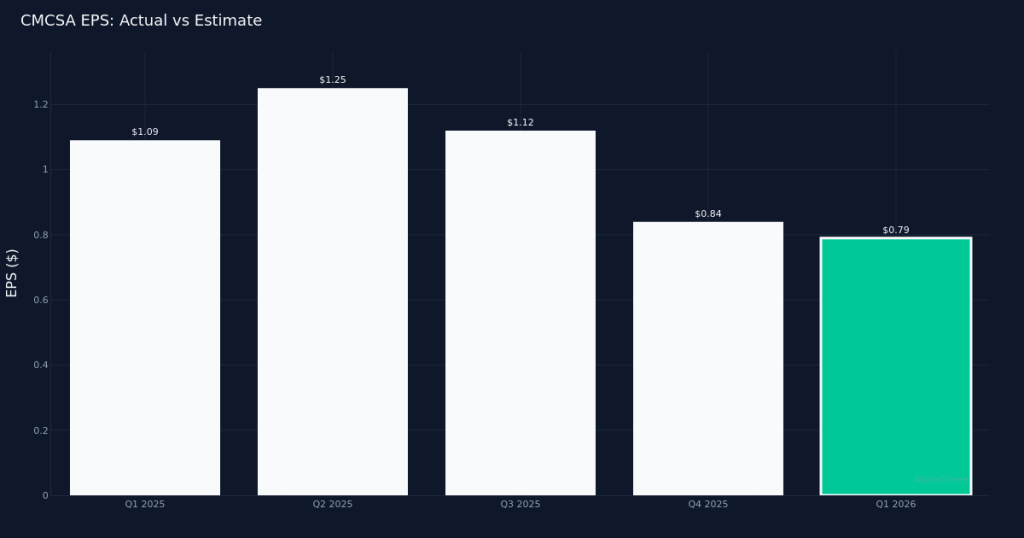

Solid beat. Comcast Corporation (NASDAQ:CMCSA) delivered Q1 2026 adjusted EPS of $0.79, topping Wall Street’s $0.76 estimate by 3.9%, as the telecom and media giant demonstrated continued momentum in its wireless business while navigating headwinds in its legacy connectivity operations. Revenue totaled $31.46B for the quarter, up 5.3% from $29.89B in Q1 2025, reflecting the company’s ability to extract growth from shifting consumer preferences despite pressure on traditional broadband and video services. The company earned $2.86B in adjusted net income for the period, underscoring the profitability of its diversified service portfolio.

Revenue-driven performance. The quality of this earnings beat appears genuine, anchored by topline expansion rather than aggressive cost-cutting. The 5.3% year-over-year revenue growth suggests Comcast is successfully offsetting declines in mature business lines with expansion in higher-growth areas, particularly wireless services. This revenue-driven beat carries more weight for long-term investors than margin engineering alone, indicating the company retains pricing power and market share in key segments even as competitive intensity remains elevated across telecom services.

Wireless momentum accelerates. Domestic wireless operations continue to serve as a bright spot, with the company adding 435,000 net new lines during the quarter and reaching 9.7M total domestic wireless lines at quarter end. This wireless expansion represents a strategic pivot for Comcast, leveraging its existing customer relationships and infrastructure investments to capture share in the mobile market. The wireless business provides a growth vector that partially offsets structural challenges in traditional cable, though the capital intensity of network investments and competitive promotional activity from incumbent carriers warrant continued monitoring.

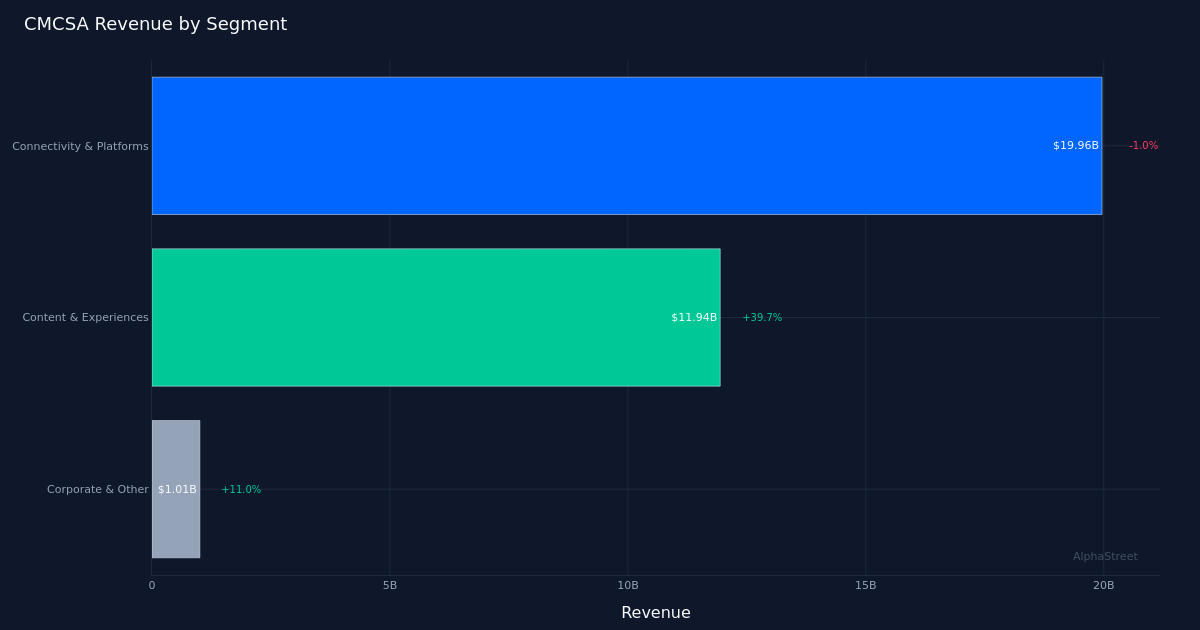

Core connectivity pressures persist. The Connectivity & Platforms segment led revenue generation with $19.96B but saw a 1.0% year-over-year decline, highlighting ongoing pressures in the company’s foundational broadband and video businesses. Cord-cutting trends and fixed wireless competition from telecom rivals continue to weigh on this segment, even as the company attempts to bundle services and drive ARPU improvements. The modest decline suggests stabilization rather than accelerating deterioration, but the segment’s trajectory remains a key concern for investors evaluating the company’s long-term value proposition.

Market reaction. Shares jumped 8.5% after the release, reflecting optimism that management can sustain profitable growth amid industry headwinds. Wall Street consensus stands at 10 buy, 21 hold, and 3 sell ratings, indicating a divided view on the company’s prospects as it transitions from legacy cable dominance to a more diversified connectivity and content model.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.