Shares of Conagra Brands Inc. (NYSE: CAG) were down 7% on Thursday after the company delivered mixed results for its fourth quarter of 2022. While earnings beat estimates, sales fell short. Like its peers, Conagra is dealing with the impacts of inflation but the company is taking measures to tackle the situation. During the quarter, the company saw margins improve in some of its segments and it anticipates this improvement will extend to all the segments in the coming year.

Mixed results

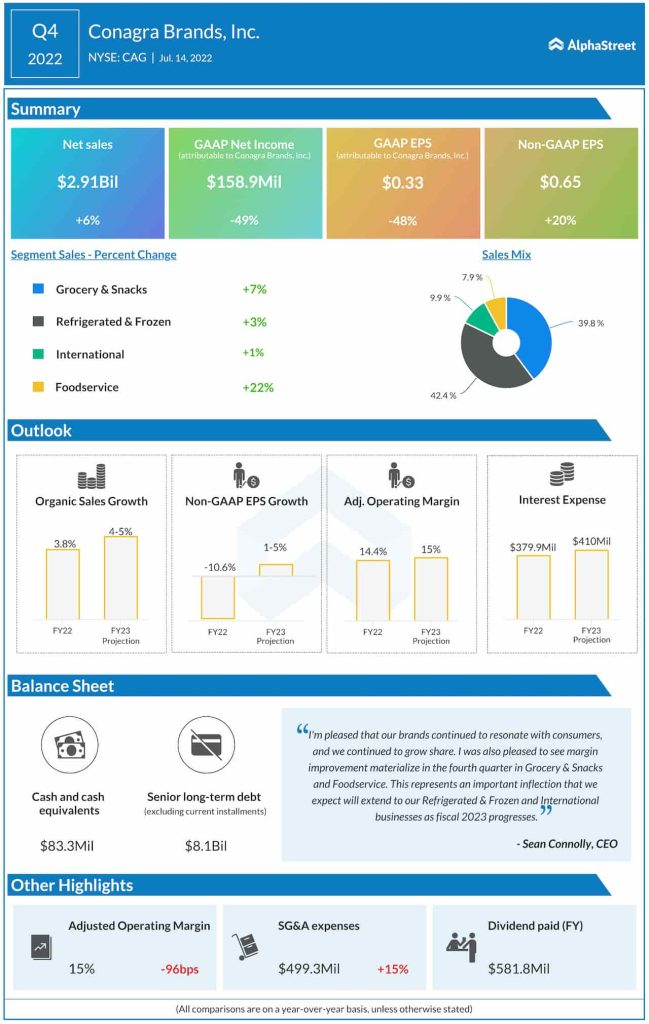

For the fourth quarter of 2022, Conagra generated net sales of $2.91 billion, which rose 6.2% year-over-year but fell short of market estimates. Net sales increased 6.8% on an organic basis. Adjusted EPS rose 20% to $0.65, beating projections.

Trends

During the quarter, organic sales growth was driven by a double-digit improvement in price/mix that was fueled by pricing actions and favorable brand mix. However the price increases led to a 6.4% drop in volume. Gross margin dropped 183 basis points to 24.5% due to the impacts of inflation.

Conagra delivered sales growth across all its segments, both on a reported and organic basis, but volumes decreased across most of the segments due to the impact of price hikes. The Grocery & Snacks segment saw a 7% decline in volume but the company gained share in both the staples and snacking categories during the quarter.

In the Refrigerated & Frozen segment, Conagra gained share in categories such as frozen single serve meals, frozen meat substitutes, and frozen desserts. Volumes in the foodservice segment rose by 4.5% as restaurant traffic picked up thanks to the easing of the pandemic. This was, however, partly offset by the elasticity impacts from pricing actions.

During the quarter, the Grocery & Snacks and Foodservice segments recorded increases in adjusted operating profit while the Refrigerated & Frozen and International divisions saw decreases. Conagra expects margins to improve across all its segments as FY2023 progresses.

Outlook

Looking ahead, Conagra expects cost of goods sold inflation to continue into fiscal year 2023 and it has rolled out price increases that will take effect during the second quarter of 2023. The company’s guidance assumes gross inflation to be in the low-teen levels.

For FY2023, Conagra expects organic net sales to grow 4-5% and adjusted EPS to increase 1-5% year-over-year. Adjusted operating margin is expected to be approx. 15%. Capital expenditures are expected to total around $500 million.

Click here to access the full transcripts of the latest earnings conference calls