Shares of Constellation Brands Inc. (NYSE: STZ) stayed in green territory on Friday. The stock has gained 8% over the past 12 months. The brewer ended fiscal year 2022 on a solid note with better-than-expected results for the fourth quarter of 2022. Here’s a look at the company’s expectations for the coming year:

Revenue and profitability

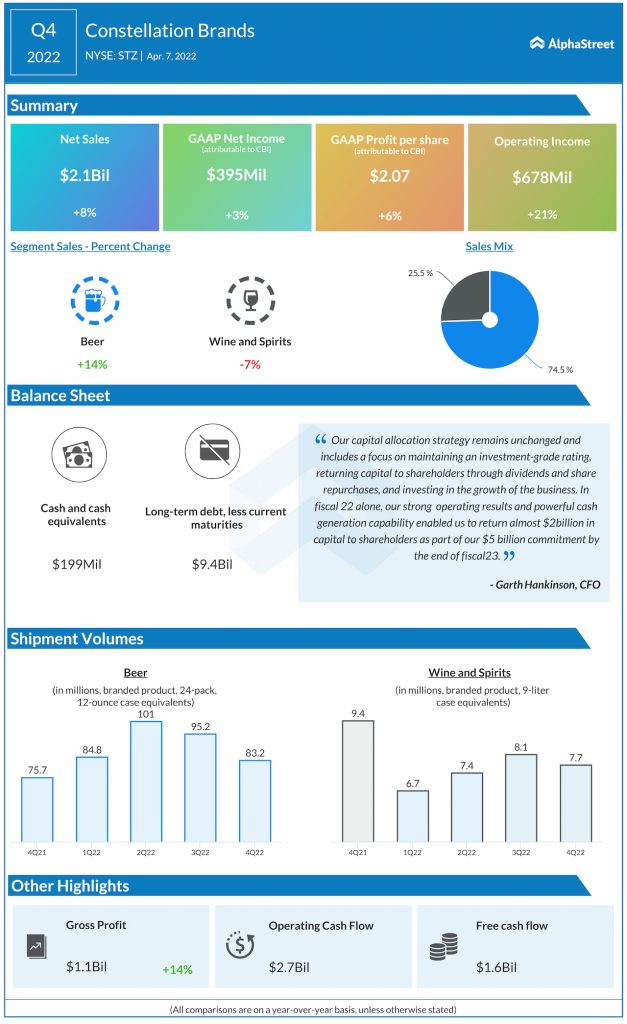

For the fourth quarter of 2022, Constellation reported net sales of $2.1 billion, reflecting a growth of 8% compared to the year-ago period. The top line exceeded estimates and was driven by strength in the beer business.

EPS, on a reported basis, rose 6% to $2.07 while comparable EPS jumped 30% to $2.37, beating estimates. For fiscal year 2023, Constellation expects reported EPS to range between $11.15-11.45 and comparable EPS to range between $11.20-11.50.

Beer and wine segments

Constellation’s beer business continues to show strong momentum. Net sales rose 14% to $1.56 billion in Q4. Depletion growth was nearly 10%, driven by strength in the Modelo Especial and Corona Extra brands. Operating income increased 21% to $613.6 million.

In FY2023, net sales for the beer segment is expected to grow 7-9% while operating income is estimated to grow 2-4%. Total beverage alcohol servings per cabinet are expected to stay stable, with growth of about 1-2% annually. Mexican imports are expected to be a key driver of gains in the overall beer segment. The flavors category is expected to see significant growth, including seltzers, flavoured beer, RPG spirits, and flavoured malt beverages, with all categories displaying strong future growth prospects.

On its quarterly conference call, the company said its Modelo Especial brand holds the number two position in dollar sales in the country and has meaningful distribution runway over the medium term to facilitate mid to high single digit total annual volume growth in the off-premise channel.

The Corona Extra brand has a fairly high household penetration but it continues to lag behind larger rivals. Constellation projects modest growth for this brand in the upcoming year. For the Pacifico brand, the company is forecasting 10-15% total annual volume growth in the medium term from distribution alone.

Within the Wine and Spirits business, net sales decreased 7% year-over-year to $536.8 million in Q4 but on an organic basis, sales grew 5%. Operating income increased 6% to $121.8 million. For FY2023, net sales in Wine and Spirits are expected to decline 1-3% while operating income is expected to grow 4-6%. In the coming year, within this segment, Constellation will focus on continued premiumization, margin expansion, and growth in DTC channels and the international business.

Capex, cash flow and shareholder returns

Capital expenditures are expected to range between $1.3-1.4 billion in FY2023. Operating cash flow is estimated to be $2.6-2.8 billion while free cash flow is expected to be $1.3-1.4 billion. Constellation returned nearly $2 billion to shareholders in the form of dividends and share buybacks during FY2022 and the company plans to repurchase $500 million of its shares in Q1 2023.

Click here to read the full transcript of Constellation Brands’ Q4 2022 earnings conference call