Shares of Constellation Brands (NYSE: STZ) stayed red on Friday. The stock has dropped 23% over the past three months. The beer giant faced several challenges during the third quarter of 2025, leading it to deliver disappointing results for the period. The uncertainty over the macro environment has led to a bleak outlook for the full year as well. However, despite these headwinds, there are a few factors that might offer optimism.

Resilience of beer business despite slowdown in spend

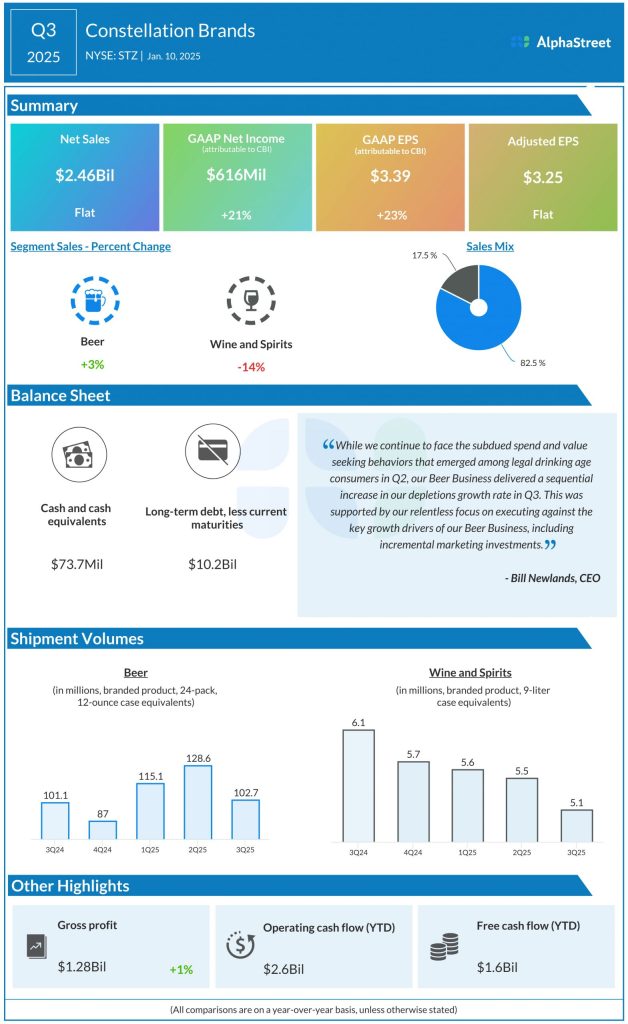

The main dampener in Constellation’s third quarter report was the impact of macroeconomic headwinds on consumer spending. A slowdown in spending and value-seeking behaviors among consumers in a tough economic environment have led to a slowdown in growth for beverage alcohol.

Despite these challenges, STZ’s beer business delivered growth in the third quarter. Net sales increased 3% year-over-year, supported by a 1.6% rise in shipment volumes. Depletions grew 3.2%, driven by growth in the Modelo Especial, Pacifico, and Modelo Chelada brands.

Constellation is facing headwinds from competitive pricing across its high-end light beer offerings, which include Modelo Oro and its Corona Light and Premier brands, especially in the large pack formats. In addition, its Chelada brands are seeing a slowdown in demand in the convenience channel. At the same time, brands like Modelo Especial, Corona Extra and Pacifico continue to gain share and grow sales.

Weakness in Wine but momentum in higher-end brands

Constellation has been seeing continued weakness in its Wine and Spirits segment. In Q3 2025, net sales declined 14% YoY, driven by a 16% drop in shipment volumes caused by weak consumer demand in the wine category, particularly in the lower-priced segments, and continued retailer inventory destocking. Depletions were down 4%.

However, the company is seeing growth in its higher-end crafts spirits portfolio, which delivered an increase of approx. 9% in depletions in the third quarter. The divestiture of SVEDKA will allow it to focus more on higher-growth, higher-margin brands based on changing consumer preferences. STZ’s fine wine portfolio also achieved depletion growth of 6% in Q3, with its largest premium wine brands Meiomi and Kim Crawford delivering depletion increases of over 7%.

Despite the persistent challenges in this segment, Constellation continues to expect improved organic shipment volume growth performance for this business in the fourth quarter of 2025 supported by benefits from pricing, marketing and distribution initiatives, as well as historical seasonal trends. It also expects to benefit from a stabilization in retailer inventory destocking.

Q3 performance

The headwinds in the Beer segment and weakness in the Wines division led to an underwhelming performance in the third quarter of 2025. Net sales of $2.46 billion and comparable earnings of $3.25 per share remained flat compared to the prior-year quarter.

Revised outlook

It remains uncertain whether consumers will revert to more normalized spending behaviors in the fourth quarter of 2025. This near-term uncertainty, along with continued consumer demand headwinds in the wines business, led Constellation to revise its outlook for fiscal year 2025.

The company now expects organic sales growth of 2-5% and comparable EPS of $13.40-13.80 for FY2025. Its previous expectations were for sales growth of 4-6% and comparable EPS of $13.60-13.80.

For the beer business, the company now expects net sales to grow 4-7% versus the previous expectation of a 6-8% growth. For the wines and spirits division, organic sales are now expected to decline 5-8% versus the prior range of a 4-6% decrease.