Shares of Constellation Brands (NYSE: STZ) stayed red on Friday. The stock has gained 4% in the past three months. The beverage company saw its sales and profits decline in the third quarter of 2026 compared to the previous year, along with sales declines across its segments. It expects lower sales and earnings for fiscal year 2026 as well.

Sales and earnings down

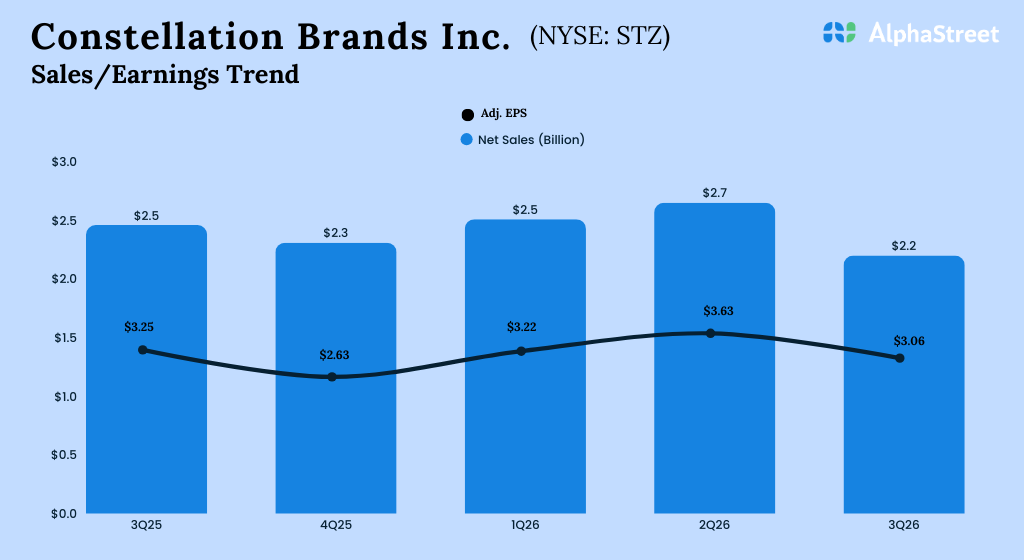

Constellation’s net sales decreased 10% year-over-year to $2.22 billion in the third quarter of 2026. The top line reflected impacts from the SVEDKA and wine divestitures. On an organic basis, sales were down 2%. Adjusted earnings per share declined 6% to $3.06. Despite the declines, the top and bottom line numbers were better than analysts’ projections.

Slow demand hurts beer business

Constellation continued to face a challenging operating environment with demand for alcoholic beverages seeing a slowdown as economic uncertainty and inflationary pressures weighed on consumer spending.

As mentioned on its conference call, the company’s beer business was hurt by weakness among Hispanic customers, who make up a substantial portion of its consumer base, as well as heavy-duty workers. Net sales in the Beer segment dropped 1%, driven by a 2.2% decline in shipments, partly offset by favorable pricing. Depletions were down 3%, with declines in both the off-premise and on-premise channels.

However, STZ managed to gain market share and increase distribution points in its beer business during the quarter. Its brand health remained strong and customers stayed loyal. Single-digit depletion declines in the Modelo Especial, Corona Extra and Modelo Chelada brands were partly offset by double-digit growth in the Pacifico and Victoria brands.

Not much sparkle in wines

Constellation’s Wine and Spirits segment saw net sales fall 51% YoY on a reported basis and 7% on an organic basis in Q3 2026. The sales decline was driven mainly by impacts from the SVEDKA and wine divestitures, strategic pricing actions taken on select brands, and changes in distributor contractual payments. Shipments decreased 70.6% while depletions were flat in the quarter.

On the other hand, the company’s higher-end wine portfolio outperformed the corresponding segment, with its Kim Crawford wine brand growing volume by over 2% and its Mi CAMPO Tequila brand seeing volume growth of around 24% in the quarter.

Outlook

Constellation forecasts organic net sales to decline 4-6% in fiscal year 2026. Net sales in the Beer segment are expected to drop 2-4% while organic sales in the Wine and Spirits segment are projected to fall 17-20%. Comparable EPS is expected to range between $11.30-11.60, down from $13.78 reported in FY2025.